Global Market Quick Take: Asia – April 19, 2024

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

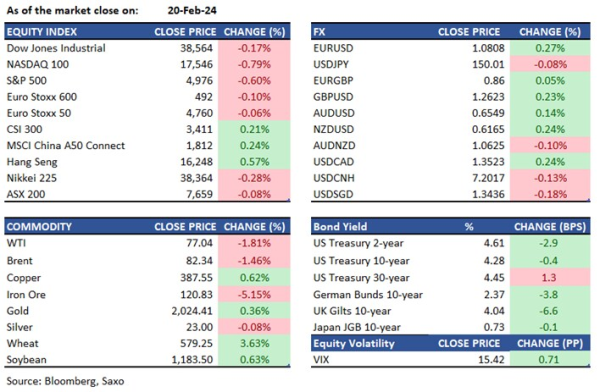

Equities: US equities extended the sell-off, with the S&P 500 closing lower for a fifth consecutive day and getting close to testing the key 5,000-mar. Concerns on inflation and the Fed path are back on the radar after several Fed members are now highlighting the possibility of no rate cuts this year, and Williams also keeping the door open for a rate hike.

Taiwanese chipmaker TSMC, the key chip supplier to Nvidia and Apple, fell 5% as its lowered forecast for overall semiconductor growth offset its strong Q1 results. TSMC also kept its capex budget unchanged, disappointing those expecting an increase. Netflix was also down in the after-hours, despite adding over 9 million subscribers in Q1 as revenue guidance fell short and its plans to stop reporting subscriber numbers from next year spooked investors.

FX: The dollar reversed its slide from earlier on Thursday and the DXY index came back above 106 in the US session as hawkish waves continued both from data and Fed speakers. CAD was the sole gainer on the G10 board but was nearly flat. NOK led the selloff, with USDNOK touching fresh highs of 11.06 as geopolitical risk premium was reduced. Japanese yen was a big focus after G7 comments yesterday hinting that the US may tolerate Japan’s intervention, but USDJPY still traded near its three-decade lows at 154.50+ levels after a brief dip below 154 yesterday. Any move towards 155 will bring heightened fears of intervention from here. EURUSD came under pressure as well as dollar rally resumed, and slipped to 1.0640 after a test of 1.090 failed. AUDUSD attempted a move above 0.6450 with copper and iron ore prices pushing higher, but employment data failed to excite, and pair dropped back to 0.6420 in the US session.

Commodities: Copper prices rallied 2.4% and signals the improving health of the global economy. Focus is also back on fundamentals with copper demand high for green transition and AI but ore downgrades limiting supply. To know more about the dynamics around Copper and copper miners, read this article from head of Commodity Strategy, Ole Hansen. Gold resumed its upside momentum despite hawkish waves from strong US data and comments from Fed’s Williams. Crude oil prices, meanwhile, are on course for a weekly drop amid a stronger dollar offsetting geopolitical concerns.

Fixed income: Treasury sell-off resumed after Fed's Williams alluded to a rate hike tail scenario in the backdrop of a hot Philly Fed survey and steady jobless claims. The 2-year yield got back to the key 5% resistance, while 10-year rose to 4.6%.

Macro:

- US jobless claims again suggested that labor market remains strong. Claims for the week of April 13 were unchanged at 212k, marginally shy of the expected 215k, leaving the 4-wk average unchanged at 214.5k.

- Fed speakers were a key focus, and Bostic repeated that a rate cut may be unlikely this year while Williams and Kashkari added to the hawkish rhetoric. Williams, a key voice in the Fed committee and a voter, even warned that if the data called for higher rates, the Fed would hike.

- Japan’s national CPI for March came in marginally softer-than-expected with headline at 2.7% YoY vs. 2.8% expected and previous. Core CPI was at 2.6% YoY vs. 2.7% expected and the core-core measure was at 2.9% YoY from 3.2% previous and 3.0% expected. This reduces the risk of another rate hike at the BOJ meeting next week, after comments from Governor Ueda earlier that yen-induced inflation will be key to monitor.

Macro events: UK Retail Sales (Mar), Germany PPI (Mar). Speakers: BoE’s Ramsden; Fed's Goolsbee

Earnings: American Express, Schlumberger, Procter & Gamble, China Tower

In the news:

- Netflix Reports Record Profits As Subscriber Growth Tops Estimates (Forbes)

- TSMC beats first-quarter revenue and profit expectations on strong AI chip demand (CNBC)

- Modi Bets on Third Term as India’s Massive Election Kicks Off (Bloomberg)

- No Link Too Tenuous for Retail Traders in China AI Gold Rush (Bloomberg)

- BOJ's Ueda signals possible rate hike if weak yen boosts inflation (Reuters)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.