Analyzing market impacts: insights into the upcoming 5-year and 7-year US Treasury auctions.

Summary:

- Despite the considerable size of the auction, the 5-year US Treasury auction is poised to outperform the 7-year auction. This is due to the likelihood that the current pricing of these notes may result in the second-highest auction yield since 2007. Moreover, the 5-year notes present a more favorable risk-reward proposition compared to their 7-year counterparts.

- If the 5-year auction tails When-Issued, it's probable that the 7-year auction will also tail, potentially prompting a rise in yields across tenors prior to the release of the PCE deflator on Friday.

- Three possible outcomes loom over the upcoming US Treasury auctions. However, even in the event of robust auctions, 10-year US Treasury yields are expected to maintain their uptrend, with little chance of dropping below 4.5% as they edge closer to the 5% mark.

Why is the belly of the yield curve important?

Changes in the yields of 5-year and 7-year US Treasury notes can provide valuable insights into broader economic conditions and interest rate expectations. These tenors are often viewed as an intermediate-term horizon, capturing expectations for economic growth, inflation, and monetary policy over a reasonably foreseeable future. Consequently, shifts in the yields of these tenors can reflect changes in market sentiment and expectations for future economic performance.

The 5-year and 7-year tenors exhibit significant sensitivity to changes in interest rates. They are more sensitive than shorter-term securities but less sensitive than longer-term securities. Therefore, these securities offer a sweet spot for those investors that are looking to extend/decrease duration at times of changing macroeconomic conditions, provoking a sudden rise or drop of this part of the yield curve ahead of a yield curve’s steepening or flattening.

The 5-year and 7-year US Treasury notes serve as important benchmarks for borrowing and lending in the junk bond space. As a matter of fact, the average maturity for junk bond debt is around 5 years. A sudden rise in yields in this part of the yield curve might be fatal to those cash-strapped companies that might need to raise debt imminently. If spreads spike in the lowest-rated high-yield corporate bonds, volatility might also arise in higher-rated segments of the corporate bond markets. However, considering that a substantial wave of junk bond maturities is not expected until the beginning of 2025, this risk appears to be contained.

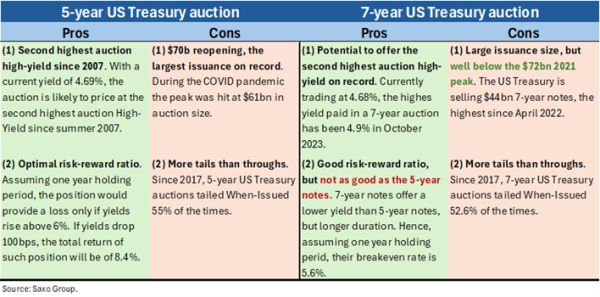

Five-year and seven-year note auctions: pros and cons.

The promising news is that both the 5-year and 7-year Treasury yields are currently at appealing levels. If the auction prices align with the current trading yield level, they will mark the second-highest auction yield since 2007 for the 5-year US Treasury auction and the second-highest auction yield on record for the 7-year tenor. Additionally, the risk-reward ratio offered by these tenors is attractive: yields would need to rise above 6% and 5.6%, respectively, within one year to result in a loss.

However, concerns arise when considering the sizes of the upcoming auctions. The US Treasury is set to sell the highest amount of 5-year notes on record, surpassing the peak during the COVID pandemic of $61 billion. While the size of the 7-year auction is below the COVID peak, it still the largest since April 2022. Notably, the When-Issued (WI) tails versus the through are also worth mentioning. According to records dating back to 2017, both tenors have recorded more tails than through, reflecting the high volatility in this segment of the yield curve.

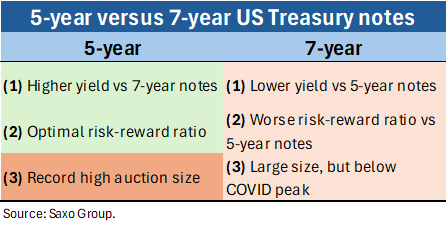

Exploring why the 5-year note auction might outperform the 7-year note auction.

