Daily Comment – US dollar could benefit from an unexciting ECB meeting

- ECB meets but unlikely to reverse euro’s recent trend

- Both the dollar and US stocks are in a good mood

- Netflix reports today after TSMC's massive profit jump

- Gold and bitcoin in demand, oil craves a bullish catalyst

Euro's suffering continues as ECB meets

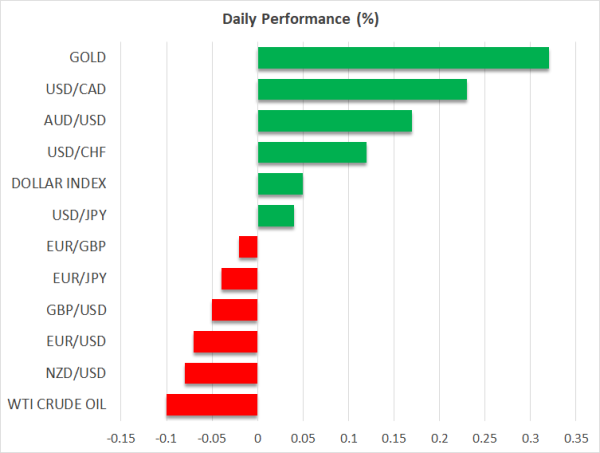

The euro remains on the back foot as it continues to underperform the dollar. The pair has dropped to the lowest level since August 2 with October shaping up to be the weakest month for euro/dollar since May 2023. This dollar outperformance could be partly explained by the lower expectations for a sizeable November Fed rate cut, but realistically the euro area economy is expanding at a snail’s pace compared to the USA's impressive growth rate.

October is shaping up to be the weakest month for euro/dollar since May 2023

Amidst these developments, the ECB will announce its rate decision at 12:15 GMT, with the usual press conference coming thirty minutes later. The market is pretty confident that another 25bps rate cut will be decided as it is currently assigning a 98% probability to such a move.

There are a plethora of reasons why the ECB could surprise by keeping rates unchanged. The meeting is not being held in Frankfurt, there are no updated staff projections and today’s gathering comes only five weeks after the September one. Even the weak September inflation print was not really a surprise as President Lagarde had already announced that a downside surprise was expected. Should the ECB decide to pause, the euro stands to benefit by potentially climbing above the $1.0930 level, provided of course that Lagarde does not pre-announce a sizeable December rate cut.

However, as both the Fed and the ECB tend to avoid disappointing the markets, the ECB will most likely confirm expectations for the 25bps cut. In this case, the focus will quickly turn to the press conference where Lagarde will most likely keep the door open to more accommodation but avoid precommitting. In this case, the euro should remain under pressure, although some profit taking could be in store following the aggressive dollar rally.

As both the Fed and the ECB tend to avoid disappointing the markets, the ECB will most likely confirm expectations for the 25bps cut.

US stocks smile again

US equity indices managed to turn the tide by recording gains yesterday, following a disastrous session on Tuesday on the back of concerns about AI and chip demand. The third quarter earnings releases continue today with Netflix scheduled to report before the US markets open. Following TSMC’s 54% profit rise earlier today, more positive earnings releases will most likely help technology stocks cover some of the lost ground and allow the Nasdaq 100 index to outperform the remaining key US stock indices.

Today’s retail sales data could really ignite the discussion about a Fed pause on November 7

But the markets will also pay attention to today’s data prints. Following the recent strong jobs report and the upside inflation surprise, today’s retail sales data could really ignite the discussion about a Fed pause on November 7. The weekly jobless claims are also published today but the recent hurricane Milton could materially impact these figures. Finally, Chicago Fed President Goolsbee will be on the wires today, and he will most likely confirm his dovish stance.

Gold and bitcoin are in a good mood, oil tries to find its footing

Gold continues to ignore the strong dollar rally, as it is edging higher again, retesting the September 26 high of $2,685. This move comes on the back of the continued negative newsflow from the Middle East, where Israel is apparently ready for its retaliatory strike against Iran and its proxies, and the market treating the latest stimulus announcements from the Chinese administration with extra skepticism.

In the meantime, the crypto world is enjoying strong gains this week with bitcoin rallying up to $68,300, before settling a tad lower. On the flip side, oil is hovering just above the $70 level, as the market seems to believe that Israel will target military bases and avoid oil installations, which is an odd reaction considering the fluidity of the situation in the Middle East.