Commodities weekly: Metal strength counterbalancing weakness in the energy and grain markets

Key points in this update:

- A softer dollar and lower US Treasury yields supported risk appetite ahead of Powell's Jackson Hole speech

- The industrial metal sector, led by aluminum, turning higher but improved fundamentals still needed

- Gold's continued surge underscores a world out of balance

- Falling fuel prices highlight crude's current demand challenge

- Persistent supply constraints keep cocoa prices elevated

Global financial markets continue to recover from the early August turmoil, supported by better-than-expected US economic data, reducing fears of a severe downturn in the world's largest economy and thereby easing pressure on the Federal Open Market Committee (FOMC) to implement deep interest rate cuts. However, China, the world's top consumer of commodities, remains weak due to a persistent property slump, rising unemployment, and weak consumption.

A softer dollar and lower US Treasury yields supported risk appetite ahead of a long-awaited speech from Fed Chair Powell at the annual Jackson Hole Economic Symposium. The speech comes at a crucial time for US monetary policy, as the Fed is nearing a shift from the high-interest-rate environment it kicked off in 2022 in response to a post-Covid inflation surge, which is now getting under control. The market has priced in a succession of rate cuts starting next month, and traders will be looking to Powell for confirmation that this is the correct approach. (Note: Given the timing of the speech at 2 p.m. GMT on Friday, 23 August, this update was written before the details became available.)

The combination of a softer dollar, lower Treasury yields, and the expected beginning of a US rate-cutting cycle continues to support the metals sector, with gold reaching a fresh record this past week before some buying fatigue led to consolidation. Meanwhile, industrial metals, led by aluminum, staged a comeback after the June to early August correction showed signs of having run its course. The energy sector, however, remains challenged by slumping product prices, pointing to softening demand for crude oil—a development potentially worsened by the prospect of an expected pickup in supply from OPEC and non-OPEC producers ahead of year-end. Still, both WTI and Brent continue to find buying interest ahead of key support.

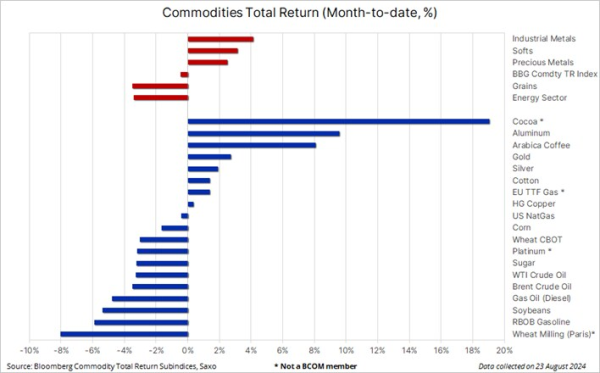

Overall, the Bloomberg Commodity Total Return index trades small down on the month and up 0.5% on the year, with losses in energy and continued weakness across an oversupplied grains market being partly offset by the mentioned strength in precious and not least industrial metals as well as the softs sector where cocoa and coffee is having a strong month amid tight supply caused by adverse weather in key growing regions.

Gold’s continued surge underscores a world out of balance

For the fifth time this year, gold managed to breach a previous high to set a new record at USD 2,531.75 on spot gold and USD 2,570.40 on the December gold futures. Note that the price difference between spot gold and the December contract reflects the cost of funding a position in the period between the two delivery dates. It roughly equates to an annual rate of 5.3%—a rate and spread that will start to come down once the FOMC begins to cut rates.

As we have highlighted in previous updates this year, we are seeing several drivers supporting an ongoing rally in gold, and unfortunately, several of these relate to buyers seeking a hedge against what can best be described as a troubled world. Examples of this include geopolitical issues, from armed conflicts and trade wars to central banks buying gold to reduce their dollar dependency, high levels of debt raising concerns about a credit event, and weakening economies such as China’s.

