Global Market Quick Take: Asia – April 15, 2024

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

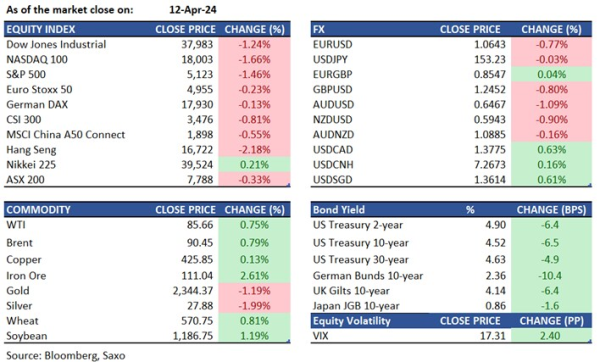

Equities: On Friday in the U.S., the Nasdaq 100 plunged by 1.7%, and the S&P 500 dropped by 1.5% in a broad-based decline, with all 11 sectors in the S&P 500 index falling. Escalation between Iran and Israel and the implication of resulting higher energy prices on inflation worried investors. Share prices of US banks did poorly on Friday despite JPMorgan, Citigroup, and Wells Fargo reporting Q1 earnings beating expectations. JPMorgan plummeted 6.4% after reporting a fall in net interest income and customer deposits. Citigroup and Wells Fargo also reported lower net interest income for Q1. In Asia, the Hang Seng sank 2.2%, with Xiaomi notably bucking the decline and rising 2.6% on an analyst raising the price target to HK$20.

This morning, after Iran said they had no intention of further attack on Israel and the White House said the U.S. would not take part in any Israeli retaliatory attack on Iran, U.S. index futures modestly rebounded in the early Asian hours. As the risk of escalation remains, Saxo’s Head of Equity Strategy suggests that equities will likely sell off short-term with high beta and cyclical sectors leading the adjustment lower such as technology, industrials, and financials. Energy, health care, and consumer staples should be bid relatively. Defence stocks (see Saxo’s defence theme basket) will continue to be extremely bid, especially European names and those that are market leaders in air defence systems such as Elbit (collaborator on Israel’s Iron Dome system), Kongsberg (the NASAMS surface-to-air missile system), Raytheon (the Global Patriot Solution), Palantir (AI surveillance and imaging recognition capabilities), and L3Harris Technologies.

FX: Dollar strength returned to the fore on Friday as Iran fears gripped markets while inflation concerns also continued to linger with higher than expected inflation expectations from the UoM survey and Fedspeak hinting at a patient approach to rate cuts. The DXY index rose to 106 and could remain a key safe-haven as a likely response from Israel keeps the market nervous. While FX markets showed a lack of a safety bid amid heightened geopolitical tensions over the weekend, all eyes remain on whether there will be any response from Israel and markets will likely be volatile in the day ahead to any geopolitical headlines. Any threats of an escalation will bring a safety bid for USD and gold, and to CHF and JPY to some extent. Likely gains in oil prices could also benefit NOK and CAD, while energy shock risks will be a headwind for EUR and emerging Asia currencies.

The SEK underperformed on Friday with Sweden’s March CPI throwing a downside surprise and opening the door to a May rate cut. EURSEK rose to 11.60 while EURUSD plunged below 1.0695 support to fresh YTD lows of 1.0623 as the room for Fed-ECB divergence has opened. ECB speak was also relatively dovish compared to Fed speak as noted below. AUDUSD tested support at 0.6450 but bounced higher while NZDUSD returned to 0.5950. USDJPY still stuck at 153+ levels amid intervention threat.

Commodities: Commodity markets will be on edge with signs of worsening geopolitics and delay of Fed rate cut expectations after the inflation shock of last week. Brent crude touched $91/barrel in early Asia open before turning slightly lower. Crude prices already included a risk premium and the extent to which it will widen further depends almost exclusively on developments near Iran around the Strait of Hormuz, and for a first, it will be fear driving oil prices higher, rather than any actual supply disruptions. Gold, meanwhile, has a major risk premium priced in already, having recently rallied strongly despite dollar and bond yield strength. With that in mind, the metal may struggle to regain last week’s strong momentum before going through a long overdue consolidation. Watch support at USD 2320 followed by USD 2290.

Fixed income: On Friday, U.S. Treasuries rallied in prices, with the 2-year yield falling 6 bps to 1.90% and the 10-year yield declining by 7 bps to 2.52%, amid escalating tensions in the Middle East and weakness in equities. While geopolitical events could keep energy prices higher and potentially inflation higher for longer, we expect US and European government bonds to be bid as they are the deepest market for derisking portfolios.

Macro:

- US preliminary UoM sentiment for April fell to 77.9 from 79.4, falling short of the expected 79.0. Current conditions and the forward-looking expectations indices fell to 79.3 (prev. 82.5, exp. 82.2) and 77.0 (prev. 77.4, exp. 77.6), respectively. Inflation expectations rose, with both 1yr and 5-10yr coming in ahead at their highest since November 2023, printing 3.1% (prev. 2.9%) and 3.0% (prev. 2.8%), respectively.

- There was a lot of Fedspeak, all hinting at patience on rate cuts. Bostic repeated his message of one rate cut this year, while Daly said that the Fed will maintain policy stance as long as necessary. Both are voters this year. Others like Goolsbee, Collins and Schmid, who vote in 2025, all talked about inflation concerns and advocated patience on rate cuts.

- ECB speak came from Kazaks and Stournaras, where the former towed the seemingly given ECB line of June rate cuts if nothing surprising occurs, while the latter reiterated his call for four rate cuts this year.

- China had a steeper-than-anticipated decline in export growth for March, dropping by 7.5% Y/Y in USD terms, significantly below the projected 1.9% decrease as per a survey conducted by Bloomberg.

- March saw China's growth in outstanding aggregate financing decelerate to a record low of 8.7% Y/Y, down from February's 9.0%. New RMB loans totaling RMB3,090 billion were notably weaker than the expected RMB3,600 billion. This led to a significant slowdown in outstanding loan growth to 9.6% Y/Y from 10.1% in the previous month.

- China's State Council pledges to bolster the "high-quality" development of the country's capital market by enhancing supervision and mitigating risks. It released guidelines outline a framework aimed at fostering market development, emphasizing the necessity of establishing a more robust mechanism to safeguard investors' interests and elevating the standard of listed companies.

Macro events: PBoC MLF, Swiss PPI (Mar), EZ Industrial Production (Feb), US Retail Sales (Mar)

Earnings: Goldman Sachs, Charles Schwab, CATL, Anji Microelectronics, Zhejiang Dahua

In the news:

- Iranian notice of attack may have dampened escalation risks (Reuters)

- Chinese developer Vanke Says It’s Addressing Liquidity Pressure, Denies Travel Ban (Bloomberg)

- Metal Traders Get Ready for Fireworks After LME Russia Ban (Bloomberg)

- JPMorgan Chase shares drop after bank gives disappointing guidance on 2024 interest income (CNBC)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration