Global Market Quick Take: Asia – April 3, 2024

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

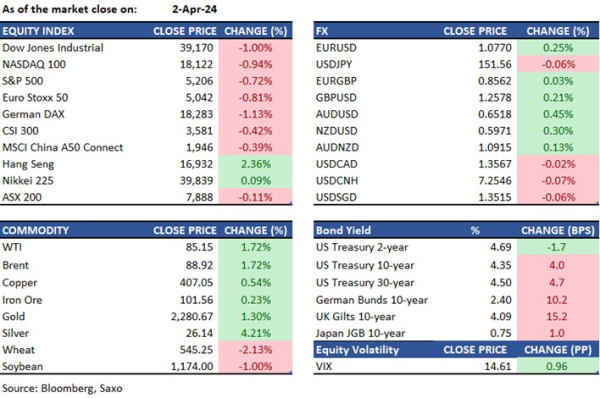

Equities: In the U.S., Investors' risk appetite wanes amid increased expectations of ‘higher-for-longer’ in the Fed’s interest rate path. The S&P 500 shed 0.7% and the Nasdaq 100 declined 0.9%. Healthcare was the worst-performing sector with the S&P 500, driven by sharp falls in Humana, CVS Health, and United Healthcare after the Biden administration announced lower-than-anticipated 2025 Medicare Advantage rates. Consumer discretionary was also among the weakest sectors, dragged by a 4.9% decline in Tesla, which tumbled after releasing data showing a delivery of 386,783 EVs in Q1, substantially below the 457,000 forecasted by analysts, and the 423,000 a year ago quarter. Energy stocks bucked the market decline, with Exxon Mobil, EOG Resources, Philips 66, Marathon Petroleum, and Valero Energy advancing around 2%-4% as crude oil prices surged.

In Japan, the Nikkei 225 managed to tic up 0.1% to stabilize at 39,839, as gains in export names such as electronic appliances makers benefitted from yen weakness offsetting profit-taking selling pressure typical at the beginning of the fiscal year.

In China, the CSI300 pulled back by 0.4% after a 1.7% surge the previous day while Hong Kong’s Hang Seng Index jumped by 2.4%, reflecting improved sentiments after the release of stronger manufacturing PMI data from the mainland. Notably, BOC Hong Kong and Trip.com led the performance of the Hong Kong benchmark, each rising over 9%. Xiaomi also saw a significant 9% increase, driven by strong pre-orders for its newly launched SU7 electric car models. Additionally, oil companies and gold mining stocks surged as crude oil reached 5-month highs and gold hit new highs. Share prices of Macao casino operators advanced 3%-6% following the release of a remarkable 53.1% Y/Y growth in gaming revenue, totalling MOP19.5 billion. This figure represents approximately 75% of the revenue level during the same period in 2019.

FX: The dollar failed to hold onto the 105 handle despite more evidence of US economic strength suggesting markets may have peaked in pricing in a less dovish Fed outcome than what data and communication suggests. Fed Chair Powell speaks today at 16:10 GMT. CHF was the underperformer in G10, with EURCHF heading higher again to re-test the 0.98 handle. Japanese yen also remained in focus with intervention threat lingering into the NFP release on Friday, As USDJPY still trades above 151.50 after touching highs of 151.80. EURUSD was relieved with German CPI only mildly below expectations and rushed higher to 1.0770 on dollar weakness later, while GBPUSD rose to 1.2580. Yuan also saw some gains due to the weaker dollar overnight, but USDCNH still trades above 7.25 and PBoC fixing will remain in focus.

Commodities: Sentiment in commodities is being boosted by strength in US and China economic data as supply side issues also continue to linger. Crude oil prices rose 2% as Iran vowed revenge on Israel for an airstrike on its embassy in Syria, which raises risks to oil supplies. OPEC+ meeting today in focus and supply cuts are likely to be maintained. Copper and iron ore also rallied, Gold touched highs of $2,290 while Silver was up 4% to hit a new two-year high as both Gold and Copper edged higher.

Fixed income: Yields surged for the second day in a row from the intermediate to the long end of the curve. Investors are adjusting to the heightened ‘higher for longer’ expectations after recent economic data pointing to a robust US economy, including the latest JOLTS job openings data on Tuesday. Fed’s Daly and Mester joined the chorus of ‘no urgency’ to cut rates. The 10-year yield rose to as high as 4.40% at one point before settling at 4.35%, 4bps higher from its previous close. The short end outperformed the rest of the yield curve, with the 2-year yield falling 2bps to 4.69%.

Macro:

- US JOLTS job openings for February came in line with expectations at 8.756 mn (exp. 8.75 mn), although January’s was revised lower to 8.748 mn from 8.863 mn, with the quits rate unchanged at 2.2%. Data continues to suggest that the US labor market remains strong and justifies the cautious stance of Fed members towards rate cuts.

- Fed’s Daly and Mester, both voters this year, stuck to a baseline view of three rate cuts this year but caveated by saying that there is no urgency and they want to see more data before easing. Mester also said the May 1st meeting is too soon for a rate cut but later said she would not rule out a June cut. Daly said that there is a real risk of cutting rates too soon.

- German inflation cooled more than expected in March to 2.3% YoY, down from 2.7% in the prior month.

Macro events: OPEC+ JMMC Meeting, EZ Flash CPI (Mar), US S&P Services and Composite Final PMI (Mar), US ISM Services PMI (Mar), US ADP National Employment (Mar), Caixin China Services PMI. Speakers: Fed’s Bowman, Goolsbee, Powell, Barr, Kugler

Earnings: No major releases

In the news:

- Tesla’s Quarterly Deliveries Fall for First Time Since 2020 (WSJ)

- Call between Xi Jinping and Joe Biden conveys stability, deep disconnect in US-China ties: analysts (SCMP)

- UK's Cameron calls for increased NATO spending amid Ukraine conflict (Reuters)

- Amazon to Remove ‘Just Walk Out’ Checkout Technology at U.S. Grocery Stores (WSJ)

- U.S., Japan to agree on subsidy rules on chips, batteries with China in mind (Nikkei Asia)

- India manufacturing PMI surges to 16-year high ahead of elections (Nikkei Asia)

- Toyota reports 20% jump in first-quarter US auto sales (Reuters)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration