Commodities weekly: Calm returns to markets, including raw materials

Key reports from Saxo Analysts during a week of turmoil, and ultimately calm:

Equities: The perfect storm hits markets and what comes next?

Commodities: Position reduction in focus as volatility spikes and US growth slows

Forex: BOJ’s back to being dovish – Can it cool the yen short squeeze?

Bonds: Stable spreads and robust insurance make a 50 bps September cut unlikely

Macro: US economy soft landing hopes vs. hard landing fears

Key points in this update:

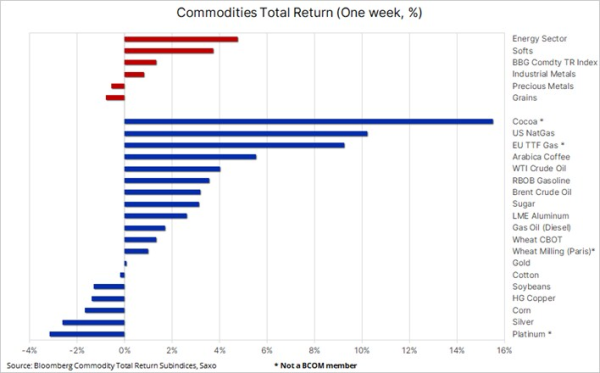

- Following a week of turmoil, the commodities sector is heading for its first weekly gain in five.

- Strong gains in natural gas, crude oil, cocoa, and coffee are offsetting some weakness in silver, copper, and soybeans.

- US and European natural gas, as well as crude oil, all trade higher as focus turns to supply.

- Copper's growing stockpile problem remains a major drag on prices and sentiment.

- Gold's resilience underpins support as current developments unfold.

This week in financial markets was marked by significant volatility, starting with turmoil reminiscent of 2020 and ending on a calmer note. Weak US data in July, coupled with the surprise rate hike from the Bank of Japan (BoJ) on July 31, triggered what can best be described as a momentum crash. The dovish Federal Open Market Committee (FOMC) message, along with last week's weak US data, altered market sentiment, leading traders to worry that central banks might be repeating historical errors by delaying interest rate cuts and then moving too slowly once they start.

On August 2, a weak US jobs report sparked discussions that the Federal Reserve might have erred by keeping interest rates too high for too long. This concern exploded on Monday, leading to significant risk reduction and a historic 12% drop in Japanese equities, driven by the unwinding of positions funded by cheap yen. The BoJ's surprise rate hike last week, accompanied by hawkish comments, disrupted the yen and funding markets, leading leveraged investors to reduce their cross-market exposure, including in commodities.

After an initial drop due to deleveraging, which impacted long gold positions and hurt the energy and industrial metal sectors, the week ended more calmly. This allowed traders to focus on sector-specific developments rather than being driven solely by sentiment. The Bloomberg Commodity Index was on track for its first weekly rise in five weeks, with strong gains in natural gas, crude oil, cocoa, and coffee, offsetting some weakness in silver, copper, and major grain contracts.

US and European natural gas surge

Dutch TTF gas, the European benchmark, reached its highest level this year due to renewed fears of possible disruptions to the remaining pipeline supplying Russian gas to Europe via Ukraine. Over the past month, prices have risen steadily, reaching EUR 40 per MWh for the first time since December, driven by temporary disruptions in Norwegian gas flows due to maintenance and increased competition for LNG cargoes from Asia. These developments have slowed seasonal stock building ahead of winter, but with inventories at 86.7% full, there is limited risk of not reaching desired levels before demand eventually exceeds supply. However, any major disruption in the coming months would heighten the need for alternative supplies, primarily via LNG, driving up prices as Europe competes with Asia and South America.

US natural gas also recovered strongly after finding support below USD 2 per MMBtu, subsequently breaking the downtrend that had prevailed since June. Prices are currently supported by an improved technical outlook, a 3.6% production cut this month, and weekly inventories rising at a slower-than-expected pace, reducing the current storage surplus relative to long-term averages.

Stabilising markets allow crude traders to focus on supportive fundamentals

Crude oil began August on the defensive, with prices suffering additional losses on top of those seen last month. The market was dominated by concerns over Chinese demand and increased focus on whether the US economy can avoid a recession. The recent loss of risk appetite across key stock market sectors culminated in a major deleveraging move out of short yen positions, sending shockwaves across global markets, including commodities.

Supply risks remain a concern, particularly with the halt in production from Libya’s biggest field, geopolitical tensions surrounding Ukraine's cross-border attack on Russia, and Iran’s promise to retaliate against Israel for a recent assassination in Tehran. Despite these threats, the market has so far seen a limited reaction, with reports suggesting that Iran wants to avoid a region-wide war that could disrupt oil and gas flows from the Middle East.

OPEC+ is increasingly likely to defer the planned October production increase given the current fragility and negative sentiment from outside developments. Additionally, with the North Atlantic hurricane season underway, the risk of disruptions to crude production or refining presents an underlying source of support for prices.

