Global Market Quick Take: Asia – April 1, 2024

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

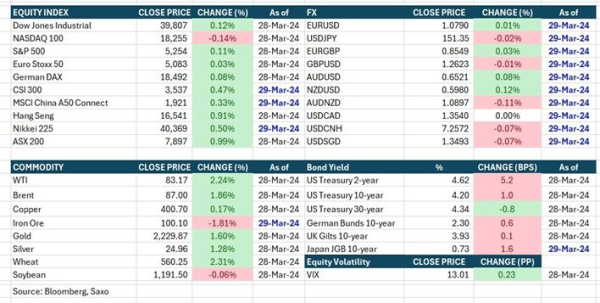

Equities: US index futures advanced on Monday Asian morning, with the S&P 500 eMini futures and Nasdaq 100 futures adding around 0.4% and 0.6%, respectively, from their closing levels last Thursday. Before the holiday, the US GDP was revised up, and consumer sentiment came in strong on Thursday. Additionally, the personal spending print released on Friday was strong, but the core PCE inflation was slower than anticipated. These data continue to point to a Goldilocks US economy, providing comfort to equity investors.

In Japan, the Nikkei 225 plunged 1.5% after the Bank of Japan’s Tankan report showing softer manufacturing activities. In mainland China, the CSI300 surged around 1.5% in early trading on Monday, adding to its 0.5% gains last Friday. Sentiments were propelled by speculation that the People’s Bank of China will be buying Central Government Bonds (CGBs), following the latest publication of remarks from President Xi, including his call for more monetary tools, which include buying and selling government bonds by the country’s central bank.

Additionally, China’s official NBS manufacturing PMI, released on Sunday, and Caixin China manufacturing PMI, released this morning, both improved more than expected. The NBS manufacturing PMI returned to the expansion territory. The Hong Kong market remains closed on Monday for a holiday.

Results released from some of China’s largest banks last Thursday showed notably weak net interest margins (NIM) as a common observation across these banks. Bank of China's revenue and earnings missed on NIM, Construction Bank experienced small misses on NIM and fees, Agricultural Bank of China slightly beat revenue and earnings in line with stronger gross loan growth, but partly offset by weakness in net interest margins (NIM). Postal Savings Bank of China had slight revenue beat, but earnings missed on fees and higher provision charges.

FX: The dollar remains steady as the Dollar Index hovers around 104.50, with EURUSD, USDJPY, and AUDUSD trading within narrow ranges, nearing 1.0790, 151.25, and 0.6525 respectively. A softer-than-expected US core PCE and dovish-leaning remarks from Powell on Friday tend to weigh on the dollar, while market reactions were muted, with traders in major markets away for holidays.

Commodities: Gold surged to $2,256 during Monday's Asian trading hours, reaching a new high amid cooler-than-expected US core PCE data.

Fixed income: This morning in the Tokyo market, reactions to the US PCE inflation data from Friday were muted, with the 10-year Treasury yield at 4.19%, 1bp below last Thursday’s New York close before the holiday-shortened week.

Macro:

- In February, US headline PCE growth slowed to 0.3% M/M, falling below the consensus of 0.4%. Notably, the core CPE inflation, the Fed's preferred gauge, came in softer than expected at 0.261% M/M, below the median forecast of 0.3% in the Bloomberg survey. Additionally, January's data was revised up to 0.452% from 0.475%, still below some economists' expectations. The downside surprises were primarily driven by softer prints in super-core service prices. On a year-on-year basis, the headline PCE increased by 2.5%, matching consensus expectations, while the core PCE rose 2.8%, slightly below the consensus of 2.8% and revised from 2.9%.

- Consumer spending in the US showed resilience, increasing by 0.8% M/M in February, surpassing the anticipated 0.5% and exceeding the previous month's 0.2%.

- Federal Reserve Chair Jerome Powell's remarks indicated a dovish-leaning stance as he stated that the February PCE inflation prints were more aligned with the Fed's targets, downplaying the hotter January data.

- The US economy's strength was reaffirmed as the Q4 GDP was revised up to 3.4% from the previously reported 3.2%.

- In Japan, the larger manufacturing enterprises index in the Bank of Japan's Tankan business confidence survey came in at 11 in Q1, slightly below the prior quarter’s 12 but above the projected 10. The outlook improved to 10 in Q1 from last quarter’s 8.

- The Tokyo core CPI (all items less fresh food) grew as expected at 2.4 Y/Y in March, but slightly slower than the 2.5% in February. The core-core CPI (all items less fresh food and energy) slowed to 2.9% Y/Y, in line with expectations and below the prior month’s 3.1%.

- China's official NBS manufacturing PMI rose to 50.8, signaling expansion and surpassing the Bloomberg surveyed consensus of 50.1 and the prior month’s 49.1. The rebound was broad-based, particularly led by strong surges in the production sub-index to 52.2 from 49.8 and the new orders sub-index to 53.0 from 49.0. The new export orders sub-index also rebounded to 51.3 from 46.3. The non-manufacturing PMI also came in stronger at 53.0, versus the projected 51.5 and the prior month’s 51.4. Meanwhile, the private Caixin China manufacturing PMI ticked up to 51.1, better than the anticipated 51.0 and the prior month’s 50.9.

Macro events: US S&P Manufacturing PMI, US ISM Manufacturing Index, US Construction Spending

Earnings: Tianshui Huatian Technology, Universal Scientific Industrial

In the news:

- Chinese Stocks Gain as Upbeat PMI Data Reinforce Recovery Hopes (Bloomberg)

- Japan's March factory activity shrinks at slower pace, PMI shows (Reuters)

- Xiaomi's EV buyers face up to seven-month wait for car, app shows (Reuters)

- Singapore Home Prices Rise for Third Quarter, Defying Slowdown (Bloomberg)

- South Korea March exports up for sixth month on chip sales (Reuters)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration