Euro has been struggling lately as US dollar gained momentum

Next round of inflation data is due on Wednesday at 10:00 GMT

Overall, outlook for the euro seems negative at this stage

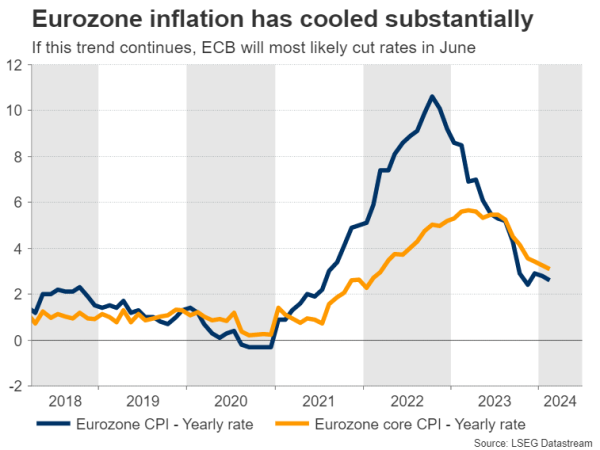

Euro gets knocked downIt’s been a difficult year for the euro so far. The single currency lost more than 2% against the US dollar in the first quarter, dragged down by a long spell of economic stagnation in the euro area, alongside mounting signs that the US economy is in much better shape. Germany continues to hold back growth in the Eurozone. The bloc’s largest economy contracted last year, plagued by a slowdown in global trade that has suppressed demand for exports, crippling the nation’s manufacturing sector. Higher energy bills after the invasion of Ukraine and the phasing out of Russian gas have exacerbated the problem. Unfortunately, the situation is unlikely to improve anytime soon, as the German government has been forced to slash public spending and investment in order to conform to constitutional debt rules that prohibit deficit spending. Therefore, Germany desperately needs an injection of stimulus, but has been given a dose of austerity instead. This could dampen growth further, leading to a situation where the European Central Bank has to cut interest rates faster and deeper than what the markets currently anticipate. Inflation in focus Next week, the spotlight will fall on the latest batch of inflation data, which will be crucial in shaping expectations around the ECB’s path and therefore for the euro itself. The ball will get rolling on Tuesday with Germany’s stats, ahead of the Eurozone-wide prints on Wednesday. Economist forecasts suggest inflation in the Eurozone continued to cool in March, with the CPI rate expected to drop to 2.5% in yearly terms from 2.6% previously, even despite the recent spike in oil prices. Business surveys pointed in the same direction, noting that Eurozone companies raised their selling prices at a slower pace in March. Considering that oil prices rose during the month, this implies that the decline in the core CPI rate may be even greater, as this figure excludes the effects of energy and food prices. A persistent slowdown in inflation would be welcome news for ECB officials, but perhaps bad news for the euro, as it would make investors more confident that rate cuts are imminent. Looking at the charts, euro/dollar has been sliding lately and further declines could bring the 1.0700 region into play. On the flipside, the most important zone to watch on the upside is the March peak of 1.0980. If the bulls break the downtrend line and then overcome this area, the technical picture would brighten. Euro outlook is grimAll told, the euro does not seem attractive at this stage. Growth fundamentals have deteriorated and recession risks could remain in play, especially with Germany ‘tightening its belt’. One reason the euro has been so resilient over the past year has been the collapse in natural gas prices, which has boosted the currency through the trade channel. The cheerful tone in stock markets also helped, by pinning down the safe-haven US dollar. Therefore, the euro has been kept afloat not by its economic performance, but mostly from developments in other financial markets. As such, any change in these trends could remove a big pillar of support for the single currency, forcing it to realign with its gloomy fundamentals. In a nutshell, the euro needs low gas prices and rising stock markets to remain above water. Otherwise, traders might start focusing on the dark growth outlook.

This could dampen growth further, leading to a situation where the European Central Bank has to cut interest rates faster and deeper than what the markets currently anticipate. Inflation in focus Next week, the spotlight will fall on the latest batch of inflation data, which will be crucial in shaping expectations around the ECB’s path and therefore for the euro itself. The ball will get rolling on Tuesday with Germany’s stats, ahead of the Eurozone-wide prints on Wednesday. Economist forecasts suggest inflation in the Eurozone continued to cool in March, with the CPI rate expected to drop to 2.5% in yearly terms from 2.6% previously, even despite the recent spike in oil prices. Business surveys pointed in the same direction, noting that Eurozone companies raised their selling prices at a slower pace in March. Considering that oil prices rose during the month, this implies that the decline in the core CPI rate may be even greater, as this figure excludes the effects of energy and food prices. A persistent slowdown in inflation would be welcome news for ECB officials, but perhaps bad news for the euro, as it would make investors more confident that rate cuts are imminent. Looking at the charts, euro/dollar has been sliding lately and further declines could bring the 1.0700 region into play.

This could dampen growth further, leading to a situation where the European Central Bank has to cut interest rates faster and deeper than what the markets currently anticipate. Inflation in focus Next week, the spotlight will fall on the latest batch of inflation data, which will be crucial in shaping expectations around the ECB’s path and therefore for the euro itself. The ball will get rolling on Tuesday with Germany’s stats, ahead of the Eurozone-wide prints on Wednesday. Economist forecasts suggest inflation in the Eurozone continued to cool in March, with the CPI rate expected to drop to 2.5% in yearly terms from 2.6% previously, even despite the recent spike in oil prices. Business surveys pointed in the same direction, noting that Eurozone companies raised their selling prices at a slower pace in March. Considering that oil prices rose during the month, this implies that the decline in the core CPI rate may be even greater, as this figure excludes the effects of energy and food prices. A persistent slowdown in inflation would be welcome news for ECB officials, but perhaps bad news for the euro, as it would make investors more confident that rate cuts are imminent. Looking at the charts, euro/dollar has been sliding lately and further declines could bring the 1.0700 region into play.  On the flipside, the most important zone to watch on the upside is the March peak of 1.0980. If the bulls break the downtrend line and then overcome this area, the technical picture would brighten. Euro outlook is grimAll told, the euro does not seem attractive at this stage. Growth fundamentals have deteriorated and recession risks could remain in play, especially with Germany ‘tightening its belt’. One reason the euro has been so resilient over the past year has been the collapse in natural gas prices, which has boosted the currency through the trade channel. The cheerful tone in stock markets also helped, by pinning down the safe-haven US dollar. Therefore, the euro has been kept afloat not by its economic performance, but mostly from developments in other financial markets. As such, any change in these trends could remove a big pillar of support for the single currency, forcing it to realign with its gloomy fundamentals. In a nutshell, the euro needs low gas prices and rising stock markets to remain above water. Otherwise, traders might start focusing on the dark growth outlook.

On the flipside, the most important zone to watch on the upside is the March peak of 1.0980. If the bulls break the downtrend line and then overcome this area, the technical picture would brighten. Euro outlook is grimAll told, the euro does not seem attractive at this stage. Growth fundamentals have deteriorated and recession risks could remain in play, especially with Germany ‘tightening its belt’. One reason the euro has been so resilient over the past year has been the collapse in natural gas prices, which has boosted the currency through the trade channel. The cheerful tone in stock markets also helped, by pinning down the safe-haven US dollar. Therefore, the euro has been kept afloat not by its economic performance, but mostly from developments in other financial markets. As such, any change in these trends could remove a big pillar of support for the single currency, forcing it to realign with its gloomy fundamentals. In a nutshell, the euro needs low gas prices and rising stock markets to remain above water. Otherwise, traders might start focusing on the dark growth outlook.