China/Hong Kong Market Pulse: Hong Kong Equity Rally Surpasses Global Markets; USDCNH Decline Signals Opportunity

Key Points:

- Hang Seng Index jumps 13.9%, outshining global counterparts.

- Speculated post-Politburo Meeting policies fuel Hong Kong equity surge.

- Strong performances in tech, healthcare, property, and insurance sectors drive gains.

- Investor sentiment likely to rise ahead of July's Third Plenary Session.

- Long USDCNH amid China's FX reserve decline relative to money supply and US-China trade tension in a US election year.

The Outperformance of the Hong Kong Equity Market Since April 19

The Hang Seng Index surged by 13.9% over the past two weeks, outperforming the S&P 500's 3.2% and the Nikkei 225's 3.2%, as well as the Nasdaq 100's 5%, the Euro Stoxx 50's 0.1%, and topping the performance of major global equity indices. Its price/earnings ratio (P/E) rallied from around 8 times two weeks ago to slightly above 9 times during the same period. The low valuation and the underweight positions taken by many benchmark-driven investors, partly due to fundamental reasons and partly in response to the multi-year underperformance of the Hong Kong equity market compared to the rest of the world, provided a breeding ground for a rally. Over the same two weeks, the Hang Seng China Enterprises Index gained 13.9% and its P/E bounded from around 7.5 times to 8.5 times. The Hang Seng Tech Index surged by 21.2%, with the P/E rising from around 15 times to over 18 times.

The mainland market lagged behind Hong Kong, with the CSI300 gaining less than 2% over the past two weeks. Despite the Chinese market being closed on May 2 and 3, while the Hong Kong market remained open, the notable outperformance of the Hong Kong market against the mainland market continued. The strong performance in large-cap China tech, healthcare, property, and insurance stocks, which have a larger weight in Hong Kong indices than their mainland counterparts, helped drive the outperformance. Southbound flows of mainland investors buying Hong Kong stocks through the Stock Connect have been consistently positive since the week ending February 9.

While consensus earnings revisions for the current reporting season have been marginal, with only a modest 0.3% upward revision for the MSCI Hong Kong Index, they fared better than the 1.4% downward revision for the MSCI China Index. Northbound flows through Hong Kong for purchasing A shares remained negative for most of April until they reversed to become positive over the past two weeks.

China’s Politburo Meeting Last Week

Following China’s Politburo Meeting held last week on April 30, the mainland A-share market is expected to react upon its reopening after the three-day Labour Day holiday. The Hong Kong market, which remained open during this period, experienced significant gains on May 2 and 3 in response to the readout from the meeting. Speculations regarding favorable policies concerning the property market and the broader economy fueled this rally.

The most significant takeaway from the politburo meeting is the announcement of the convening of the Third Plenary Session in July. This suggests that a consensus has finally been formed within the Chinese leadership on strategic directions and implementation measures for the economy over the next five years. General Secretary Xi’s decision to unveil this plan alleviates previous uncertainty surrounding the meeting's delay, which typically outlines China's economic development strategy. Investor sentiment may improve leading up to the Third Plenary Session in July, potentially setting the stage for disappointment if it fails to introduce significant reform initiatives. The meeting’s focus may primarily centre on accelerating the implementation of existing policies due to limited space for introducing new reforms.

Regarding the property sector, the Politburo meeting's statement mentioned not only the focus on completing the construction of pre-sold housing properties but also for the first time a top-leadership directive to coordinate national and cross-ministries efforts to resolve the inventory overhang in the housing sector. Equity market investors interpreted this as increasing the probability of local governments being asked to acquire housing inventories from developers through local government financing vehicles (LGFVs) and other government-controlled investment entities, such as recent cases in Zhengzhou and Nanjing. However, it is not clear how this purchase will be financed and implemented without adding to the already stressed financial resources of local governments and how to avoid moral hazards.

As of March 2024, the national inventory cycle for new residential properties in 100 cities is approximately 25 months. Following the April 30th Politburo meeting, the General Office of the Ministry of Natural Resources promptly issued a notice to restrict the supply of land to be used for building new residential properties. The notice requires cities with inventory cycles exceeding 36 months to temporarily suspend the sale of land until the inventory cycle for residential properties is reduced to below 36 months; for cities with inventory cycles between 18 and 36 months, they are allowed to sell the amount of land for replacement of the property inventory successfully sold. The restrictions on land supply may help marginally, but the key issue is that the amount of housing inventory is too large for the weak demand for housing and will take a long time to clear. Along the way, distressed and overextended developers will go bankrupt.

