FX Outlook: USD in limbo amid political and policy jitters

Key points

- US election uncertainty: The US presidential election introduces significant risks for currency markets through several channels including fiscal policy, trade relations, foreign diplomacy as well as its impact on Fed and global interest rate policy.

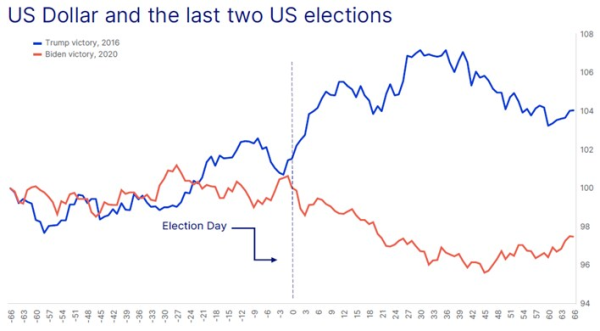

- USD in flux: A Trump victory could boost the USD through pro-growth policies that emphasize US exceptionalism and increased safe-haven demand driven by higher tariffs and geopolitical risks. However, this could also amplify structural risks to the USD. On the other hand, a Harris presidency may make the USD more dependent on Fed policy and global dynamics. A divided US Congress under Harris, however, could induce volatility, which would likely support the USD and other safe-haven currencies.

- Fed policy & JPY reversal: With the Fed hinting (and eventually starting) its rate-cutting cycle and the Bank of Japan keeping the door open for further hikes, there has been a notable shift in JPY short positioning during Q3. Scope for further unwinding in carry bets remains, which could bring still more JPY strength especially if recession concerns escalate.

Trump’s tariff threats and pro-growth policies could push USD higher

A Trump victory is expected to usher in higher fiscal spending and pro-growth policies, alongside risks of escalating trade and geopolitical tensions. While these factors are likely to provide cyclical support to the US dollar (USD), the structural outlook remains more complex.On the fiscal front, Trump’s pro-growth policies, including higher fiscal spending and tax cuts, are likely to bolster the USD by reinforcing the narrative of US economic exceptionalism. Additionally, this could ease the pressure for aggressive Fed rate cuts as recession risks decline and inflation concerns come back in focus.

Trump’s renewed focus on tariffs and protectionism would also likely lift the USD in the short term, especially against the Chinese yuan (CNH) and EM FX. Additionally, key commodity-exporting currencies such as the Australian dollar (AUD) and New Zealand dollar (NZD) could face headwinds under stricter trade policies, while the Canadian dollar (CAD) may prove more resilient due to lower exposure to tariff threats.

Geopolitically, a less supportive stance on Ukraine could heighten risk aversion, driving demand for safe-haven assets like the USD, yen, and gold. Meanwhile, European currencies may come under pressure in case of rising risks of tariffs and worsening geopolitics. The Mexican peso (MXN) is also exposed to risks of universal tariffs given its substantial exports to the US, as well as to threats of tighter immigration policies.

While the near-term outlook for the US dollar appears to be positive in case of a Trump presidency, the long-term structural outlook is potentially more bearish. Rising US debt levels and the risk of threats to the Fed’s independence could weigh on the dollar over time. Moreover, Trump’s aggressive tariff policies and strained foreign relations may accelerate global efforts to reduce reliance on the greenback as the reserve currency, amplifying risks of structural weakness.

Harris’s status quo will leave the Fed in the driving seat

A Harris presidency would likely emphasize fiscal restraint, with tax hikes playing a key role. This shift could prompt a more accommodative monetary policy from the Federal Reserve, increasing the likelihood of deeper interest rate cuts. The combination of fiscal tightening and monetary easing could be a near-term headwind for the USD. However, the probability of Harris securing a clean sweep remains low. A divided Congress could lead to policy gridlock, hindering significant fiscal initiatives and increasing market volatility. This environment might boost demand for safe-haven assets, such as the USD, Japanese yen (JPY), and Swiss franc (CHF), especially if current stimulus measures face uncertainty in renewals and concerns about a 2025 recession grow.

Harris’ victory might also avoid a drastic worsening of trade relations, which could initially boost the Chinese yuan (CNH) and other emerging market currencies, in turn weakening the USD amid a risk-on environment. However, China’s economic challenges may limit CNH gains. Similarly, commodity-exporting nations such as Australia and New Zealand could see their currencies rally as risks of worsening global trade relations are priced out. However, medium-term FX performance will largely depend on the broader economic context, whether the global economy achieves a soft landing or slips into a deeper recession.

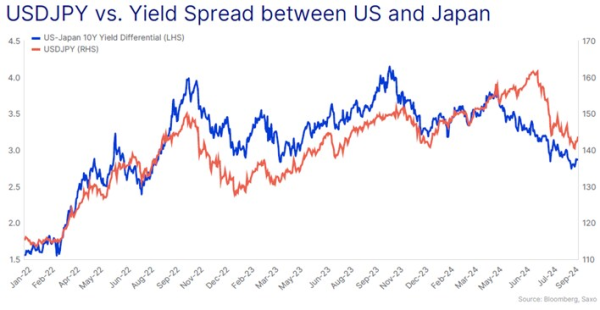

Fed policy and risks of Yen carry trade reversal

With the Federal Reserve having begun its rate-cutting cycle, the USD is facing increased downside pressure. While the ‘Dollar Smile’ theory says that a soft-landing can mean a softer USD, it also needs other major economies to be relatively stronger to attract inflows. However, the German and Canadian economies continue to face hard-landing risks and China’s growth engines could sputter further if global growth slows. This means Q4 could be bumpy for USD as the Fed cuts rates further, but a sustained sell-off may still be unlikely. Currency crosses like EURGBP (downside) or AUDCAD (upside) could remain interesting to watch on economic and policy divergences.

The Bank of Japan has left the door open for future rate hikes, narrowing the US-Japan yield differential and driving a reversal in the dollar-yen carry trade, with the pair already pulling back significantly from summer highs. As we approach the end of 2024, further unwinding of carry trade positions could support more yen strength. However, the pace may slow as the Fed could struggle to meet the market’s dovish expectations if a recession doesn’t materialize quickly. Meanwhile, the BOJ’s cautious stance, with fading yen weakness reducing price pressures, may also moderate yen gains. The case for yen strength remains, bolstered by its safe-haven appeal and the shrinking yield gap with the US, but both the Fed and BOJ are likely to move gradually, keeping yen gains more modest.