Daily Comment – Strong US data keep the dollar in demand

- ECB cuts rate, keeps door wide open to a December move

- Euro suffers as US retail sales surprise on the upside

- Focus today is on Fedspeak and in particular Fed’s Bostic

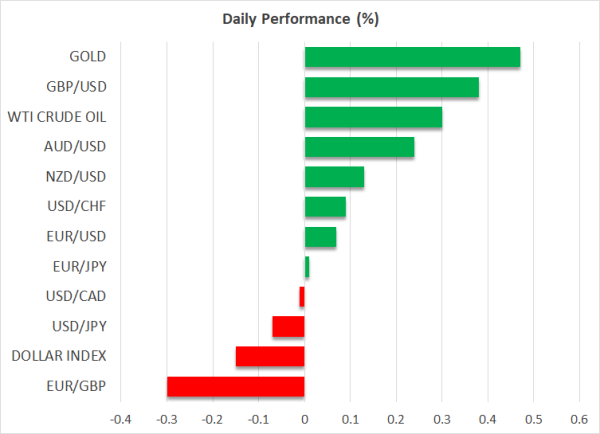

- Gold surpasses $2,700 as China announces further measures

ECB announces rate cut, prepares for a December move

The euro suffered another weak session yesterday, with the euro/dollar pair dropping below the key 200-day simple moving average and euro/pound fully erasing the recent UK CPI-induced correction. The ECB announced the overwhelmingly expected 25bps rate cut with President Lagarde maintaining her recent rhetoric.

The weak September PMI surveys played a crucial role in yesterday’s decision, which means that the October version of the PMIs published next week is potentially more important than the next inflation report. The market is fully pricing in another 25bps rate cut in December with some investment houses talking about an acceleration in the easing pace, which could prove a strong headwind for the euro.

The October version of the PMIs published next week is potentially more important than the next inflation report.

US retail sales have had a bigger market impact

The key print of yesterday’s session proved to be US retail sales. Following the strong jobs report and the above-expectations inflation prints, the September retail sales figures produced another upside surprise and confirmed the underlying strength of the US economy. This latest data release further complicates the discussion about the November 7 Fed meeting, although the market remains confident that a 25bps rate cut will be delivered.

Understandably, the Fed hawks might be less inclined to approve another cut, especially if the outcome of the US presidential election is not finalized by November 7. Fed members Kashkari, Waller and Bostic will be on the wires today with the Atlanta Fed President being the one that talked about a pause last week.

Could the Middle East conflict come to an end?

Apart from the preliminary PMI surveys, next week’s calendar is rather light on US data prints, which means that Fedspeak, the third quarter earnings and especially the pre-election rhetoric will remain in the spotlight. The current US administration is trying to boost Harris’s chances of winning on November 5 by pushing once again for a ceasefire in the Middle East.

And the latest developments on the ground could open the door to such an outcome. The assassination of the Hamas leader is celebrated in Israel with PM Netanyahu stating that "this action is the beginning of the end for the war in Gaza". Gold has not taken notice of this comment yet, as it achieved a new all-time high by climbing above the $2,700 level, despite the dollar recording another strong session.

China announces further support measures

Following numerous press conferences from Chinese officials, it was the PBoC Governor’s turn to take the stand and present the next likely steps to boost market liquidity and help the Chinese economy to transform into a consumption powerhouse. While the market remains skeptical of the recent announcements, the mood seems to be improving somewhat following today’s positive set of data prints and predominantly the strong retail sales figures.

Following numerous press conferences from Chinese officials, it was the PBoC Governor’s turn to take the stand

Pound rallies on stronger retail sales

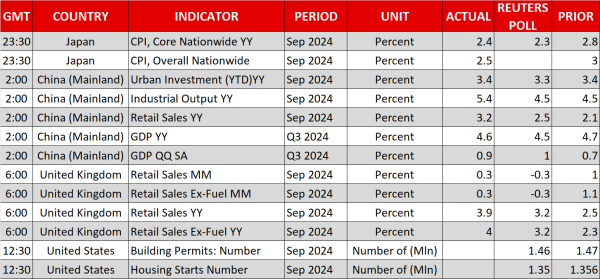

September was apparently a good month for consumer spending as the UK retail sales report, published earlier today, also managed to produce an upside surprise. The pound is on the rise again against both the dollar and euro, quickly erasing the impact of Wednesday’s very weak inflation report. The market is still confident that a November 25bps rate cut will be announced, but stronger figures like today’s retail sales could potentially shut the door to a more aggressive easing pace.