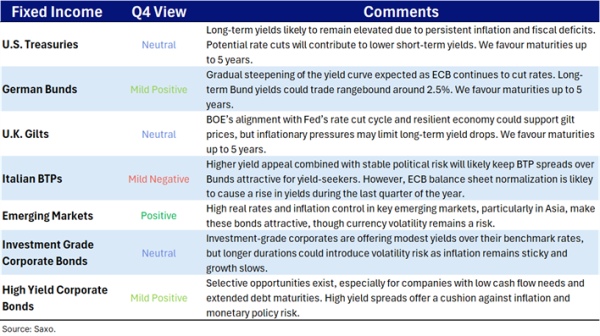

Fixed Income Outlook: Bonds Hit Reset. A New Equilibrium Emerges

Key points

- Interest Rate Cuts and Inflation: Central banks in the US and Europe are gradually cutting rates, but persistent inflation and fiscal deficits are likely to keep long-term yields elevated.

- Economic Outlook: US growth is decelerating, and inflation remains above target, while Europe’s recovery, though modest, is bolstered by low unemployment and rising wages. This environment is likely to keep policymakers cautious, increasing the risk of rate cut disappointments as central banks may hold back on aggressive easing.

- Investment Strategy: Investors should focus on short-to-intermediate bonds, prioritize strong credits, and consider emerging market bonds for attractive yields.

Overview: Navigating Rate Cuts and Inflationary Pressures

As we enter the final quarter of 2024, the fixed-income landscape presents a mix of opportunities and risks. Central banks, particularly in the US and Europe, are expected to continue gradual rate cuts, with a more normalized interest rate environment likely by late 2025. However, persistent inflation and fiscal deficits will likely keep long-term yields elevated, complicating the bond market. Investors should continue to focus on building a defensive buffer, prioritizing sound credits, and remaining agile in response to potential shifts in monetary policy and fiscal conditions.

Economic Outlook: Slower Growth and Persistent Inflation

The US economy remains resilient, with annualized growth of 3.1% as of June, driven by solid consumer spending. However, signs of a slowdown are emerging, as the labor market cools and job growth moderates. GDP growth is projected to slow to 2.4% in 2024 and further to 1.7% in 2025. While inflation has eased from its 2022 peak, it remains above desired levels, which will likely keep the Federal Reserve cautious about its rate-cutting trajectory.

In Europe, the economic recovery has been slower than expected, but low unemployment and rising real wages continue to support growth. The ECB is likely to maintain its gradual rate-cutting approach, aiming to bring the deposit rate to 2.5% by September 2025.

Interest Rates: A New Equilibrium Emerges

Interest rates across developed markets are stabilizing at a higher equilibrium, driven by central banks' cautious efforts to control inflation. In the U.S., inflation has moderated but remains elevated. The Federal Reserve has already cut 50 basis points, and forecasted two more 25 basis point cuts this year at its September meeting, depending on incoming data. Rate reductions could continue into 2025, potentially bringing the Fed Funds rate down to 3.5%. However, core inflation remains sticky and, barring recession, the Fed is likely to keep a restrictive stance to avoid reigniting inflationary pressures. That’s why the Fed’s longer run forecast of the long-term neutral rate has inched higher to the current 2.9% level, the highest since September 2018. This would likely mean elevated long-term U.S. Treasury yields in the medium term.

In Europe, economic growth has lagged expectations, but low unemployment and rising real wages continue to support modest GDP expansion. The ECB is expected to gradually reduce rates by 25 basis points per quarter, possibly lowering the deposit rate to 2% by late 2025. Yield curves in Europe are also likely to steepen, although long-term yields may remain elevated, influenced by trends in U.S. Treasuries.

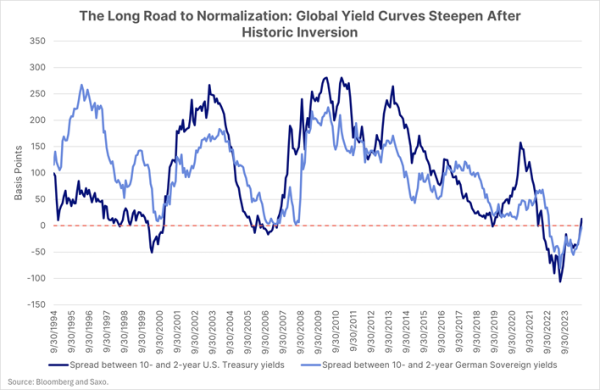

Yield Curve Dynamics: Gradual Normalization Amid Structural Pressures

In the U.S., the yield curve is gradually normalizing as the Fed proceeds with rate cuts. However, long-term yields may face upward pressure due to ongoing concerns about deficit spending and the potential for economic reacceleration in 2025. Looking at the September FOMC macroeconomic forecast, which anticipates 2% real GDP growth over the next three years and inflation returning to 2%, the fair value of 10-year U.S. Treasury yields should be around 4%. Long-term yields are likely to remain rangebound until a clearer direction emerges from the U.S. election or a more rapid deterioration in economic conditions.

European yield curves are expected to follow a similar trajectory, with longer-term yields remaining elevated. In particular, the German 10-year Bund could rise to find a new trading range around 2.5%. The spread between Italian BTPs and German Bunds may widen slightly as the ECB normalizes its balance sheet, although we expected it to remain well below 200bps throughout the last quarter of the year, as BTPs attract investors seeking higher yields.

Investment Strategy: Managing Inflation, Volatility, and Monetary Policy Risks.

As we move into Q4 2024, bond investors should focus on building a buffer against inflation and potential surprises in monetary policy, exactly as in 2022 and 2023. Although markets anticipate an aggressive rate-cutting cycle, central banks may deviate from these expectations. Positioning in the short-to-intermediate segments of the yield curve will help investors capitalize on falling rates while reducing exposure to long-end volatility.

Credit selection will be critical, particularly in a volatile environment. Companies, particularly in the junk bond space, that have no immediate cash flow needs and have successfully extended their debt maturities are well-positioned to offer attractive yields while being resilient in the face of an economic slowdown. There are also opportunities in the investment-grade space, although these bonds generally carry longer durations and offer only a modest yield premium over their benchmarks.

The current environment is particularly favorable for emerging market bonds, especially in countries with high real interest rates and strong incentives to remain vigilant about inflation. These conditions give emerging market governments flexibility to cut rates, potentially enhancing bond valuations. However, by adopting a cautious approach and avoiding aggressive cuts, these countries can preserve currency stability against the dollar and euro, reducing depreciation risk.

In Latin America, central banks have already implemented significant rate cuts, limiting some investment opportunities. However, Mexico stands out, where interest rates remain elevated at above 10% as of end-Q3, despite inflation being near 5%. This gives Banxico room to cautiously lower rates while maintaining a buffer against inflation.

In Asia, the outlook is more promising. Central banks have taken a more cautious stance, with countries like Indonesia recently hiking rates in April and holding them steady since. Both Indonesia and Malaysia present attractive cases, as headline and core inflation have dropped to around 2%, while interest rates remain high, offering room for measured rate cuts in the future.