Upon comparing the upcoming 5-year and 7-year US Treasury auctions, it becomes evident that the primary downside of the 5-year sale lies in its auction size. However, despite this drawback, 5-year notes present a compelling proposition with higher yields and lower duration risk compared to their 7-year counterparts.

This suggests that investors are likely to show greater interest in securing favorable returns through the 5-year tenor rather than the 7-year tenor. Consequently, if a tail materializes in the 5-year US Treasury auction, it's probable that the 7-year auction will also experience similar dynamics.

Exploring potential impacts on 10-year US Treasury yields.

Three possible outcomes loom over the upcoming US Treasury auctions. However, even in the event of robust auctions, 10-year US Treasury yields are expected to maintain their uptrend, with little chance of dropping below 4.5% as they edge closer to the 5% mark.

The possible scenarios are:

1. Both Auctions Stop Through WI: This scenario indicates robust demand for US Treasuries across various tenors, as investors seek to extend duration, capitalizing on above-average yields. In this case, 10-year US Treasury yields are likely to break below weak resistance at 4.58%, with the next resistance level expected at 4.5%. However, it's unlikely for yields to drop below this level as the market awaits PCE numbers on Friday.

2. Both Auctions Tail WI: This outcome would be bearish for US Treasuries across all tenors, signaling insufficient demand to meet issuance for the 5-year tenors and a lack of investor interest in extending duration up to seven years. If this occurs, 10-year US Treasury yields might break above resistance at 4.70% and continue their ascent towards 5%.

3. One Stops Through and One Tails: This scenario suggests good demand, but investors are selective. They may either reject duration or opt to extend it. Such a mixed signal could result in either a steepening or flattening of the yield curve, depending on the strength of duration demand. Within this scenario, 10-year US Treasury yields are likely to continue trading within a range of 4.5% to 4.7%.

Other recent Fixed Income articles:

18-Apr Italian BTPs are more attractive than German Schatz in today's macroeconomic context

16-Apr QT Tapering Looms Despite Macroeconomic Conditions: Fear of Liquidity Squeeze Drives Policy

08-Apr ECB preview: data-driven until June, Fed-dependent thereafter.

03-Apr Fixed income: Keep calm, seize the moment.

21-Mar FOMC bond takeaway: beware of ultra-long duration.

18-Mar Bank of England Preview: slight dovish shift in the MPC amid disinflationary trends.

18-Mar FOMC Preview: dot plot and quantitative tightening in focus.

12-Mar US Treasury auctions on the back of the US CPI might offer critical insights to investors.

07-Mar The Debt Management Office's Gilts Sales Matter More Than The Spring Budget.

05-Mar "Quantitative Tightening" or "Operation Twist" is coming up. What are the implications for bonds?

01-Mar The bond weekly wrap: slower than expected disinflation creates a floor for bond yields.

29-Feb ECB preview: European sovereign bond yields are likely to remain rangebound until the first rate cut.

27-Feb Defense bonds: risks and opportunities amid an uncertain geopolitical and macroeconomic environment.

23-Feb Two-year US Treasury notes offer an appealing entry point.

21-Feb Four reasons why the ECB keeps calm and cuts later.

14 Feb Higher CPI shows that rates volatility will remain elevated.

12 Feb Ultra-long sovereign issuance draws buy-the-dip demand but stakes are high.

06 Feb Technical Update - US 10-year Treasury yields resuming uptrend? US Treasury and Euro Bund futures testing key supports

05 Feb The upcoming 30-year US Treasury auction might rattle markets

30 Jan BOE preview: BoE hold unlikely to last as inflation plummets

29 Jan FOMC preview: the Fed might be on hold, but easing is inevitable.

26 Jan The ECB holds rates: is the bond rally sustainable?

18 Jan The most infamous bond trade: the Austria century bond.

16 Jan European sovereigns: inflation, stagnation and the bumpy road to rate cuts in 2024.

10 Jan US Treasuries: where do we go from here?

09 Jan Quarterly Outlook: bonds on everybody’s lips.