Global Market Quick Take: Asia – August 30, 2024

Key points:

- Equities: Dow Jones record high while Nvidia weighing on technology

- FX: Euro trading the weakest this week in G10

- Commodities: Gold remained close to a record high

- Fixed income: US bonds are on track for strongest performance in three years

- Economic data: Eurozone CPI, US PCE

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

In the news:

- Stock Market Today: S&P 500 ekes gain as Nvidia slip weighs (Investing)

- Tokyo CPI, core inflation up slightly more than expected in August (Investing)

- Dell raises annual forecasts on strong AI server demand (Investing)

- Gap shares rise after it resumes trading, Q2 results show growing sales and margin (Yahoo)

- Ulta Beauty reports disappointing earnings after Warren Buffett's Berkshire Hathaway takes stake (Yahoo)

- Luluemon shares fall in afterhours trade on weak results, guidance (Yahoo)

- Chipmaker Marvell Tech beats quarterly revenue estimates amid AI surge (Reuters)

Macro:

- The 2nd estimate of US Q2 GDP was revised higher to 3.0% from 2.8%, beating expectations of it being left unchanged. Consumer Spending was also revised up to 2.9% from 2.3%, while the GDP deflator was revised up to 2.5% from 2.3%, above the expected 2.3%. Core PCE was revised down to 2.8% for Q2 from the 2.9% prior. This data, however, has limited implication for what the Fed does at the September meeting given it is backward-looking.

- US initial jobless claims rose 231k in the w/e 24th August, slightly shy of the expected, 232k, and the prior, 233k, but continues to hover around the 230k mark and highlight that the labour market is not seeing any further weakness or notable softening, which suggests the Fed will likely go with a 25bps cut in September. However, the August non-farm payrolls data will have a bigger sway in Fed’s policy decision.

- Germany’s August CPI saw a sharp drop to the 2% target from 2.6% in July, supporting the case for an ECB rate cut in September. Euro-area inflation figures are due today and consensus expects headline inflation to fall to 2.1% YoY in August from 2.6% in July but core falling more slowly to 2.8% from 2.9% previously.

- Japan’s Tokyo CPI came in higher-than-expected for August, supporting the case for further rate hikes from Bank of Japan. Headline Tokyo CPI rose to 2.6% YoY from 2.2% in July and 2.3% expected. Core CPI also higher at 2.4% YoY in August from 2.2% prior and expected and the core-core measure rose to 1.6% YoY from 1.5%.

- US PCE Preview: Focus today will be on the core PCE print and personal income and spending numbers for July. Consensus for core PCE stands unchanged at 0.2% MoM but slightly higher on YoY basis at 2.7% from 2.6% in June. However, with the Fed having hinted rate cuts clearly, a print close to 0.4% MoM may be needed in the core measure to derail that. The PCE is also unlikely to prompt the market to price in a larger rate cut for September in case of softening, so bigger focus still remains on labor market indicators.

Macro events: French Prelim CPI (Aug), EZ Flash CPI (Aug), Italian Flash CPI (Aug), US PCE (Jul), US University of Michigan Final (Aug)

Earnings: Frontline, JinkoSolar, MiniSo

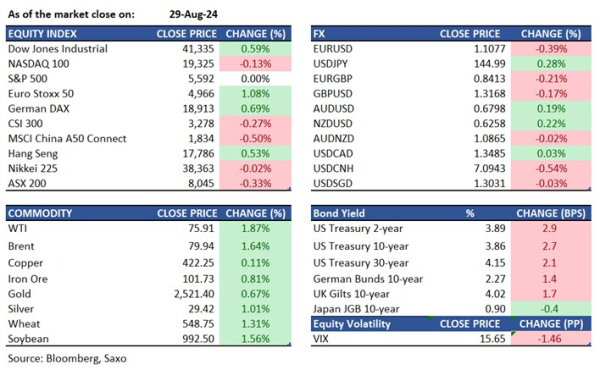

Equities: S&P 500 and Nasdaq remained mostly unchanged, while the Dow Jones hit a new record high, rising over 200 points. Investors were evaluating recent economic reports and Nvidia's results. Although Nvidia's quarterly profit and revenue guidance were better than expected, they didn't meet the high expectations, causing its shares to drop by 6%. Meanwhile, the US GDP growth for Q2 was revised up to 3% from 2.8%, and personal spending, a key economic driver, increased by 2.9%, higher than the earlier estimate of 2.3%. Additionally, initial jobless claims fell by 2,000 to 231,000 from the previous week. Corporate earnings also affected the market, with Salesforce, Best Buy, and Affirm shares performing well on strong results, while Dollar General fell by 30% after lowering its full-year outlook due to weaker sales.

Fixed income: Treasuries fell due to unexpected upward revisions in US 2Q GDP components. Treasury futures hit their lowest levels of the day, with losses persisting after a weak 7-year note auction. Treasury yields rose by 3 to 3.5 basis points, with the US 10-year yields closing around 3.87%, underperforming German bunds. The 7-year note auction tailed the WI by 0.9 basis points, with primary dealer awards at 13.7% and direct awards at 11.2%, the lowest since March 2020. In August, the US money-market fund industry attracted $127 billion, the largest monthly inflow of the year, as investors sought high yields ahead of expected Federal Reserve rate cuts. Total assets reached a record $6.26 trillion. US bonds are set for their best performance in three years as traders anticipate Federal Reserve rate cuts. Treasuries have returned 1.7% this month through August 28, marking a fourth consecutive monthly gain and a year-to-date rise of 3%, according to the Bloomberg US Treasury Total Return Index.

Commodities: Oil prices held steady after Thursday's surge, driven by positive US economic data and worsening supply disruptions in Libya. West Texas Intermediate traded below $76 a barrel after a 1.9% gain, while Brent crude closed near $80. Despite this, oil is on track for a second consecutive monthly loss due to weak demand in China and potential OPEC+ supply restoration. Gold remained near a record high at around $2,520 an ounce as traders awaited a US inflation report that could influence Federal Reserve rate cuts. Lower borrowing costs typically benefit gold. Aluminum continued its decline from a two-month high due to concerns about China’s demand recovery. Since Tuesday's close, aluminum has fallen by about 3%, trimming its strong monthly gain. The spot three-month spread on the London Metal Exchange was $27 a ton.

FX: The strength in US data overnight, coming from GDP and jobless claims, fueled gains in the US dollar as expectations about a 50 basis points rate cut in September were questioned. Still, market pricing has not changed a lot and August jobs data is awaited. Swiss franc weakened the most among the major currencies, although the Japanese yen pared some of its weakness. The euro was on the backfoot, falling back below 1.11 against the US dollar and testing 0.84 against the British pound as weaker German inflation data supported the case for an ECB rate cut in September. Commodity currencies, meanwhile, erased their earlier strength as equities came under pressure.

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.