Global Market Quick Take: Asia – April 9, 2024

Saxo’s Q2 2024 Outlook titled “The wasted year” is now out. You can read it here.

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

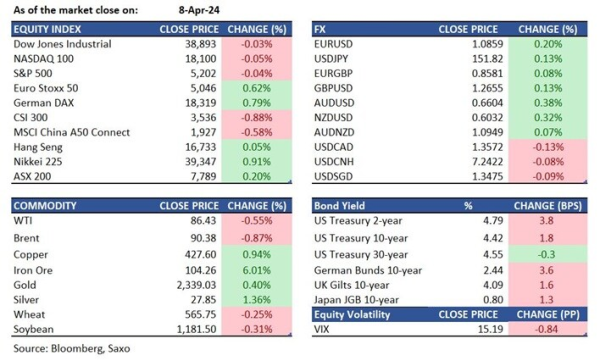

Equities: The S&P 500 finished the session nearly unchanged at 5,202, while the Nasdaq 100 shed 0.1% to 18,100 in a muted session. Tesla rebounded 4.9% as investors reacted to Elon Musk’s announcement last Friday of an August unveiling of the long-awaited self-driving Robotaxi. Coinbase Global surged 6.7%. In Asia, Japan’s Nikkei 225 rallied by 0.9% to 38,893, while China’s CSI300 slid 0.9%. The Hang Seng Index climbed modestly by 0.1% to 16,733. Treasury Secretary Yellen said in Beijing that the U.S. is not seeking to decouple with China, but she reiterated her criticism of China exporting its overcapacity in green energy products to the U.S.

FX: The dollar was unable to go higher again despite yields being sticky on the 3-year inflation expectations surging higher. The weaker dollar pushed activity currencies higher, and NOK and AUD gained despite oil prices inching slightly lower on hopes of a ceasefire in the Middle East. EURNOK drifted lower to 11.60 from highs of 11.66 yesterday. AUDUSD rose back above 0.66 with 6% gain in iron ore prices and broader commodities. EURUSD surged back above 1.0850 and 100DMA test comes in at 1.0874, while USDCAD was back below 1.36 and both ECB and Bank of Canada could show a dovish tilt at their meetings this week. USDJPY remains pinned below 152 and eyes will be on the US inflation release on Wednesday. Bitcoin was flying again, up over 3% to inch above $72k again but reversed lower in Asia, while Ethereum was up about 9% as Bitcoin halving draws closer.

Commodities: Crude oil prices reverted back to gains after a drop to sub-$90/barrel level on hopes of a ceasefire in the Middleeast conflict, as reports suggested that Hamas rejected the Israel ceasefire offer. EIA’s monthly oil report will be in focus today. Gold and copper were also at fresh highs. Gold demand remained underpinned by central bank demand from China and India, as well as retail demand from China. US CPI will be the next big focus.

Fixed income: The 10-year yield climbed another 2bps to 4.42% on Monday after the post-employment report spike last week. At one point, the 10-year yield advanced to 4.46% in European hours but pulled back in the New York trading hours. The 2-year yield rose 4bps to 4.79%.

Macro:

- Fed’s Kashkari was on the wires again, after his comment last week that no rate cuts may be needed this year. The Fed Minneapolis President the inflation rate is running around 3% and the Fed has to get back down to 2% suggesting that the inflation fight is not over. On labor market, he said that it is not red hot like last year, but still tight.

- The NY Fed inflation expectations saw the 1-year measure unchanged at 3.0%, but the 3 year expectations rose to 2.9% to 2.7%.

Macro events: EIA STEO

Earnings: Bank of Ningbo, Hengli Petrochemical

In the news:

- Jamie Dimon Warns U.S. Might Face Interest-Rate Spike (WSJ)

- US Treasury's Adeyemo warns 'malign' actors are using virtual assets (Reuters)

- Biden’s Student-Loan Plan Seeks to Slash Debt for 30 Million Americans (WSJ)

- China Has Too Much at Stake in Industry Push to Listen to Yellen (Bloomberg)

- US to award Samsung up to $6.6 billion chip subsidy for Texas expansion, sources say (Reuters)

- Shin-Etsu to bolster chip supply chain with first Japan plant in 56 years (Nikkei Asia)

- TSMC expands U.S. investment to $65bn after securing $6.6bn grant (Nikkei Asia)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration