Bank of Japan Preview: Exaggerated Expectations, and Potential Impact on Yen, Equities and Bonds

Key points:

- Japan's inflation and wage growth have recently come in above expectations, bolstering the speculation about a possible rate hike and reduced bond buying from the Bank of Japan.

- We believe the BOJ will adopt a gradual and cautious approach, balancing the risk of economic slowdown and market stability.

- Yen strength may have run its course, and Fed’s stance will matter more for the yen than the BOJ itself. A cautious stance on Japanese equities may be warranted, but selective opportunities still exist.

The Bank of Japan policy announcement is due on July 31. Timing remains tentative, but it is usually out around 10-11am SGT. Expectations are for the BOJ to move ahead with further policy normalization.

Japan’s inflation accelerated for a second month in June, with consumer prices excluding fresh food rising 2.6% YoY, slightly below economists' consensus of 2.7%. This marks the 27th consecutive month that inflation has met or exceeded the BOJ's 2% target. The core measure, excluding both fresh food and energy, rose to 2.2% YoY from 2.1% in May, with service prices accelerating for the first time since November. Workers’ base salaries also saw the highest jump since 1993, bolstering the case for rate hikes.

Market Expectations

- Rate Hike: The market has priced in a 15bps rate hike with over 50% probability, effectively suggesting a 7-8bps rate hike.

- Bond Buying Reduction: The BOJ is expected to cut its bond purchases, likely focusing on 5 to 10-year notes, from ¥6 trillion ($32 billion) to ¥5 trillion ($27 billion) monthly, with a further reduction to ¥3 trillion ($19.5 billion) within two years.

BOJ Has a Long History of Disappointing Hawks

The BOJ has a long history of disappointing hawkish expectations. In several meetings over the past few years, despite market anticipation for policy normalization through rate hikes or reductions in bond purchases, the BOJ has maintained its dovish stance. At the June meeting, when markets participants expected more definitive clues on tapering of bond buying, all they got was a decision to lay out the details of the BOJ’s bond buying at the July meeting. The April meeting had similarly surprised dovish, as we discussed in this article. The BOJ exited negative interest rates at the March meeting, but the language remained dovish and reaffirmed that an accommodative policy will be maintained.

While the market is anticipating significant policy moves, we believe it is unlikely that the BOJ will implement both a rate hike and a substantial reduction in bond buying simultaneously. Two hawkish moves at one policy meeting may be a bit of a stretch for a central bank that is inherently dovish by nature. There are several reasons for the BOJ to keep its pace of policy normalization gradual and modest. We discussed some of those considerations, including macro risks and fiscal sustainability risks, in a piece titled ‘A reality check on Bank of Japan’s policy normalization and JPY appreciation expectations’ earlier this year. Some further, more recent considerations, are listed below:

- Weak Consumer Demand: GDP data has shown a decline in consumer spending over the past four quarters. Japan's government recently cut its growth forecast for the fiscal year ending March 2025 to 0.9% from 1.3% due to weak consumer spending.

- External Demand Uncertainty: Global economic conditions remain uncertain, with potential economic slowdown and a risk of trade tariffs as US elections come into focus.

- Volatile Yen: The yen has shown significant volatility, moving from a 38-year low to a two-month high recently, likely due to the unwinding of some yen-funded carry positions. Sharp gains in the yen can be a headwind for the export-dependent Japanese economy, and last week’s move hammered assets from Japanese stocks to gold and Bitcoin as investors reassess their leveraged bets.

- Global Liquidity Impact: Sudden moves could destabilize global liquidity, given that Japanese investors hold a significant amount of global bonds.

- Recent Comments from Japan’s Ministry of Finance: The MOF recently noted that the BOJ officials should take into account commercial banks’ capacity to hold bonds, in deciding how much to cut bond purchases themselves. The finance ministry clearly seems to be tilting in favor of reducing bond purchases at a slow pace to avoid unsettling the market.

These reasons suggest that the central bank will proceed cautiously when it unveils its plan to cut bond buying at its policy decision meeting next week. This is the BOJ’s first step toward quantitative tightening after more than a decade of monetary easing.

