Crude oil surge caps strong four-week rally for commodities

Key points

- The commodities sector trades up by 9.3% in the last four weeks on broad gains across all sectors.

- The rally is supported by US rate cuts, China stimulus, and now higher oil prices, as the market awaits Israel’s response

- Precious metals remain short-term torn between geopolitics, lower US cut expectations and buying fatigue in the physical market

- An Israeli strike against Iran may trigger several different outcomes, most of which will be short term oil price supportive

The commodities sector traded higher for a fourth week last week, and so far this week has started with gains, primarily supported by the energy sector, where the risk of an Israeli retaliation attack on Iran continues to lift prices, with Brent honing in on the important USD 80 level. In the process, this supports a bid across the fuel sector, where especially the distillate contracts have received a bid from wrong-footed short sellers who, up until recently, focused on sluggish demand. However, China stimulus, the Middle East escalation, and robust US economic data have forced a rethink.

The Invesco Bloomberg Commodity UCITS ETF, shown below, is one of several ETFs tracking the performance of 24 major futures markets included in the Bloomberg Commodities Total Return Index, spread almost evenly across energy, metals, and agriculture sectors. Following the massive run-up between the COVID days in 2020 and the Russian invasion of Ukraine, the index retraced around half those gains before trading sideways for almost two years.

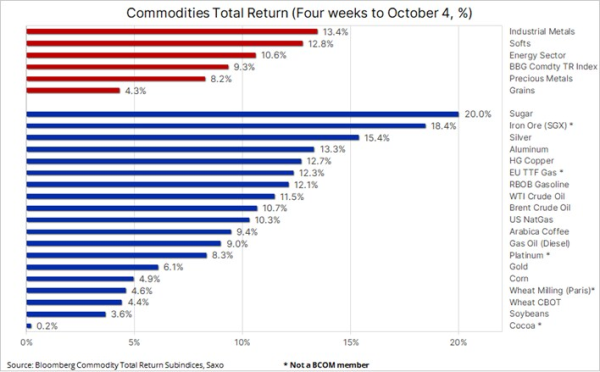

During the mentioned four-week period, the BCOM TR Index has risen by 9.3%, with not a single commodity trading down during this period. Note that several commodities in the table did not contribute to the mentioned gain, as they are not included in the index. The most relevant being iron ore, which jumped 18.4%, EU gas, platinum, Paris milling wheat, and cocoa. While weather worries were a constant throughout the month, supporting a strong short-covering rebound across the grains sector and a big jump in sugar, it was three major events that helped set the overall positive tone:

- The US Federal Reserve kicked off the rate cut cycle with a bumper 50 basis-point cut, a move that helped ease recession concerns in the world’s biggest economy.

- China, the world’s second-biggest economy and top consumer of raw materials, followed suit, and just before a week-long holiday, they announced a number of measures aimed at boosting economic growth. China’s top economic planner will hold a press briefing on 8 October, where economists and traders will look for clarification on the actions already taken while looking out for additional policy measures.

- Iran’s missile attack on Israel last week has raised expectations for a retaliatory strike that would likely serve the purpose of weakening Iran’s economy through various forms of attack, whether direct or indirect. Crude oil jumped the most last week since January 2023 for fear that an attack on Iran’s oil and gas industry may lead to tight supply and potentially widen the conflict.

In addition, a fourth development can be mentioned after US economic data in recent weeks continued to surprise to the upside, culminating on Friday when a strong US jobs report forced traders to rethink and lower the pace and depth of future US rate cuts, while driving short- and long-term yields higher. This development supports growth-dependent commodities while creating some short-term headwinds for the precious metal sector, not least gold, which, besides geopolitical support, increasingly has been showing signs of buying fatigue as physical traders balk at the prospect of buying near record highs.

One month ago, crude oil prices were struggling to hold above key support levels amid a sluggish demand outlook and the prospect of rising production, with OPEC+ focusing on slowly bringing back production that the group voluntarily had held back from the market in order to support higher and stable prices. A few weeks after briefly dipping below USD 70, Brent crude is back to challenge USD 80, with activity in the options market showing increased demand for hedging the risk of further gains amid worries about a minor or, in the worst case, major supply disruption from the Middle East.

The first part of the rally has undoubtedly been driven by wrong-footed short sellers after hedge funds, as recently as 10 September, held the first-ever recorded net short position in Brent crude futures. Since then, the weekly COT reports have pointed to increased buying activity, which undoubtedly culminated last week.

It is extremely challenging to predict the full impact of an Israeli counterstrike on Iran, aside from the likelihood of short-term price increases. Below, we outline four potential scenarios – out of many - that could emerge following such an event, with some possibly leading to downward pressure on prices:

- Under U.S. pressure, Israel may choose to delay action or focus on non-oil and gas sectors. This could result in a 10% price drop as attention shifts back to sluggish demand, particularly from China.

- A targeted strike on Iran’s oil production infrastructure could further elevate prices, reducing exports, especially to China, and potentially driving prices up by 5% to 10%.

- A strike on Iran’s refinery assets might initially boost prices but could lead to a subsequent drop in crude prices as exports rise due to Iran’s limited storage capacity. China, Iran’s main buyer of refined products, may tap into its reserves, potentially preventing significant spikes in gasoline and diesel prices.

- A major disruption of oil and gas flows through the Strait of Hormuz would be a key concern, as it could impact around 30% of global supply. While some producers could redirect flows via pipelines, many would struggle to transport their crude. This scenario carries the risk of oil prices temporarily rising to USD 100 or higher. In response, the market may look to strategic reserves and increased production from countries with spare capacity.

Recent commodity articles:

7 Oct 2024: COT: Broad buying momentum persists, led by Brent, copper and grains

2 Oct 2024: Q3 2024 Commodity Outlook: Gold and silver continue to shine bright

30 Sept 2024: COT: Fed and PBOC trigger largest weeklyl surge in commodities demand in a decade

27 Sept 2024: Commodity weekly: Industrial metals gain strength during a week of crude weakness

26 Sept 2024: Crude prices drop again as Saudi and Libya supply concerns grow

24 Sept 2024: Fed and PBOC add momentum to commodities market rebound

23 Sept 2024: COT: Dollar short reduced; Investment metals see strong demand ahead of FOMC

20 Sept 2024: Commodity weekly: Commodities boosted by bumper rate cut

20 Sept 2024 Video: Gold or silver, which metal will perform the best

17 Sept 2024: With gold reaching new heights, silver shows potential

16 Sept 2024: COT: Record short Brent and gas oil positions add upside risks to energy

11 Sept 2024: Crude slumps amid technical selling and recession fears

10 Sept 2024: US Election: will gold win in all scenarios

9 Sept 2024: COT: Crude long cut to 12-year low; Dollar short more than doubling

5 Sept 2024: Can gold overcome the 'September curse'?

4 Sept 2024: Wheat rises on European crop worries

3 Sept 2024: Chinese economic woes drag down crude oil and copper

2 Sept 2024: COT: Commodities see broad demand as the USD slumps to a net short