Strong Momentum in the Near Term but Medium-term Challenges Remain

Given the underweight of many institutional investors and the fact that outperformance will by itself draw further momentum chasing buying, the momentum in the Hong Kong equity market may have more upside in the near term. As discussed above, the mainland A-share market is likely to rally this week after returning from a long holiday and has the opportunity for the first time to react to the perceived favorable messages from the Politburo meeting held just before the holiday. However, it was one thing to rebound from 8 times PE two weeks ago and another thing to sustain the rally beyond 10 times PE without a pick-up in earnings growth forecasts. It would be even more challenging for the CSI300, which is already trading at 13 times the 2024 earnings estimate. After the initial hype, the incremental support to the housing sector and the potential lack of policy space for more economic reforms and stimulus measures are poised to disappoint investors this summer. The medium-term challenges of structurally lower productivity and trend growth during the transformation of the economic development model and the potential intensification of the trade war between the U.S. and China in the U.S. election year remain elevated.

While strong performance in exports in both the official manufacturing PMI from the National Bureau of Statistics and the private Caixin manufacturing PMI for April stirred up some optimism about an improvement in the export sector, there will be limits for China to shift its trade pattern to export more, especially intermediate and capital goods to countries such as Mexico, Vietnam, Canada, South Korea, Thailand, India, and others, while these countries increase their exports of finished products to the U.S. As the US-China trade tension is likely to intensify, this kind of indirect export through changes in trade flows and patterns may hit its limit. As discussed in this previous Saxo article, the trade war between the US and China will be an important campaign issue for the November US presidential and congressional elections. In addition, the national security-driven US restrictions on semiconductor technology have expanded to a wider derisking in supply chain reliance and data security regarding Chinese solar energy and wind power equipment supply, electric vehicles, batteries, biotechnology, and social media.

What Investors Bought through Stock Connect before the Chinese Long Holiday

As the mainland market resumes trading today and the channel for mainland investors to buy Hong Kong stocks and overseas investors to buy mainland A shares resumes, it could be worthwhile to review some of the stocks that investors have been buying in April as a reference. In terms of percentage of market capitalization, top buying by mainland investors of Hong Kong stocks via the southbound Stock Connect included China Resources Power, China Hongqiao, Hong Kong Exchanges, Shengzhou International, Bank of China, China Resources Land, China Pacific Insurance, Yankuang Energy, CGN Power, Kuaishou Technology, Tsing Tao Brewery, Li Auto, and Xiaomi. Through the northbound Stock Connect, overseas investors bought A shares in BOE Technology, Jiangxi Copper, Eastroc Beverage, Will Semiconductor, Haier Smart Home, China Vanke, Luxshare Precision, Ping An Bank, Industrial Bank, and Yunnan Baiyao Group.

USDCNH below 7.20 Presents a Long Dollar/Short CNH Opportunity

The USDCNH fell by 0.9% from 7.2548 on April 30th to close at 7.1928 on May 3. However, during the same period, the CNHJPY weakened by 2.1% from 21.74 to 21.28. The decline in the USDCNH was primarily a derivative of weakness in the dollar against the yen instead of any intrinsic strength in the renminbi against the dollar. Japan's Ministry of Finance reportedly intervened on April 29 and again on May 1 to reverse he decline of the yen, selling over USDJPY57 billion. This was not fundamentally a sudden reversal in the renminbi or the beginning of a strengthening trend for the renminbi.

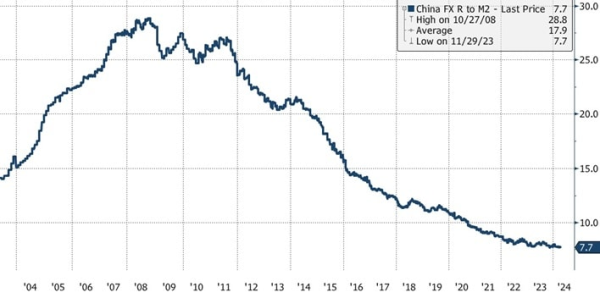

The recent decline in the USDCNH provides a good entry level for new long positions in the currency pair. China's FX reserves as a percentage of broad money supply, M2, have declined from over 20% ten years ago to just around 7.7% currently (Figure 1). FX reserves have hovered around USD3-3.2 trillion since 2016, while China's M2 has doubled since then. Given the desire for the Chinese leadership to grow the money supply to support the economy, the bullet that the PBoC has to stop a sharp depreciation of the renminbi versus the dollar will be very limited. A drop in its FX reserve to below USD 3 trillion worsens the situation as it jeopardizes investors' confidence in the sufficiency of China’s FX reserve.