Impact on Markets

Japanese Yen: Limited Room for Appreciation

The yen strengthened 2.4% against the dollar last week as carry trades funded in the currency rapidly unwound. This suggests that market has priced in some amount of BOJ normalization. As such, scope for further yen appreciation may be limited even if the BOJ was to go ahead with the dual move of a rate hike and bond tapering. Sustained yen appreciation, with USDJPY moving below 150, is also unlikely unless there is a significant rise in US recession risks or a sharp dovish turn from the Fed.

Meanwhile, if the BOJ did not meet the market’s high hawkish bar, yen slide could make a return. USDJPY could rise back above 155, and yen-funded carry trades could be back in vogue if BOJ signals caution. Latam FX still remains attractive for carry given that many central banks have halted their easing cycles. In Asia, the Indian rupee also offers an attractive carry with political jitters left behind. Within the G10 FX space, positioning for yen weakness may be considered against currencies like NZD where RBNZ rate cuts have been largely priced in.

Sustained yen weakness is also supported by technical factors, including:

- Options skew: The options market shows high volatility in yen options maturing in one week. But beyond that time frame, volatility is declining, suggesting a more stable market that may imply room for carry trading to be sustained and fizzling of the current yen rally.

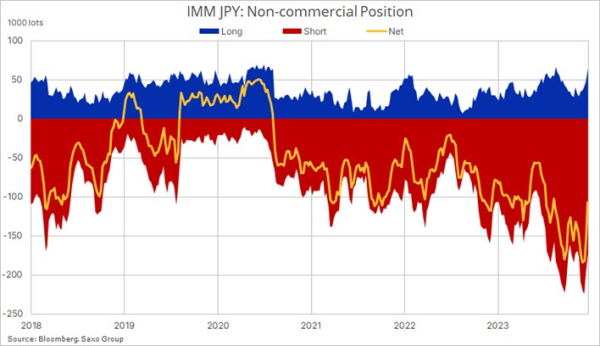

- CFTC Positioning: Real money managers and leverage funds have cut back on their net short positions in the Japanese yen recently. The latest CFTC data showed that the non-commercial net-short positioning in JPY has been cut by 42% to -107k in the week to July 23 from a record short in the week of July 2. Yet, there are few signs such positions will reverse anytime soon unless there’s any drastic changes for the BOJ’s policy towards tightening.

- Seasonality: July is a seasonally strong month for the yen, followed by several months of weakness for August through October based on data over the last five, ten or fifteen years.

Japanese Equities: Selective Exposures Could be Key

Japanese equities have a significant negative correlation to the Japanese yen, given the dominance of large exporters in the economy and the broader indices. A hawkish stance from the BoJ could therefore initially put downward pressure on Japanese equities, especially if it leads to a stronger yen, impacting exporters. Last week’s 2.4% acceleration in the yen led to a 6% decline in Nikkei 225.

This warrants a cautious stance on Japanese equities. Even if the BOJ remains cautious on normalization, there remain reasons to expect that the Fed will flag a September rate cut with the US economy losing momentum. This could lower the yield gap between the US and Japan’s yields, and lead to a rebound in the Japanese yen which could weigh on Japan’s broader equity indices.

However, structural tailwinds for Japanese equities are likely here to stay. This could call for more active management, with exposures tilted towards:

- companies that have high profitability and resilience to FX fluctuations

- domestic demand exposures with real wages accelerating

- dividend plays amid corporate governance reform to increase shareholder returns

- geopolitical plays or companies that get a tailwind form China+1 supply chain strategies

- -value stocks, and particularly financials, may benefit as BOJ’s policy normalization progresses in H2

- defense theme could continue to be relevant as US election related volatility increases

- structural themes like energy transition, nuclear and digitalization

Japanese Bonds: Higher Yields Could Attract Japanese Insurers

Clarity on the BOJ’s bond-buying plan would reduce uncertainty on Japan’s rate path and encourage insurers and pension funds to quicken their repatriation of capital on expectation that yields on Japanese bonds will rise.

A reduction in JGB purchases by the BoJ could lead to higher yields and lower bond prices. If the 30-year JGB yield moves above 2%, it will be attractive to life insurers, especially with US treasury yields easing and currency-hedging costs remaining significantly high.

Disclaimer: Forex, or FX, involves trading one currency such as the US dollar or Euro for another at an agreed exchange rate. While the forex market is the world’s largest market with round-the-clock trading, it is highly speculative, and you should understand the risks involved.

FX are complex instruments and come with a high risk of losing money rapidly due to leverage. 65% of retail investor accounts lose money when trading FX with this provider. You should consider whether you understand how FX work and whether you can afford to take the high risk of losing your money.

Recent FX articles and podcasts:

- 26 Jul: US PCE Preview: Key to Fed’s Rate Cuts

- 25 Jul: Carry Unwinding in Japanese Yen: The Current Dynamics and Global Implications

- 23 Jul: Bank of Canada Preview: More Cuts on the Horizon

- 16 Jul: JPY: Trump Trade Could Bring More Weakness

- 11 Jul: AUD and GBP: Potential winners of cyclical US dollar weakness

- 3 Jul: Yuan vs. Yen vs. Franc: Shifting Carry Trade Strategies

- 2 Jul: Quarterly Outlook: Risk-on currencies to surge against havens

- 26 Jun: AUD, CAD: Inflation Rising, Can Central Banks Stay on Pause?

- 21 Jun: JPY: Three-Way Pressure Piling Up

- 20 Jun: CNH: China Authorities Loosening their Grip, But Devaluation Unlikely

- 19 Jun: CHF: Temporary Haven Flows Unlikely to Fuel SNB Rate Cut

- 18 Jun: GBP: UK CPI Details and Elections Will Keep BOE on Hold

- 13 Jun: BOJ Preview: Tapering and Rate Hike Talk Not Enough to Boost JPY

- 10 Jun: EUR: Election jitters and ECB rate cut add to downside pressures

Recent Macro articles and podcasts:

- 25 Jul: Equity Market Correction: How to Position for Turbulence?

- 24 Jul: Powell Put at Play: Rotation, Yen and Treasuries

- 22 Jul: Biden Out, Harris In: Markets Reassess US Presidential Race and the Trump Trade

- 8 Jul: Macro Podcast: What a French election upset means for the Euro

- 4 Jul: Special Podcast: Quarterly Outlook - Sandcastle economics

- 1 Jul: Macro Podcast: Politics are taking over macro

- 28 Jun: UK Elections: Markets May Be Too Complacent

- 24 Jun: Macro Podcast: Is it time to diversify your portfolio?

- 12 Jun: France Election Turmoil: European Equities Amidst the Upheaval

- 11 Jun: US CPI and Fed Previews: Delays, but Dovish

- 10 Jun: Macro Podcast: Nonfarm payroll shatters expectations - how will the Fed react?

- 3 Jun: Macro Podcast: It is a rate cut week

Weekly FX Chartbooks:

- 22 Jul: Weekly FX Chartbook: Election Volatility and Tech Earnings Take Centre Stage

- 15 Jul: Weekly FX Chartbook: September Rate Cuts and the Rising Trump Trade

- 8 Jul: Weekly FX Chartbook: Focus Shifting Back to Rate Cuts

- 1 Jul: Weekly FX Chartbook: Politics Still the Key Theme in Markets

- 24 Jun: Weekly FX Chartbook: US Presidential Debate is the Big Market Unknown

- 10 Jun: Weekly FX Chartbook: US CPI and FOMC dot plot have a low dovish bar

- 3 Jun: Weekly FX Chartbook: ECB and Bank of Canada likely to cut rates

FX 101 Series:

- 15 May: Understanding carry trades in the forex market

- 19 Apr: Using FX for portfolio diversification

- 28 Feb: Navigating Japanese equities: Strategies for hedging JPY exposure

- 8 Feb: USD Smile and portfolio impacts from King Dollar