Crude prices drop again as Saudi and Libya supply concerns grow

Key points

- Crude oil trades lower, having failed to join the China stimulus-led rally seen among other commodities this week

- While the demand outlook shows signs of stabilising, the prospect of rising supply is now weighing on prices

- The latest weakness is driven by a report saying Saudi Arabia is ready to increase production and regain market share

Crude oil’s failed attempt to join the China stimulus-led rally seen among other commodities sectors this past week highlights a market where the focus has switched away from an improved demand outlook to the prospect of additional supply hitting the market at a time when it is not needed. Having failed earlier in the week to gain a foothold above USD 75, Brent crude is back on the defensive following a two-day slump, and for now, the outlook remains short-term challenged with a sustained break below USD 70 potentially sending prices lower towards USD 65, while a move above USD 75 is needed to trigger fresh buying from speculators, some of whom currently hold net short positions.

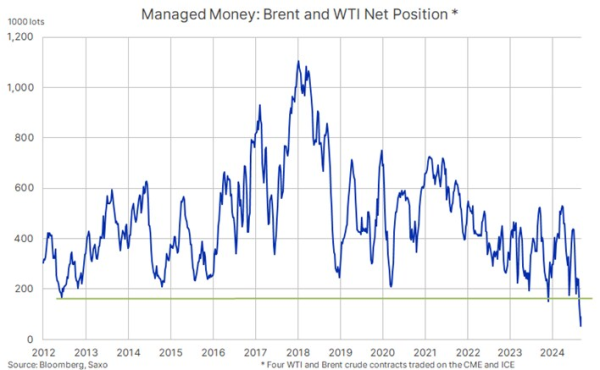

Prior to this month, Brent, the global benchmark, had spent a prolonged period trading sideways in a wide USD 70 to 90 per barrel range before recession angst and demand worries briefly sent prices into the USD 60s only to be rescued by the Federal Reserve’s first and bumper 50 basis point rate cut. China’s bold stimulus measures briefly supported prices, but the failure to move back above the key USD 75 level confirmed the current weak sentiment, which recently resulted in the first-ever recorded short position being held in Brent by hedge funds. Combined with a net long in WTI, speculators nevertheless hold the weakest belief in higher prices since at least 2012.

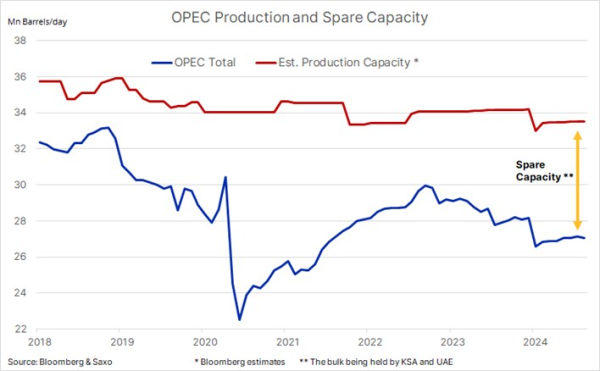

Driven by slowing demand growth and a high level of spare capacity (see chart below), especially among OPEC’s GCC members who have provided the bulk of voluntary production cuts, we believe the 70s are the new 80s for Brent, though the risk of an increased supply-driven slump into the 60s cannot be ruled out—especially if OPEC+ unity is challenged by persistent cheating from several members, such as Iran, Kazakhstan, Russia, and the UAE.

The prospect of additional supply from Libya and Saudi Arabia has been the main driver behind the latest weakness, after representatives from Libya’s rival eastern and western administrations reached a compromise on appointing new leadership for the OPEC member’s central bank, which manages billions of dollars of the nation’s oil wealth. Since the dispute began in mid-August, the oil-rich nation has seen its daily production more than halved from above 1 million barrels to below 0.5 million barrels.

Price declines accelerated after an article in the Financial Times said Saudi Arabia is ready to abandon its official oil price target of USD 100 a barrel as it prepares to increase output—a major shift in thinking from the de-facto leader of OPEC, who, since November 2020, has led other OPEC+ members in repeatedly cutting output to support stable and high prices. While stability, until recently, was successfully achieved, the higher price target has failed, not least due to a major slump in China’s oil demand growth, down from around 1.3 million barrels a day in 2023 to less than 200,000 barrels a day in 2024.

In response to falling prices, the OPEC+ group of producers last month postponed until December plans to gradually roll back voluntary production cuts of 2.2 million barrels per day. Saudi Arabia, the biggest contributor with around 1 million barrels of these cuts, has, in the past couple of years, seen its crude revenue and market share slump. The outlook for slowing demand growth, not least in China, has probably prompted them to accept a lower price tag for crude and, with that, the need to increase production. Saudi Aramco, the state-run oil behemoth, has seen its profit take a hit, even as the company has maintained its massive dividend payout that is crucial for the government to plug a rising budget deficit.

Recent commodity articles:

24 Sept 2024: Fed and PBOC add momentum to commodities market rebound

23 Sept 2024: COT: Dollar short reduced; Investment metals see strong demand ahead of FOMC

20 Sept 2024: Commodity weekly: Commodities boosted by bumper rate cut

20 Sept 2024 Video: Gold or silver, which metal will perform the best

17 Sept 2024: With gold reaching new heights, silver shows potential

16 Sept 2024: COT: Record short Brent and gas oil positions add upside risks to energy

11 Sept 2024: Crude slumps amid technical selling and recession fears

10 Sept 2024: US Election: will gold win in all scenarios

9 Sept 2024: COT: Crude long cut to 12-year low; Dollar short more than doubling

5 Sept 2024: Can gold overcome the 'September curse'?

4 Sept 2024: Wheat rises on European crop worries

3 Sept 2024: Chinese economic woes drag down crude oil and copper

2 Sept 2024: COT: Commodities see broad demand as the USD slumps to a net short

30 Aug 2024: Commodities sector eyes fourth weekly gain amid softer dollar and Fed expectations

27 Aug 2024: Month-long sugar slide pauses amid concerns of Brazil's supply

27 Aug 2024: Libya supply disruptions propel crude prices higher

26 Aug 2024: COT: Funds boost metals investment as dollar long positions halve amid weakness

23 Aug 2024: Commodities Weekly: Metal strength counterbalancing energy and grains

22 Aug 2024: Persistent supply contraints keep cocoa prices elevated

21 Aug 2024: Weak demand focus steers crude towards key support

19 Aug 2024: Resilient gold bulls drive price to fresh record above USD 2500

19 Aug 2024: COT Buyers return to crude as gold stays strong; Historic yen buying

16 Aug 2024: Commodities weekly: Gold strong as China weakness drags on other markets

9 Aug 2024: Commodities weekly: Calm returns to markets, including raw materials