Gold remains an alternative asset that doesn’t offer a yield or dividend like traditional investments in bonds and stocks. Additionally, the level of short-term interest, which has been relatively high since 2022, has provided a negative carry as highlighted above, meaning investors had to rely on the price appreciating to achieve a return.

Despite these obstacles, which now finally show signs of easing, gold nevertheless managed to climb 13% last year and 21% so far this year, highlighting demand from investors that are not rate- and dollar-sensitive. Having reached a fresh record high above USD 2,500, the short-term attention—depending on the outcome of Powell’s speech—may turn to consolidation. However, with the mentioned supportive drivers not going away, the prospect of a succession of rate cuts, and with that, renewed demand from interest rate-sensitive investors through exchange-traded funds, could see gold trade even higher.

The biggest short-term risk is the risk of a buyer's strike from investors and central banks looking for a setback before adding exposure. In the short term, traders will be looking for support around USD 2,470-2,475, but overall, the yellow metal can fall USD 100 towards USD 2,400 without challenging the bullish setup.

Falling fuel prices highlight crude’s current demand challenge

Crude oil is heading for a weekly loss as falling product prices point to soft demand, potentially worsened by the prospect of an expected pickup in supply from non-OPEC producers ahead of year-end. So far, however, both WTI and Brent have managed to find support ahead of key levels around USD 71 and USD 75, respectively. While the geopolitical risk premium ebbs and flows, the crude oil market faces ongoing pressure as China’s economic slowdown and the rise of EVs and hybrid cars reduce fuel demand, leading to lower refinery activity. However, weak refinery margins in Europe and the USA, dampening crude demand, make it increasingly unlikely that OPEC+ will unwind voluntary cuts in October.

Since OPEC+ announced a 2 million bpd production cut in October 2022, Brent has traded mostly sideways, averaging USD 83.30. While OPEC+ has stabilized prices, this has also encouraged non-OPEC+ production, now complicating efforts to increase output without harming prices. As mentioned, Brent and WTI both revisited key support levels that were challenged at the start of August, and with the risk of a potential 5-10% downside extension on a break, the focus will remain firmly on OPEC+ and their ability to stick with current agreements to keep production capped, especially considering forecasts pointing to a surplus in 2025.

Copper rally stalls as stock levels remain elevated

Copper futures in London and New York traded higher for a second week, supported by fresh demand from momentum buyers and renewed demand from hedge funds that, during the recent and deep 24% correction, had cut their net long exposure in High-Grade futures by 90% to near neutral. Strike action at BHP’s Escondida mine in Chile, the world’s largest, helped kickstart the rebound amid fears of supply disruptions supporting tighter market conditions.

However, prices continued higher after BHP reached a deal with workers, but so far, the rebound has been relatively muted while aluminum raced higher, in the process recouping around half of the May to July 21% loss. We believe the worst of the correction is over, but before copper can mount a stronger recovery, demand fundamentals need to improve, potentially supported by restocking through lower funding costs once the FOMC starts its long-awaited rate-cutting cycle.

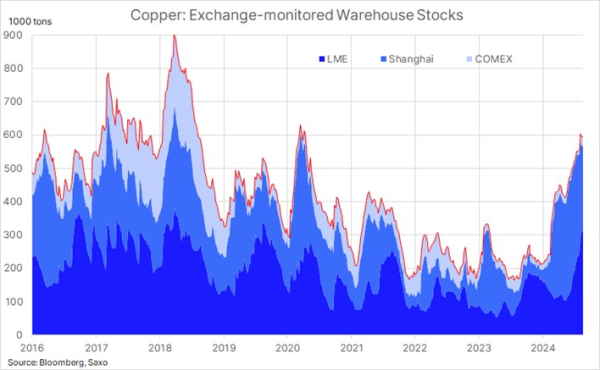

Until then, traders will continue to look out for signs of improvement, not least through the reduction of elevated stock levels at warehouses monitored by the three major futures exchanges. Since peaking at 337k on 7 June, SHFE-monitored stocks have declined by 86k to 251k, while LME has jumped by 192k to 315k and CME by 16k to 28.4k, leaving the market amply supplied, thereby reducing the short-term prospect for a sustained price recovery.

