Daily Comment – Risk appetite ebbs as markets fret over China stimulus, Fed rate cuts

- Risk sentiment dented as China refrains from fresh stimulus measures

- Fed officials give cautious green light to more rate cuts

- Dollar and equities turn lower after recent gains as US CPI awaited

Markets consolidate as China announcement disappoints

Optimism about China’s newfound love for bold stimulus policies faded slightly on Tuesday as a much-anticipated press briefing by the country’s National Development and Reform Commission (NDRC) ended without any significant new measures being announced. Chinese traders returned from a week-long holiday today and hopes were high that the government would unleash more big packages to support the flagging economy.

Instead, the decision to bring forward a 100 billion yuan investment plan failed to satisfy investors. Nevertheless, Chinese stocks managed to finish the day sharply higher in a catch-up move, but equites globally turned red.

Fedspeak unable to extend dollar rally

The sense of disappointment wasn’t restricted to just China, however, as investors sifted through the latest remarks by Fed officials. In a busy week for Fedspeak, Monday’s commentary, which included those from Williams, Kugler and Musalem, were balanced, supporting the case for additional rate cuts but seeing little need for further 50-bps moves.

Rate cut expectations held steady after the comments, with investors pricing in 25-bps reductions in both November and December, following the dialling back of aggressive bets after Friday’s blowout jobs report. But Wall Street closed lower and futures are flat today.

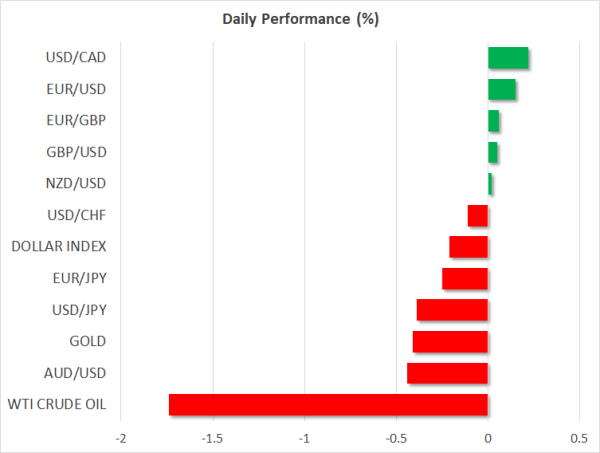

The US dollar is also on the slide today, snapping a six-day winning streak that took its gauge against a basket of currencies to a seven-week high. The focus now is on Thursday’s CPI report for September, which could further cast doubt on whether another rate cut is forthcoming in November. Ahead of that, the minutes of the Fed’s September meeting will be watched tomorrow to gain better insight into the Fed’s thinking behind the surprise decision to cut by 50 bps.

Yen recoups some losses as aussie struggles

Elsewhere, the yen sought to extend its gains for a second day as it recovers from last week’s losses when it came under pressure from Japanese Prime Minister Ishiba’s U-turn on his support for interest rate normalisation.

The Australian dollar slid the most as the absence of fresh stimulus from China weighed on the currency even as the Reserve Bank of Australia revealed it has not ruled out future rate hikes in its meeting minutes that were published today. The attention is now on the New Zealand dollar as the RBNZ is expected to slash rates by 50 bps when it meets early on Wednesday.

Gold drifts lower as oil tumbles

Gold prices remained subdued on Tuesday despite the softer greenback. The pullback in Treasury yields today is very modest and seems more of a corrective move than a sustained reversal, and this is likely holding gold bulls back for the time being. Still, with strong support in the $2,630 area, a near-term bounce back is possible, especially as tensions in the Middle East remain very elevated.

Oil futures are also correcting lower, slipping by around 2.0% as the world holds its breath while Israel decides on how to respond to last week’s missile attack by Iran. The fact that Israel has yet to carry out retaliatory strikes could be an indication that its response will be measured, and this could be negative for oil in the short term. In the meantime, Israel continues to bombard south Lebanon, with no end in sight to the conflict in the region.