Commodities Watch: Brent Crude back at Dec 2021 low, gold remain above US$2,500

Round-up

The past week has seen market participants broadly leaning on the defensives, as weak seasonality, uncertainty over the US presidential race and mixed economic data may seem to limit appetite for risk-taking. Clues for the Federal Reserve (Fed)’s next move continue to be highly sought, with any validation for the current 25 basis point (bp) market rate pricing likely to offer more calm for markets.

Attention will be on the US inflation data ahead. Further disinflation is likely to be the story but with the balance of risks now shifting towards growth, any significant downside surprise will not be reassuring by highlighting weaker domestic demand. Expectations are for headline inflation to ease to 2.6% year-on-year from 2.8% prior, with core inflation unchanged at 3.2%.

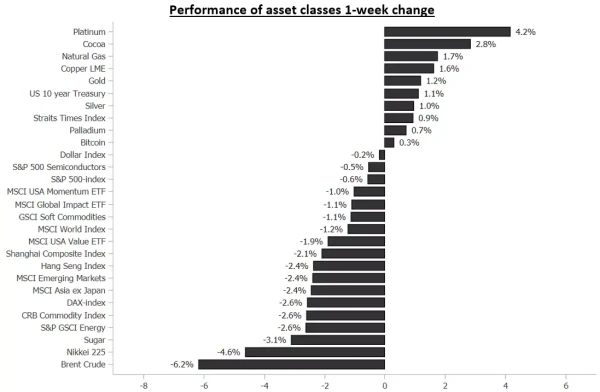

In the commodities space, platinum prices pulled ahead with a 4.2% gain for the week. Cocoa prices were up 2.8%, while natural gas edged 1.7% higher. Notably, gold prices have held up around its record high, defending its key US$2,500 level amid a 1.2% weekly gain. On the other hand, Brent Crude prices disappoint with a hefty 6.2% plunge, dipping to its lowest level since December 2021.

Brent crude: Lowest level since December 2021

Having traded in a broad descending triangle pattern since September 2022, Brent Crude prices have plunged through the lower trendline level at the US$71.40 level in today’s session and registered its lowest level since December 2021. Thus far, market participants have looked beyond geopolitical tensions in the Middle East, as the conflict proved to be contained with minimal supplies disruptions.

Greater focus has revolved around the prolonged weaker demand outlook from China and rising supplies from higher US oil production and a gradual restoration from OPEC+. More recently, OPEC has cut its forecast for global oil demand growth in 2024 and trimmed its expectation for next year, marking the producer group's second consecutive downward revision.

The broader bearish bias for oil prices remain, with its daily relative strength index (RSI) struggling to cross back above its mid-line. Further downside may leave the US$65.87 level on watch, which marked its previous horizontal support back in August 2021 and December 2021. On the upside, the US$71.40 level now serves as a key support-turned-resistance to watch.

Spot Gold: Defending its US$2,500 level

Gold prices remain resilient above its US$2,500 level, hovering near record high territory with a break above its previous consolidation range seemingly leaving the US$2,685 level on watch as an eventual price target. Its daily RSI continues to trade above the mid-line as a reflection of buyers in control, alongside various trend indicators (50-day, 100-day, 200-day moving averages (MAs), daily Ichimoku Cloud).

The latest Commodity Futures Trading Commission (CFTC) data revealed net positioning among money managers at its highest net-long positioning since March 2020. Any downside may leave the US$2,480 level on watch, which buyers have defended so far on two occasions since August this year.