From a technical standpoint, the rally has paused after meeting resistance at the early August highs at USD 4.22 per pound in New York and USD 9,320 per ton in London. A break would open up for an extension to USD 4.31 and USD 9,500, respectively.

Persistent supply constraints keep cocoa prices elevated

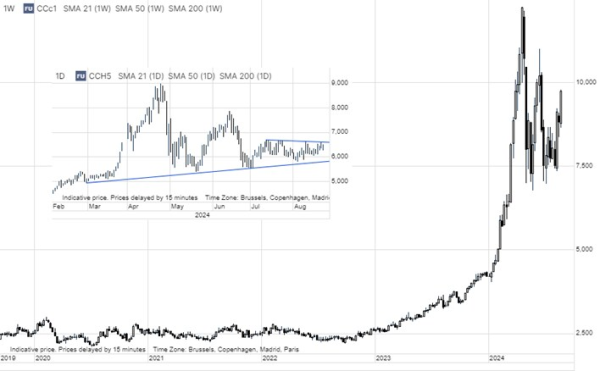

Cocoa prices have experienced a significant rally in 2024, driven by a combination of supply shortages, primarily due to adverse weather and crop diseases in West Africa, increased demand, and market volatility leading to panic buying. After reaching an all-time-high above USD 12,000 back in April, nearly five times the long-term average, the New York futures contract has since gone through a period of consolidation with support emerging on several occasions in the USD 6000 area, before rallying by 19% this month to USD 7600.

The latest jump has been supported by a prolonged supply worry, after the Ghana Cocoa Board reduced its harvest outlook for 2024/25 by 20% citing ongoing weather concerns. The main crop harvest season in West Africa normally runs from October to March while a smaller mid-crop harvest is collected between April and September. The March cocoa contract (see insert below) which includes deliveries from the upcoming main harvest season, trades around USD 1300 below the current futures price, and while it highlights a lower price amid upcoming supply, it also reflects a market still concern whether the production will be big enough to meet demand.

Earlier this week I rejoined Erik Townsend on Macro Voices where we discussed the latest developments across the commodities sector, and with the outset in our “Year of the metals” theme we took a closer look at gold, silver and copper as well as drawing a few parallels between the recent weakness in copper and uranium, two green transition themes. Also crude oil and agriculture in focus.

Recent commodity articles:

21 Aug 2024: Weak demand focus steers crude towards key support

19 Aug 2024: Resilient gold bulls drive price to fresh record above USD 2500

19 Aug 2024: COT Buyers return to crude as gold stays strong; Historic yen buying

16 Aug 2024: Commodities weekly: Gold strong as China weakness drags on other markets

9 Aug 2024: Commodities weekly: Calm returns to markets, including raw materials

8 Aug 2024: Sentiment-driven crude sell-off eases, allowing traders to focus on supply risks

7 Aug 2024: Limited short-selling interest observed during copper's recent aggressive correction

6 Aug 2024: Video: What factors are fueling the current market turmoil and gold's response

5 Aug 2024: COT: Broad commodities sell-off gains momentum; Forex traders seek JPY and CHF

5 Aug 2024: Commodities: Position reduction in focus as volatility spikes

2 Aug 2024: Widespread commodities decline in July, with gold as the notable exception

31 July 2024: Crude's month-long slide halted by fresh Mideast worries

30 July 2024: Record demand explains gold's current resilience

29 July 2024: COT: Energy and metals selling cuts hedge fund long to four-month low

4 July 2024: Sluggish US economic indicators boost demand for gold and silver

4 July 2024: Podcast Special: Quarterly Outlook - Sandcastle Economics

2 July 2024: Quarterly Outlook - Energy and grains in focus as metals pause

1 July 2024: COT: Crude long builds ahead of Q3 while grains selling accelerate