Brent crude hit the bottom of a long-held range between USD 75 and USD 90 per barrel this week. However, stabilizing markets, geopolitical tensions, a continued drop in US crude stocks, and a technically oversold market condition helped support a small and ongoing recovery. Considering current and potential future developments, the market may hold current support levels, but the upside potential appears limited to the mid-80s.

Copper’s stockpile issues

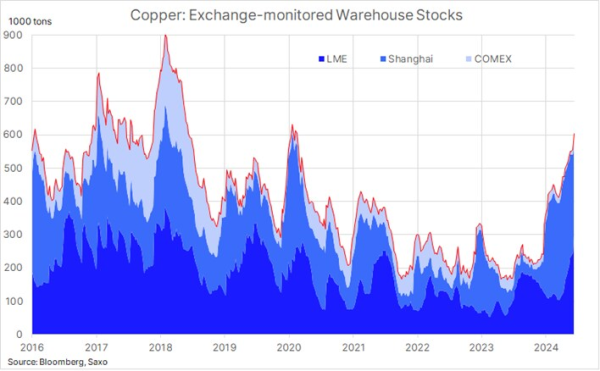

Since reaching a record high of USD 5.2 per pound in late May, High Grade copper has slumped 20%, with most of the decline occurring over the past month as China's demand outlook deteriorated and US data increasingly pointed to a slowdown. The second quarter in China typically sees industrial activity pick up after winter and the Lunar New Year holiday, but this year has been different. Inventories monitored by major futures exchanges have continued to rise rapidly, signaling a major supply-demand mismatch due to weak demand.

Total stocks at warehouses monitored by the London and Shanghai exchanges have risen to levels not seen since the pandemic's early days in 2020. After an initial rise in Shanghai, where the overhang was most pronounced, material began flowing into LME warehouses in South Korea and Taiwan. This culminated this week when the LME reported the biggest one-day inflow since 2019, bringing total LME-monitored stocks near 300k tons, further unnerving remaining bulls. Monday’s deleveraging-led mini-crash and volatility spike only added to the negative sentiment, which at best suggests a period of consolidation until fundamentals improve.

Five consecutive weeks of selling have returned HG copper to around USD 4 per pound. Technically, support is seen near USD 3.85 per pound, aligning with the trendline from the 2020 low and the consolidation area that existed for several months before the move higher earlier this year. The first sign of stabilization would likely require a move back above the 200-day moving average, currently at USD 4.11, followed by the recent high at USD 4.2235. It is also worth noting that speculators since May when their net long reached a 40-month have cut their exposure by 87%, with none of the reduction being driven by fresh short-selling.

Gold’s resilience amid turmoil

Gold, and to a lesser extent silver, remains a go-to metal amid the current turmoil. However, given the exposure concentration by leveraged funds, gold has not been immune to selling as funds cut their overall positions. The latest Commitment of Traders Report highlighted this concentration, with nominal net-long exposure in gold amounting to USD 46 billion, followed by crude oil (WTI & Brent) at USD 22 billion, and coffee (Robusta & Arabica) at USD 6 billion.

We maintain a positive view on gold as a diversifier hedge against turmoil elsewhere. If the Federal Reserve begins cutting rates, potentially as early as next month, interest rate-sensitive investors may return to gold via ETFs, which have seen consistent net selling since 2022 when the FOMC began its aggressive rate-hiking campaign. In addition, we have in this recent update mentioned several other factors currently supporting an investment in precious metals.

Recent commodity articles:

8 Aug 2024: Sentiment-driven crude sell-off eases, allowing traders to focus on supply risks

7 Aug 2024: Limited short-selling interest observed during copper's recent aggressive correction

6 Aug 2024: Video: What factors are fueling the current market turmoil and gold's response

5 Aug 2024: COT: Broad commodities sell-off gains momentum; Forex traders seek JPY and CHF

5 Aug 2024: Commodities: Position reduction in focus as volatility spikes

2 Aug 2024: Widespread commodities decline in July, with gold as the notable exception

31 July 2024: Crude's month-long slide halted by fresh Mideast worries

30 July 2024: Record demand explains gold's current resilience

29 July 2024: COT: Energy and metals selling cuts hedge fund long to four-month low

4 July 2024: Sluggish US economic indicators boost demand for gold and silver

4 July 2024: Podcast Special: Quarterly Outlook - Sandcastle Economics

2 July 2024: Quarterly Outlook - Energy and grains in focus as metals pause

1 July 2024: COT: Crude long builds ahead of Q3 while grains selling accelerates

28 June 2024: Metals and natural gas propel commodity sector to quarterly gain

26 June 2024: Crude seeks support from seasonal demand strength

24 June 2024: Copper's resilience despite China weakness

18 June 2024: Precious metals go through prolonger period of consolidation

17 June 2024: COT: Dollar long jumps; Funds start rebuilding crude long

14 June 2024: Commodity weekly: Energy sector gains counterbalance metal consolidation

13 June 2024: Oil prices steady amid divergent OPEC and IEA demand projections

10 June 2024: COT: Brent long cut to ten-year low; metals left exposed to end of week slump

3 June 2024: COT: Crude length added before OPEC+ meeting; gold and copper see profit-taking