3Q 2024 earnings preview – Key Singapore stocks to watch

3Q 2024 earnings preview – Key Singapore stocks to watch

The 3Q 2024 earnings season will unfold over the coming weeks, with any earnings resilience likely to be on market participants’ radar to drive further risk-taking. Year-to-date, the Straits Times Index (STI) is up more than 10%, driven by a catch-up rally in August this year. The index has been enjoying increased traction for its composition of dividend-paying stocks amid lower bond yields, along with ongoing authorities’ focus to increase Singapore stocks’ value proposition for investors.

But moving forward, corporate earnings will likely hold the key in determining whether the index can push to a new multi-year high. Here is a brief overview of what to expect for the key sectors and companies.

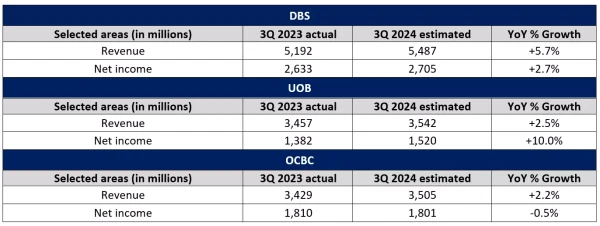

Banking trio: DBS, OCBC, UOB

With the US Federal Reserve (Fed)'s rate-cutting cycle in place, expectations are that the upcoming reporting quarter could see the banks’ net interest income contract slightly (-1% to -2%) from a year ago.

This comes as lending margins could see some downward pressures. A lower interest rate environment could weigh on banks’ loan rates, while funding costs are usually slower to adjust. However, the pace of tapering in the banks’ net interest margin (NIM) may remain gradual amid smaller Fed’s rate cuts priced into 2025, which may still offer some earnings resilience.

There will likely be earnings cushion around the banks’ net fee and commission income as well. Robust market conditions may help to support wealth management activities, alongside credit card fees on economic resilience. Aside, loan loss provisions may likely see a more measured build-up, with a slight downtick from previous quarter aiding to downplay economic risks.

With that, the banks’ overall profits should be able to grow at the low single-digit. With expectations for lower interest rates ahead, their current dividend yield of more than 5% may continue to stand out as an attractive income play.

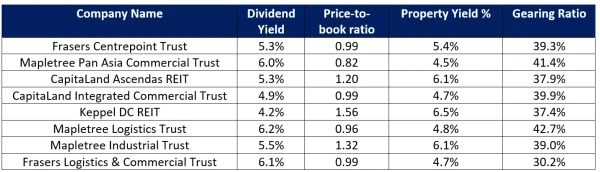

Real estate investment trust (REITs)

Despite surging as much as 16% over the past three months, the sector continues to trail the broader index by a significant margin. Year-to-date, the iEdge S-REIT index is still in the red by 2.8% while the STI is up 11%. Thus far, the major REITs continue to deliver attractive dividends in the range of 4 - 6%.

With sentiments around the rate-sensitive sector improving amid the Fed’s policy pivot, further catch-up performance among the REITs remains a theme to watch. A lower interest rate environment may help to lower the sector’s borrowing costs, drive higher property valuation for their portfolio and enables their dividend yield to stand out more.

Retail REITs (eg. CapitaLand Integrated Commercial Trust, Frasers Centrepoint Trust) may continue to stay supported by stable retail sales, along with brewing optimism of an October boost from Chinese tourists with the Golden Week holiday. Global trade dynamics in the region may help to support industrial REITs, which has also diversified their exposure into data centres, such as Mapletree Industrial Trust and Ascendas REIT. Ongoing digital transformation and broadening adoption of artificial intelligence (AI) across more sectors may help to offer a stable backdrop for these REITs’ earnings.

Industrials: Singapore Airlines, SATS, Yangzijiang

In the aviation space, travel demand is likely to remain healthy, but this has to be balanced with higher capacity in the market. Lower passenger yield, alongside rising fuel costs, would be a key challenge for airlines to tackle. Expectations are for Singapore Airlines’ FY2025 revenue to register a somewhat negligible growth (+0.7%), while net income could come with a 18% contraction from a year ago, alongside a fall in net margin.

For SATS, having reversed out of its losses in 1Q 2025, focus will be on whether the turnaround can continue. Expectations are for FY 2025 revenue to register a 9.7% growth from the previous year, alongside a four-fold improvement in net income. After a strong improvement in operating profit margins in Q1 FY25, market participants will keeping an eye on whether SATS can maintain or improve these margins as well.

Yangzijiang Shipbuilding clearly has a bumper year so far, with its share price up 71.1% year-to-date and holds the award for the top-performing STI constituent as of today (9 Oct 2024). A record-high order book offered strong visibility for future revenue through 2028, as it remains a beneficiary for the clean energy transition theme or low-carbon shipping. 79% of its new orders are classified as clean energy vessels. Expectations are for FY2024 revenue to increase 16.0% year-on-year, while growth momentum may be expected to pick up pace to deliver a 19.7% growth for FY 2025.