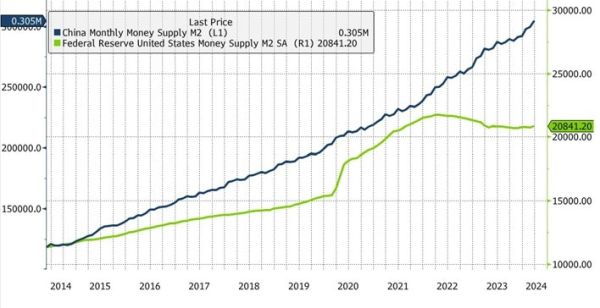

Before the peak of China's foreign exchange reserves in 2014, the issuance of the renminbi was effectively backed by the accumulation of foreign currencies, mainly the US dollar, from rapid increases in export proceeds. As China’s FX reserves grew fast then, the People's Bank of China (PBoC) had to raise the reserve requirement ratio (RRR) to as high as 22% at one point to prevent China’s money supply from rising too fast. This has changed since 2015 as the accumulation of foreign currency from exports has slowed. The PBoC had to cut the RRR numerous times to a weighted average across large and small banks to 7% to grow the money supply to support the economy. Growth in China’s M2 has been much faster than the U.S., especially over the past two years (Figure 2). This is also one of the reasons why the monetary policy space for the PBoC to further expand China's M2 growth without affecting the value of the renminbi is a challenge.

Since 2014, the PBoC has utilized lending through Medium-term Lending Facilities (MLF) and Pledged Supplementary Lending (PSL) to inject the monetary base into the banking system to supplement the growth in the money supply. With the need for more tools for the PBoC to manage China’s money supply at a time when its FX reserve is not growing and the RRR has been reduced to relatively low levels, the Chinese leadership, including General Secretary Xi, is asking the PBoC to become more active in trading Chinese government bonds in the secondary market. While the law on the PBoC forbids China’s central bank to buy government bonds in the primary market, it is allowed to do so in the secondary market. Historically, the PBoC seldom did that. Going forward, however, it may be buying government bonds more often and it may shift at the margin, the effective backing of China’s money supply from currencies such as the dollar and euro to Chinese government bonds. If it happens on any significant scale, which is not in the foreseeable future, it may potentially put downward pressure on the renminbi. Moreover, China may not resist a decline in its currency against the USD, as the renminbi has appreciated against the Japanese yen by about 46% over the past four years while depreciating against the USD by only 14% since 2021, and in fact remaining nearly unchanged from the level of four years ago in 2020. As long as the depreciation against the dollar is gradual and not disorderly, a weakening of the renminbi may be a welcome development for Chinese authorities.

Buying USDCNH may be an attractive trade in terms of risks and rewards, while chasing Hong Kong equities may be riskier.

Selective recent China/Hong Kong focussed articles:

2024-03-19 US Election: Shaking Up Chinese Equities and the Renminbi?

2024-03-06 China/Hong Kong Market Pulse: Two Sessions Spark Divergent Market Reactions in Mainland and Hong Kong

2024-03-04 China/Hong Kong Market Pulse: Decoding Expectations about the Two Sessions

2024-02-06 China/Hong Kong Market Pulse: The Stormy Waters of the Chinese Equity Market

2024-01-15 Taiwan Elections Aftermath: Markets May Find Relief from Another Four Years of DPP Presidency Hampered by a Hung Legislature

2024-01-12 Taiwan's 2024 Elections: Balancing Geopolitical Realities and Economic Pragmatism

2024-01-09 Investing in China: Navigating Q1 amid economic challenges

2023-11-07 China/Hong Kong Market Pulse: Central Financial Work Conference Unveils Near-Term Bullish Signals

2023-10-12 China/Hong Kong Market Pulse: Central Huijin Increases Stakes in the Four Largest SOE Banks

2023-10-09 China/Hong Kong Market Pulse: Evaluating the Potential Rebirth of Pro-Market Reforms

2023-09-27 China/Hong Kong Market Pulse: Property Debt Overhang, Recovery Signs, and Policy Outlook