Global Market Quick Take: Asia – April 18, 2024

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

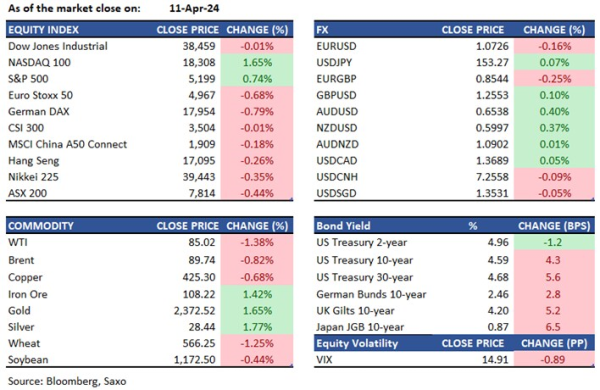

Equities: Even as yields cooled, rate jitters persisted and weighed on US stocks with NASDAQ 100 leading the losses with a decline of 1.2% and S&P 500 down 0.6%. Big hit came from disappointing earnings from European chipmaker ASML with a temporary setback in orders, and this saw US chipmakers taking a plunge as well withy Nvidia down 4% and AMD down nearly 6%. To read more on the outlook for ASML, read this note from our Head of Equity Strategy, Peter Garnry.

Some relief came through in after-hours especially as Micron rose on reports that it is set to receive $6bn in US government grants by next week under the 2022 CHIPS and Science Act. Taiwan’s TSMC will be in focus today, having received $11.6bn in US grants earlier and it also reports earnings today. Video streaming giant Netflix is also set to report first-quarter earnings on Thursday, and subscriber growth will be a key focus.

FX: The US dollar had trouble extending gains on Wednesday with much of the Fed pushback to rate cuts now priced in and markets only expecting the first full rate cut from the Fed in November. The DXY index slipped below 106 which brought a recovery in activity currencies. AUDUSD rose back to 0.6440 after three days of losses and having tested the 0.64 handle, as iron ore prices jumped higher, and Australia’s employment data will be on tap today. NZDUSD also rose back above 0.59 from YTD lows with RBNZ rate cut expectations pushed forward post-Q1 CPI release yesterday. EURUSD bounced higher from 1.06 support to highs of 1.0680 for the day while GBPUSD found support at 1.24 but remained choppy despite hot UK inflation data.

USDJPY is still above 154 even as it eased from the highs of 154.79, and dollar strength from the last few days has become a concern for many EM Asian currencies. Japanese and Korean officials held a trilateral meeting with Janet Yellen, suggesting intervention threat could take a leg up here. USDCNH has also retreated below 7.25 with dollar weakness and PBoC fixing will be on the radar today to assess any devaluation concerns for the yuan.

Commodities: Oil prices slumped sharply overnight with Brent coming back below $88/barrel following a bearish IEA inventory report which showed that US crude inventories rose by 2.7 million barrels last week, expanding to a 10-month high. Geopolitical premium could also start to be reduced with escalation concerns in Middle East taking a backseat. However, US sanctions on Venezuela have been re-imposed, but the impact could be limited. Meanwhile, President Biden announced tariffs on Chinese steel would be tripled to 25%. This could be a symbolic move with Chinese steel making up only 1% of America’s domestic consumption and aluminum for about 4% of total US imports. However, iron ore futures gained over 5%. Gold retreated slightly with geopolitics taking a backseat while Silver was supported by the $28 handle.

Fixed income: Treasury sell-off cooled amid some bargain-hunting with UK CPI coming in hotter-than-expected and equities coming under pressures after the disappointing ASML earnings report. Yields dropped from recent 2024 highs, with 2-year yield failing to break above 5%. The solid 20yr auction also underscored the bid.

Macro:

- There was no major data, but Fed and ECB speakers took centerstage. Fed’s Mester said that they want more information to be sure that inflation is on a sustainable path to 2%, and that there is no hurry to cut rates. Bowman also said that progress on inflation may have stalled. Meanwhile, ECB speakers (Centeno and Nagel) continued to talk about a June rate cut, although Lagarde said that they are watching exchange rates and a weaker EUR could be inflationary. This continues to highlight that there is room for the Fed-ECB divergence to extend, and we discuss in this article how market participants can play that.

- UK CPI came in hotter-than-expected with headline at 3.2% YoY for March vs. 3.1% expected but still cooling from 3.4% last month. Core CPI cooled from 4.5% YoY in Feb to 4.2% YoY in March, but deceleration trends are intact with upside being driven primarily by housing and phone apps and not broad-based. This may rule out the case for a BOE rate cut in May, but the door for a June rate cut is still open.

Macro events: Australia Employment (Mar), US Philly Fed (Apr), US Jobless Claims (Apr 13). Speakers: BoJ Noguchi; ECB’s de Guindos, Schnabel; Fed’s Williams, Bowman, Bostic

Earnings: Netflix, Intuitive Surgical, Blackstone, Marsh & McLennan, DR Horton, Nokia, Schindler, TSMC, L’Oreal

In the news:

- Foreign holdings of US Treasuries hit record high; Japan holdings rise, data shows (Reuters)

- Google lays off employees, shifts some roles abroad amid cost cuts (Reuters)

- Buffett’s Berkshire Targets Narrower Spreads on Yen Bonds as BOJ Bets Ease (Bloomberg)

- Yellen Meets Japan, South Korea Counterparts in Bid to Boost Economic Ties (Bloomberg)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration