CAD vulnerable as market underprices dovish Bank of Canada risks

Hard landing risks loom

- Canada’s composite PMI has been in contraction for 10 months in a row, indicating a slowdown in economic activity.

- Labor market data for March showed net job losses and unemployment rate rising to 6.1%, the highest in 2 years.

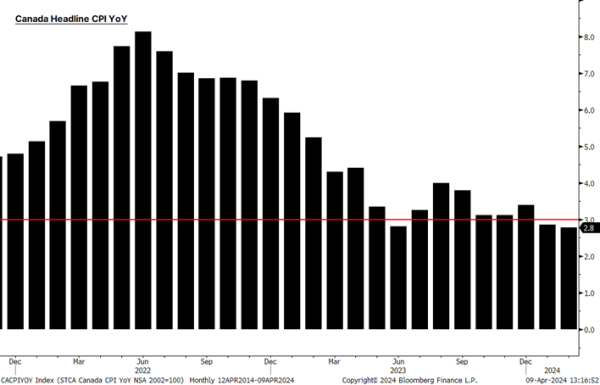

- February CPI eased to 2.8%, falling within the BOC target range of 1-3%. Core measure also eased to 3.1% in February and could come in at or below the 3% upper bound in March (due April 16).

- Q4 GDP growth was strong and January GDP also beat expectations. But this strength was aided by a rebound in education as Quebec strikes ended, as well as milder weather. BoC’s business survey reports the outlook remains “subdued”.

- The government is expected to make it difficult for firms to hire temporary works in an effort to reduce temporary resident numbers. This could also pose downside threats to growth and inflation.

- Canadian economy could face hard landing risks if the BOC opted to wait for the Fed to start rate cuts.

Market not positioned for BOC rate cuts

- Market sees less than 20% chance of a rate cut this week. This is a reminder of the SNB rate cut risk we flagged earlier in March. Note that BOC is more of a trend follower than the SNB, so the odds of a rate cut this week are still low, but not zero.

- Market also sees a just over 70% chance of a rate cut by June.

- Even if the BOC doesn’t view one month of labor data as a reason to start cutting interest rates yet, the economic outlook and forward guidance is likely to turn dovish.

CAD has room to weaken

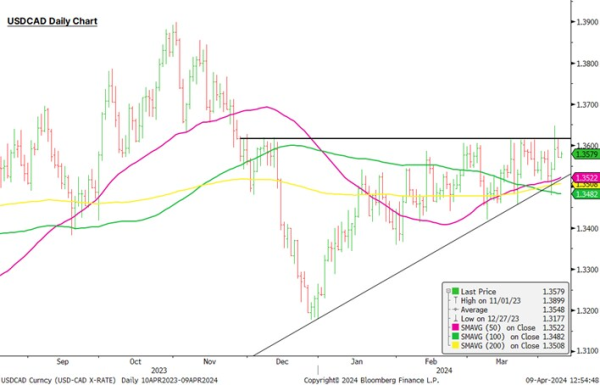

- USDCAD rose above the 1.3620 resistance following the Friday jobs release which highlighted economic divergence to the US where Fed members are reiterating patience on rate cuts.

- USDCAD saw cycle highs of 1.3899 in November, when oil prices were around the same $90/barrel mark. Oil prices are a weaker driver of CAD now, while focus is on yield differentials.

- USDCAD needs a clear break of 1.3620 to extend the upside.

- If BOC proves dovish, CAD weakness could be prominent against other commodity currencies that are likely to benefit from the US reflation theme such as NOK or AUD.

- CADNOK has reversed from 8.00+ levels and testing the cluster of moving averages just above 7.82.

- AUDCAD has moved above 100DMA and could extend gains to 0.90+ in case of a dovish BOC.

-----------------------------------------------------------------------

Other recent Macro/FX articles:

9 Apr: Global Market Quick Take - Asia

9 Apr: US inflation report: How to trade the event

8 Apr: Macro and FX Podcast: NFP, CPI, ECB and Japan

8 Apr: Weekly FX Chartbook: US CPI, geopolitics and dovish pivots from ECB and Bank of Canada in focus

3 Apr: Chinese yuan bears are undeterred by PBoC’s grip

25 Mar: Macro & FX Podcast: Swiss central bank surprises; PCE and China

25 Mar: Weekly FX Chartbook: The return of US exceptionalism

22 Mar: Swiss National Bank’s bold move will kickstart the G10 rate cut cycle

20 Mar: Thematic Podcast: Japan's route to abolish negative interest rates

20 Mar: Japan’s exit from negative rates: Implications for the economy, yen and stocks

19 Mar: FOMC rate decision: How to trade the event

18 Mar: Macro & FX Podcast: Central bank meetings all over

18 Mar: Weekly FX Chartbook: Heavy central bank focus as FOMC, BOJ, BOE, SNB, RBA meet

14 Mar: FOMC vs. BOJ: Who moves the Yen?

12 Mar: Dampening equity sentiment could test GBP resilience

11 Mar: US inflation report: How to trade the event

6 Mar: Bitcoin fever is running high, again

5 Mar: FX & Macro Podcast: US jobs data, China's "Two Sessions" & Super Tuesday

28 Feb: Navigating Japanese equities: Strategies for hedging JPY exposure

23 Feb: Nvidia momentum spills over to FX markets

21 Feb: Central bank divergence on the radar: Hawkish RBNZ, Dovish BOC and SNB

15 Feb: Swiss Franc’s bearish view gets more legs

14 Feb: Sticky US inflation could make dollar strength more durable

9 Feb: Japanese Yen is throwing a warning

8 Feb: FX 101: USD Smile and portfolio impacts from King Dollar