Daily Comment – Dollar edges up, stocks muted as China stimulus underwhelms

- China announces more stimulus details but no word on size of package

- Attention turns to week’s other events as stocks unimpressed

- Euro and pound flat as ECB decision and UK CPI awaited

China pledges more support, stocks steady

Chinese officials unveiled more measures to shore up the country’s embattled property sector while also pledging further support for businesses and consumers in two separate announcements on Saturday and Monday. But the much-anticipated details on Beijing’s fiscal stimulus plans were short on key specifics such as the timeline and the overall size and allocation of the package, leaving investors underwhelmed yet again.

Still, the message from the finance ministry that the government is willing to increase borrowing to finance its plans as well as capitalise its banks to boost lending was very clear, and this was enough to maintain the positive sentiment in equity markets.

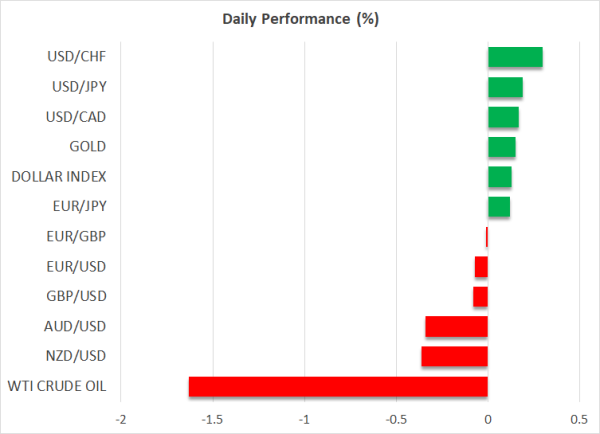

China’s major equity indices managed to close up by around 2%, though investors elsewhere were more sceptical and gains were more modest. US futures, meanwhile, were last trading little changed from Friday’s close, and the US dollar has started the week on a solid footing.

Dollar seeks to extend gains after data boost

After two strong weeks, it seems that the dollar’s recovery has more to go, although with a much quieter economic agenda this week, the rebound might lose momentum. The change in the greenback’s fortunes come on the back of the repricing of Fed rate cut expectations following hotter-than-expected data, as reinforced by last week’s inflation indicators. Both the CPI and PPI reports surprised to the upside, meaning the Fed will find it hard to justify another 50-basis-point cut at its remaining two meetings of the year.

The dollar would have probably rallied more last week had it not been for the jump in weekly jobless claims, which bolstered the case for gradual policy easing. The focus this week is on Thursday’s retail sales numbers for September. But the week will get off to a slow start as the US bond market is shut today for Columbus Day, although comments by Governor Waller might draw some attention at 19:00 GMT.

ECB meeting the week’s main highlight

For European currencies, however, the week could shape up to be quite significant. The European Central Bank is expected to cut its main lending rates by 25 bps on Thursday for the third time this year as the economic outlook in the euro area takes a turn for the worse.

The euro has pulled back from around $1.12 in September to test the $1.09 level as the PMI and inflation data since the last meeting have come in below expectations. Nevertheless, the hawks within the ECB might be wary about trimming rates too quickly and any signs of divisions on Thursday might be positive for the euro.

UK data eyed for BoE clues, oil slips

The pound has also had a tough couple of weeks after Bank of England Governor Andrew Bailey opened the door to steeper rate cuts. Yet, a 25-bps cut is not fully priced in for the BoE’s next meeting in November, so this week’s releases will be crucial for market bets.

The latest UK jobs numbers will be watched first this week, particularly the wage growth data, before investors turn to Wednesday’s CPI report for September for more clues.

In other currencies, the Australian and New Zealand dollars struggled the most against their US counterpart on Monday amid some disappointment from China’s stimulus announcements. Oil futures came under pressure too, with the lack of escalation in the Middle East conflict further dampening prices. But gold climbed higher, hoping to extend its positive streak to a third day.