Global Market Quick Take: Asia – April 5, 2024

Saxo’s Q2 2024 Outlook titled “The wasted year” is now out. You can read it here.

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

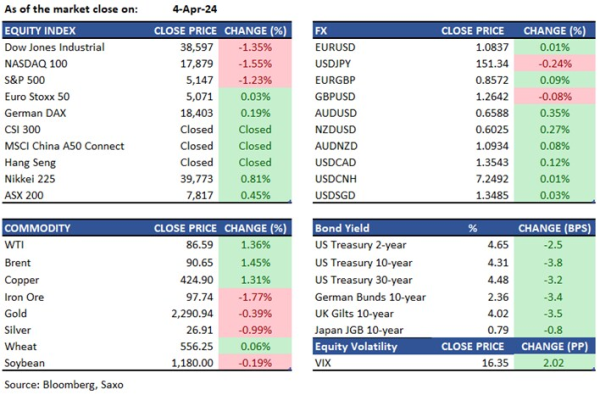

Equities: Another round of comments from Fed officials, being cautious about easing prematurely, including Minneapolis Fed's Kashkari, a non-voting FOMC member this year, who mentioned the possibility of no rate cut at all if inflation moves sideways, weighed on the US equity market. The Nasdaq 100 plunged 1.6%, and the S&P 500 dropped by 1.2% in a broad-based decline. All 11 sectors of the S&P500 finished lower, led by the sharp fall in information technology, health care, and communication services. AMD plummeted 8.3%, making it one of the worst-performing stocks.

In Japan, the Nikkei 225 rebounded, gaining 0.8%, as investors turned their attention to the anticipated increases in dividends and stock buybacks by Japanese companies in the upcoming earnings reporting season. Meanwhile, the mainland China and Hong Kong markets were closed on Thursday for a public holiday, and the mainland bourses will continue to be closed today as the Hong Kong bourse resumes.

FX: Fed commentaries were incoherent rather than hawkish, and the markets were spooked more by geopolitical worries rather than a pushback on rate cut expectations. This saw a safety bid coming through in the dollar in the late US session, marking some reversal of recent gains in other currencies. GBPUSD reversed from highs of 1.2684 to trade around 1.2640, while EURUSD was back at 1.0840 from highs of 1.0877. Safety bid came through to yen and CHF as well. EURCHF saw sharp gains earlier in the session to 0.9840 on Swiss CPI coming in lower than expected, but pair dropped back below 0.9780 in the late US session. USDJPY was also lower, slipping below 151.40. Meanwhile, AUDUSD still ended the day higher supported by gains in commodities.

Commodities: Geopolitical risks have taken a leg up as talk of Iran retaliatory strikes against Israel began to grip the markets. Brent crude extended its recent rally, as a result, and currently trades above $91/barrel. Gold retreated from its recent record high on profit taking and after Fed speakers warned of higher rates for longer. Copper rallied to a 14-month high as further risks to supply emerged on the prospect of a global recovery in demand.

Fixed income: Despite another round of hawkish comments from Fed officials, the US Treasury market was resilient on Thursday, as the selling pressure that was mounting earlier in the week faded away. Rising geopolitical tension in the Middle East and the US job report scheduled to be released on Friday kept traders cautious about pushing yields higher. The 10-year yield fell by 4bps to 4.31%.

Macro:

- Comments from the US Fed speakers lacked a coherent message, signaling the difficulty in interpreting data and putting immense focus on NFP release ahead today. Kashkari (non-voter) was the most hawkish, saying that rate cuts may not be needed this year if progress on inflation stalls. Meanwhile, Mester (voter) said that Fed could be close to the level of confidence needed to bring interest rates lower. Barkin (2024 voter) leant somewhat hawkish, noting it is smart for the Fed to take their time on rate cuts, noting the early 2024 data is less encouraging, and it raises the question of whether the outlook is shifting. Still, markets continue to expect 75% odds of a June rate cut from the Fed.

- US jobless claims rose to 221k in the latest week, above the 214k forecast and rising from the prior 212k to the highest level since the end of January.

Macro events: RBI Announcement, German Industrial Orders (Feb), EZ/UK Construction PMI (Mar), EZ Retail Sales (Feb), US Labour Market Report (Mar), Canadian Labour Market Report (Mar)

Earnings: Yaskawa Electric

In the news:

- Tesla knocks BYD off its perch as world’s largest pure EV makers struggle to win new customers in China’s shrinking market (SCMP)

- Samsung flags 10-fold rise in first-quarter profit as chip prices recover (Reuters)

- Use of Fed Central Bank Tool Grows as Cash Stockpiling Continues (Bloomberg)

- US small businesses dial back hiring plans again, NFIB says (Reuters)

- Disney to start cracking down on password-sharing from June, CEO Iger says (Reuters)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration