Global Market Quick Take: Asia – April 8, 2024

Saxo’s Q2 2024 Outlook titled “The wasted year” is now out. You can read it here.

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

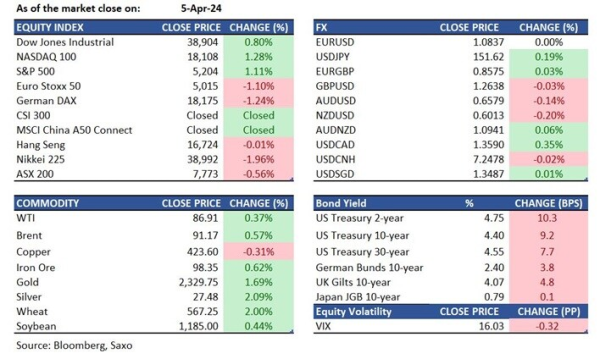

Equities: US stocks shrugged off the higher bond yields triggered by a strong job report and chose instead to focus on the resilience of the economy’s positive implications on corporate earnings. The S&P 500 staged a broad-based rally with all of its 11 sectors finishing 1.1% higher at 5,204 on Friday, led by communication services, industrials and information technology. GE surged 6.1%, topping the performance of the S&P 500. The tech-heavy Nasdaq 100 gained 1.3%. Tesla shed 3.6% following a Reuters report that Tesla has scrapped its plan to make low-cost EVs while focusing on developing robotaxis.

In Japan, the Nikkei 225 plummeted 2% to 38,992 as investors trimmed positions amid rising tensions in the Middle East that saw oil prices higher and stirring up risk-off sentiments, coupled with cautious corporate earnings forecasts. The mainland Chinese markets remained closed for a holiday while Hong Kong’s Hang Seng Index finished nearly unchanged in a lackluster session.

On April 8, Shimao Group announced that China Constructtion Bank (Asia) filed a winding-up petition at the High Court of the Hong Kong SAR against the company.

FX: The reaction of the FX markets to the hot US jobs report was short-lived, as the dollar’s jump to 104.70 was erased quickly. Dollar ended the week marginally lower despite hawkish Fedspeak and US exceptionalism in the week, signaling that much of the hawkishness may have been priced in for now. NOK was the G10 outperformer for the week, as USDNOK slid below 10.8 on oil price gains. Sharp jump in Treasury yields however saw Japanese yen weakening again, and USDJPY remains in the intervention threat zone of 151.50+. USDCAD rose above resistance at 1.3615 to its YTD lows amid a soft Canadian jobs report where unemployment rate rose to 6.1% from 5.9%. EURUSD supported at 1.08 for now and GBPUSD stays above 1.26.

Commodities: Oil prices pushed lower at the start of the new week in Asia after Brent touched $92/barrel levels on Friday and closed at its highest levels in over five months. Geopolitical tensions have underpinned gains recently, but Iran risks remained in check over the weekend and reports are suggesting that talks of a ceasefire in Mideast are progressing. Gold also retreated from post-NFP highs of $2,330 as geopolitical premium was being taken off, and Silver followed after 10% gains last week. Copper prices also turning lower as the week begins and focus will be on China’s return from holidays and their yuan fixing.

Fixed income: Strong gains in employment in both the non-farm payroll establishment survey and the household survey, a decline in the unemployment rate, and a rebound in the workweek all pointed to a robust US labour market. As a result, Treasuries sold off across the yield curve. The 2-year yield finished 10bps higher at 4.75% and the 10-year yield added 9bps to settle at 4.40%. Investors’ focus is turning to the CPI inflation data and the FOMC minutes on Wednesday. Core-CPI is expected to dip modestly to 0.3% M/M from 0.4% and 3.7% Y/Y from 3.8%. Regarding the FOMC minutes, investors will scrutinize the discussion on a potential slowing down of the runoff of the Fed’s securities holdings, or quantitative tightening. Given Powell's repeated use of the phrase 'fairly soon' in the latest post-FOMC press conference, it's probable that the Fed will announce a reduction in the pace of balance sheet runoff during the May 1 FOMC meeting, with implementation expected to begin in June. For a discussion on the reduction in the pace of the QT, please refer to this article.

Macro:

- US jobs report was hot once again. Headline NFP added 303k jobs in March, above the 200k forecast, the 270k prior. The unemployment rate eased to 3.8% from 3.9%, despite expectations for it to be left unchanged while the labour force participation rate rose to 62.7% from 62.5%. While the report once again shows that US economy remains resilient in the face of high interest rates, focus shifts to US CPI release this week which will be a bigger test of whether the recent inflation bump is a trend or not.

- Fedspeak tilted generally hawkish with Bowman saying that it is not yet time for the US to consider cutting rates, while Barkin said the March NFP was very strong. Logan (non-voter) said it is too soon to think about cutting rates, given upside risks to inflation. Markets are now expecting less than three rate cuts this year and the odds of a July rate cut are lower at 91%.

- China’s PBOC announced that the central bank will provide RMB 500 billion in loans to banks at a preferential rate of 1.75%. These loans are intended for banks to extend 1-year credits to industries, supporting technological innovation and enhancing industrial capabilities.

- During the three-day Qingming Festival holiday, China's domestic tourist travels reached 119 million, marking an 11.5% increase from the same period in 2019. Domestic tourism spending rose to RMB 54 billion, reflecting a 12.7% growth compared to the same period in 2019. In other words, spending per person/trip surpassed the pre-pandemic level.

- US Treasury Secretary Janet Yellen voiced concerns in Beijing about China exporting overcapacity in new energy vehicles and solar modules to the U.S. Expectations are for further contention between the two countries in these industries in the coming months, as trade and national security become focal points in the upcoming US presidential and congressional elections. For a more detailed analysis, please refer to our recent article.

- The People’s Bank of China increased its gold holding to 72.74 million troy ounces in March in its 17th consecutive month of buying.

Macro events: Swiss Unemployment Rate (Mar), German Trade Balance (Feb)/Industrial Output (Feb), EZ Sentix Index (Apr)

Earnings: Welcia Holdings, Create SD Holdings, Mani Inc, Fuji Co, Samty, CK Infrastructure, Hiday Hidaka Corp.

In the news:

- Tesla scraps low-cost car plans amid fierce Chinese EV competition (Reuters)

- Toyota valuation doubles in new CEO's 1st year, nearing Tesla (Nikkei Asia)

- Israeli military says it reduces troops in south Gaza (Reuters)

- Yellen meets China's Premier Li amid 'tough conversations' on industry (Nikkei Asia)

- Dutch set to comply with U.S. demands that chipmaking giant ASML stop servicing some equipment it has sold to Chinese customers (Reuters)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration