Apple (AAPL) Q4 2024 Earnings Preview: AI Integration and China Market in Focus

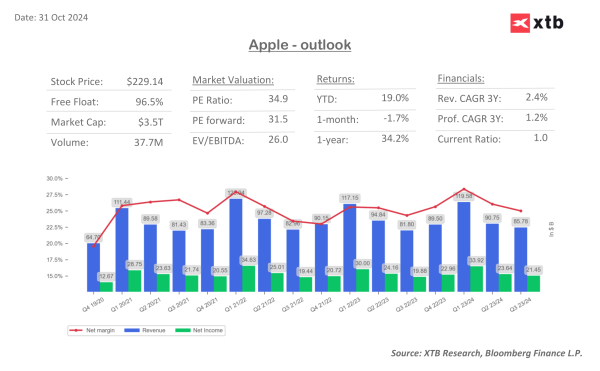

As Apple prepares to report its fiscal fourth-quarter earnings after the market close on October 31, 2024, all eyes are on the tech giant's performance amid shifting market dynamics and technological transitions. Trading near all-time highs with a 19% year-to-date gain, Apple approaches this earnings report with considerable momentum, though analysts remain cautiously optimistic about the quarter's results.

Earnings estimates

For the fiscal fourth quarter, analysts expect Apple to report revenue of $94.58 billion, representing a 5.7% year-over-year increase – the company's strongest annual growth in two years. Earnings per share are projected at $1.48, marking a modest 1% increase from the previous year. These expectations reflect both the opportunities and challenges Apple faces in its key markets, particularly in China.

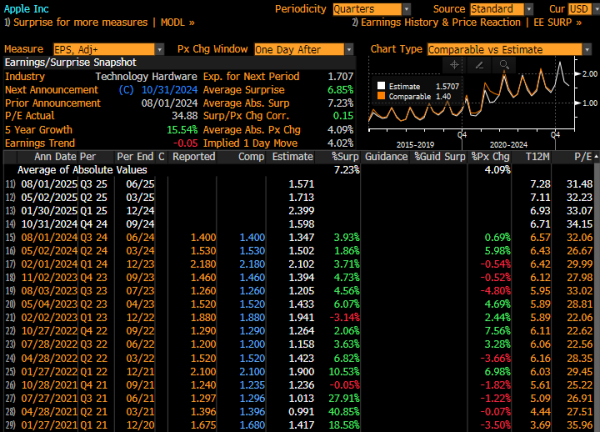

The consensus EPS estimate stands at $1.598 (GAAP), showing a modest 0.22% growth over the previous period. This figure sits between the various analyst projections we've seen, with some forecasting $1.48 (LSEG estimate) and others projecting $1.60 (TradingView consensus). The company has demonstrated strong execution historically, beating EPS estimates in 7 out of the last 8 quarters, suggesting potential for another positive surprise.

Implied volatility after earnings. Source: Bloomberg

Profitability Metrics:

- Net Income (Adjusted): Expected at $24.323 billion, showing a 0.18% increase

- Operating Profit: Projected at $29.961 billion, with a slight decline of -0.02%

- EBITDA: Forecast at $32.127 billion, showing a -2.11% decrease

Looking ahead, analysts project continued growth with:

- Q1 2025 (Dec '24): EPS of $2.399

- Q2 2025 (Mar '25): EPS of $1.713

- Q3 2025 (Jun '25): EPS of $1.571

The market is pricing in a significant earnings reaction, with an implied one-day move of 4.09% following the report. This is particularly noteworthy given Apple's historical tendency to surprise to the upside, with an average earnings surprise of 7.23% over recent quarters.

iPhone's future

The iPhone segment remains crucial to Apple's success, and recent data suggests mixed signals. Early iPhone 16 sales in China have shown promising results, with a 20% increase in the first three weeks compared to its predecessor. Notably, consumers are gravitating toward higher-end models, with Pro and Pro Max versions experiencing a 44% surge in sales compared to the same period last year. However, reports of potential order cuts of approximately 10 million units across Q4 '24 to Q2 '25, primarily affecting lower-end models, have raised some concerns among investors.

What else to look for?

The integration of artificial intelligence into Apple's ecosystem has emerged as a key focus area for investors. The company recently launched iOS 18.1, featuring AI-based Apple Intelligence, which introduces enhanced writing tools, photo editing capabilities, and improved notification management. While these features are currently available on the latest iPhone models, the timeline for their rollout in China remains uncertain, though European Union availability is confirmed for April 2025.

Apple's Services segment continues to be a bright spot in the company's portfolio, contributing between 25-30% of overall revenue and maintaining its position as the most profitable division. Analysts expect Services revenue to grow by 13% year-over-year, slightly below the previous quarter's 14% growth but still maintaining impressive double-digit expansion. This segment, which includes the App Store, Apple Pay, Apple TV+, Apple Music, Apple Arcade, and iCloud, has become increasingly important to Apple's growth story and profit margins.

Other product categories are also showing promise, with iPad revenue projected to grow 10% year-over-year, following a robust 24% surge in the previous quarter driven by new model releases. The current quarter's results will partially reflect the impact of recent product launches, including the AirPods Max.

Looking ahead, investors will be particularly focused on management's commentary regarding several key areas: the broader rollout strategy for Apple Intelligence and AI features, plans for the Vision Pro headset amid reports of scaled-back production, strategies to navigate the competitive Chinese market, and the sustainability of Services growth. Additionally, any forward-looking indicators about the iPhone 16 cycle will be crucial for market sentiment.

Chart (daily interval)

The price is currently trading just above the 23.6% Fibonacci retracement level and between the 30- and 50-day SMAs. For bulls, holding above the 23.6% Fibonacci level and the 50-day SMA will be essential to maintain momentum. If this support fails, bears could push for a retest of the 100-day SMA. RSI indicates a bearish tilt, showing a divergence with lower highs and lows, while MACD is also gradually turning bearish, suggesting potential downside momentum. Source: xStation