Dow 30: weekly technical overview buoyed by fundamental forces

Dovish FOMC stirs hopes for rate cut amid weaker data

Plenty of data came out of the US last Friday, with the focus primarily on its labour market, where:

- Non-Farm Payrolls for April saw growth of 175K, finally experiencing a clear miss from mostly 200K+ forecasts (with net downward revisions)

- The unemployment rate rose to 3.9%, with the U6 also a notch higher at 7.4%

- Wage growth month-on-month (m/m) was slightly below forecasts at 0.2%, taking the year-on-year (y/y) figure below 4%

- The labour force participation rate held at 62.7%, but the employment-population ratio was a notch lower at 60.2%

- The employment component of the latest ISM services release dropped from 48.5 to 45.9 (for manufacturing last Wednesday also beneath 50), with the overall print falling into contraction for the first time in over a year (new orders dropped to 52.2, prices paid jumped to 59.2).

Key stock indices finished the week with gains, supported by a dovish FOMC (Federal Open Market Committee) hold and clearly weaker data, with Treasury yields finally offering a notable red weekly finish (the 10-year ending near 4.5%), lower in real terms, and market pricing (CME's FedWatch) more comfortable on a September rate cut compared to the start of last week and improved odds for two by the end of this year.

Week Ahead: Treasury auctions, FOMC members speaking, and UoM’s preliminary figures

The week ahead is relatively lighter out of the US compared to last week. The Fed’s Senior Loan Officer Survey is releasing today for those wanting insight into loan demand from both households and businesses over the first quarter of this year. Consumer credit is tomorrow for March, where the figures, as of late, have been beneath pre-pandemic averages.

But it isn’t just consumer borrowing market participants have been noting, as the notable uptick in government spending and issuance to cover rising deficits have meant Treasury auctions have been taking some attention and more so when demand has struggled to keep up with the growing supply. Lastly, there's UoM’s (University of Michigan) preliminary consumer sentiment and inflation expectations on Friday to see if the former struggles, especially when there's an increase in the latter.

Dow technical analysis, overview, strategies, and levels

Another week finishing in the green is a plus for its weekly technical overview that has been struggling as 'bull average' with most of its key technical indicators neutral but the price still above all its main long-term weekly moving averages. As for the shorter-term daily timeframe, it's 'cautious consolidation' but enjoying a more positive technical bias due to breaking out of narrower ranges and shy of crossing and closing above the last of its main daily moving averages.

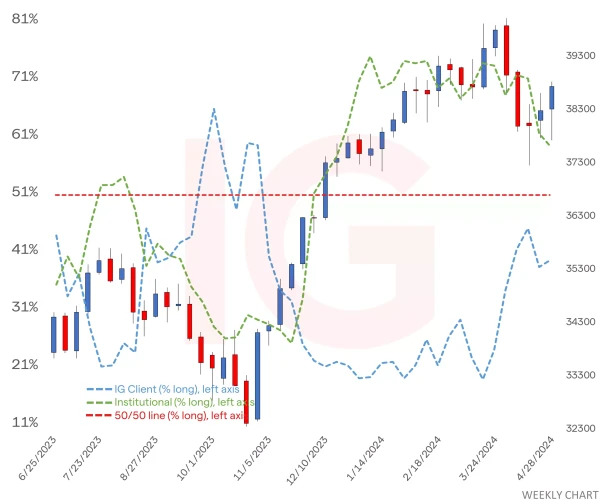

IG client* and CoT** sentiment for the dow

CoT speculators have been pulling back their majority long bias somewhat (longs -1,383 lots, shorts +271), despite consecutive price gains (though positioning as of last Tuesday means it doesn't factor in the fundamental updates from last Wednesday and Friday). IG clients have been increasing their majority sell bias, moving it into heavy short territory. They were close to the middle last Tuesday before the price gains.

Dow chart with retail and institutional sentiment

- *The percentage of IG client accounts with positions in this market that are currently long or short. Calculated to the nearest 1%, as of the start of this week for the outer circle. Inner circle is from the start of last week.

- **CoT sentiment taken from the CFTC’s Commitment of Traders report, outer circle is latest report released on Friday with the positions as of last Tuesday, inner circle from the report prior.