Global Market Quick Take: Asia – April 16, 2024

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

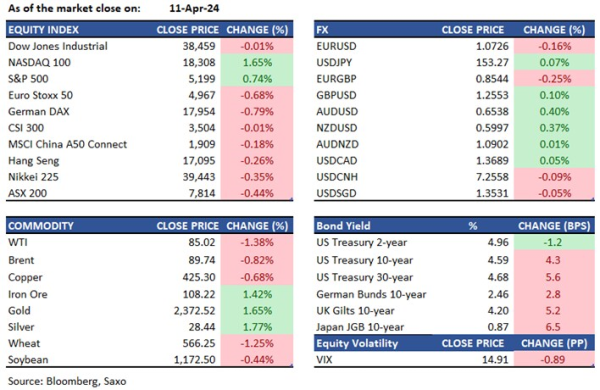

Equities: The S&P 500 Index rallied as much as 0.9% at the open but stocks soon gave ground as Treasury yields surged on a hot retail sales report and the lingering uncertainty about potential escalation of the military conflict between Israel and Iran. At the close, the S&P 500 shed 1.2% and the Nasdaq 100 fell 1.7%, with Tesla one of the worst-performing stocks. Tesla plummeted by 5.6% after Elon Musk emailed staff about a more than 10% job cut aiming at cost cutting. On the other hand, Goldman Sachs gained 2.9% after the investment bank reported Q1 earnings surpassing expectations.

In China, while the CSI 300 Index surged 2.1%, driven by large state-owned enterprises and the CSI Small Cap 500 Index also added 1.2%, the CSI 1000 Index, composed of stocks with market capitalization below those in the CSI 300 and CSI 500, plunged 1%. The CSI 2000 Index, which represents even smaller cap stocks, plummeted 4.1%. The 9 guidelines issued by China’s State Council last Friday emphasise tightening the supervision and regulation of the markets, listed companies, and large shareholders to protect investors, triggering selling in micro-cap stocks in the A-share market despite strong performance in the benchmark indices. Today’s attention in China will be on the release of Q1 GDP, industrial production, retail sales, and fixed asset investments.

FX: The dollar index remained steady on Monday even as no further geopolitical risk was priced in, but a bid came in at the US open with US retail sales beating estimates. Fed’s Williams was dovish on the margin, but geopolitical escalation risks picked up again amid reports of an Israel response to the Iran attack. Safety bid came through in CHF as well, although JPY lagged. EURCHF tested Friday’s lows of around 0.9680 while USDJPY rose above 154 to fresh highs of 154.44 amid higher US yields. Threat of intervention could be key here as yen weakness was seen across the FX board rather than just against USD as was the case post-CPI. EURUSD testing the 76.4% fibo retracement from the October low at 1.0611 while GBPUSD has broken below 200DMA and could test 1.24 with inflation and labor data due in the week ahead. Focus today, however, on USDCAD which risks breaking above 1.38 with Canada CPI due today, and a June rate cut priced only 60%.

Commodities: Crude oil traded lower on Monday as markets ere relieved that Iran’s attack did not bring casualties and awaited Israel’s response. Gold, however, resumed its surge in the late US session despite a stronger dollar, amid reports that Israel is looking to respond and comments from Iran that it will strike back within “seconds” if Israel was to strike back. This tit-for-tat tone keeps markets on edge, and saw silver also running higher for a test of $29 again. Meanwhile, aluminum led the base metals sector higher as the market digested bans on Russian metal being delivered onto the London Metal Exchange. China’s growth metrics will be a key focus in the day ahead.

Fixed income: Much stronger than expected retail sales data saw the 10-year Treasury yield sharply higher by 8bps, reaching 4.60%. The 2-year yield added 2bps to 4.92%.

Macro:

- US retail sales topped estimates and suggested US economic resilience yet again. Headline retail sales rose by 0.7%, above the 0.3% forecast but down from the prior (upwardly revised) 0.9%, the ex-autos measure surged 1.1% from the prior 0.6%, above the 0.3% forecast, while ex-gas and autos rose by 1.0% from the prior 0.5% - showing widespread gains across consumer spending. The control group, which feeds into US GDP, rose by 1.1%, accelerating sharply from the prior 0.3% and above the 0.4% forecast. The Atlanta Fed GDPNow growth estimate for Q1 rises to 2.8% from 2.4% after stronger-than-expected retail sales.

- Fed member Williams said he does not want to speculate on rate moves but in his own view, rate cuts will likely start this year if inflation continues to come down. He said that he does not see the March CPI report as a turning point, nor a game changer.

- The EU may be investigating China's medical device sales, possibly announcing the probe in mid-April. This could lead to measures limiting China's access to EU public tenders, as reported by Bloomberg on April 15th.

Macro events: China GDP (Q1)/Industrial Production (Mar)/Retail Sales (Mar), UK Jobs Report (Mar/Feb), German ZEW Survey (Apr), US Building Permits (Mar), Canada CPI (Mar), US Industrial Production (Mar), New Zealand CPI (Q1)

Earnings: Bank of America, Bank of New York Mellon, Morgan Stanley, PNC Financial Services, Johnson & Johnson, Interactive Brokers, UnitedHealth,

In the news:

- Israel-Gaza live updates: Iran will respond in 'seconds' if Israel strikes back, Iranian official says (ABC News)

- ECB’s Lane Says Current Disinflation Is ‘Necessarily Bumpy’ (Bloomberg)

- Tesla to cut 10% of global workforce (FT)

- Lawrence Wong to take over as Singapore Prime Minister from Lee Hsien Loong on May 15 (CNA)

- BOJ's new policy approach takes shine off its inflation forecasts (Reuters)

- Goldman Sachs tops first-quarter estimates fueled by trading, investment banking (CNBC)

- EU Set to Launch China Probe on Medical Device Procurement (Bloomberg)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration