Global Market Quick Take: Asia – March 28, 2024

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

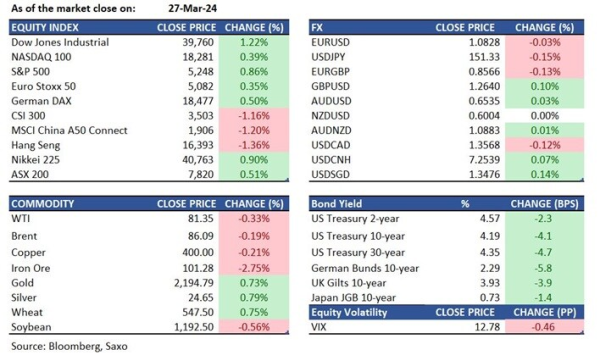

Equities: Risk sentiments abounded in the US equities market. Trump Media & Technology added 14.2% after surging 16% the day before. The S&P 500 gained 0.9% to 5,248 while the Nasdaq 100 climbed 0.4% to 18,281. Merck surged 5% following the approval of a potential blockbuster drug. Nvidia dropped by 2.5%, pulling back for the second day in a row. The US equity market will be closed for the Good Friday holiday on March 29. For long-term investors, read this Saxo article highlighting some attractive sectors for the longer term.

In Japan, the Nikkei 225 rallied amid a weaker Yen, rising 0.9% to 40,763, having its record highs in sight.

In Hong Kong, market sentiment soured as Alibaba's share price dropped 2.1% following the cancellation of its logistics subsidiary, Cainiao, coupled with persistent anxiety about a weaker renminbi dragged down by the Japanese Yen which hit a 34-year low on Wednesday. Also weighing on the market, EV stocks plunged 3%-6%, driven by a downbeat 3.6 million volume guidance from BYD, falling short of the 3.7 million expected by analysts. Factoring in the fast growth in exports, the growth in the domestic EV market looks decelerating and dampens the share prices of other EV stocks. The Hang Seng Index dropped by 1.4% and the mainland’s CSI300 finished 1.2% lower. The Hong Kong market has a busy earnings calendar today ahead of the long weekend starting on Friday.

FX: On Wednesday, USDJPY surged to 151.97, reaching its highest level in 34 years, before slightly pulling back to around 151.30. Japan's Finance Minister, Shunichi Suzuki, issued a cautionary statement, indicating the Ministry of Finance's readiness to take "decisive steps" in reaction to currency fluctuations. Later in the day, the Ministry of Finance, the Bank of Japan, and the Financial Services Agency held an emergency meeting to discuss about the weakening of the yen. In the briefing from the meeting, Vice Finance Minister Masato Kanda said he “won’t rule out any steps to respond to disorderly FX moves”, hinting at the potential for foreign exchange intervention. He went on to say that the BOJ could respond with monetary policies as well if the yen’s fluctuations affect the economy and inflation.

Commodities: Oil pulled back slightly as prices bounced from intraday lows after a smaller-than-expected weekly increase in commercial crude inventory according to data released by the Energy Information Administration. Precious metals rallied modestly with gold and silver trading at around 2190 and silver to 24.60 in Asian morning on Thursday.

Fixed income: In the absence of economic data and ahead of the PCE data scheduled to be released on Friday when the market is closed to observe the Good Friday holiday, Treasuries rebounded moderately, with yields falling 2bps to 5bps across the yield curve. Investor demand was strong for the $43 billion 7-year notes auction. At the close, the 10-year yield was 4bps lower at 4.19%. Today the Treasury market will close early.

Macro:

- The S&P affirmed the long-term and short-term sovereign credit ratings of the United States at AA+ and A1+ respectively and maintains its assessment of the credit rating outlook of the US as ‘stable’.

- In the first two months of the year, China's industrial profits amounted to 9140.6 billion yuan, marking a turnaround from a 2.3% decline the previous year to a positive growth of 10.2%. Looking at sectoral performance, profits in mining declined by 21.1% year-on-year, while those in manufacturing grew by 17.4% and utilities increased by 63.1%. Among the 41 major industries, 29 experienced year-on-year profit growth. Notably, computer, communication, and other electronic equipment manufacturing saw profits double.

Macro events: On Thursday: US Initial & Continuous Jobless Claims (weekly), US Chicago PMI (Mar), US Pending Home Sales U of Michigan Consumer Survey (March, Final), US GDP (Q4 3rd revision); On Friday: US PCE and core PCE inflation (Feb), US Persona Income and Consumption (Feb )

Earnings: Bank of China , China Construction Bank, Agricultural Bank of China, Postal Savings Bank of China, China International Capital Corporation, China Galaxy Securities, Haitong Securities, China Pacific Insurance, China Overseas Land & Investment, China Vanke, Chinasoft, Great Wall Motor, Dongfeng Motor, Guangzhou Auto, Brilliance China, Changjiang Electric, Jiangxi Ganfeng Lithium.

In the news:

- Fed's Waller still sees 'no rush' to cut rates amid sticky inflation data (Reuters)

- BOJ board divided over economic strength upon negative rate exit (Nikkei Asia)

- US Is Asking Allies to Tighten Servicing of Chip Gear in China (Bloomberg)

- Xi Jinping to China’s central bank: restart treasury-bond trade, after 2-decade hiatus (SCMP)

- Oil Heads for Quarterly Advance as OPEC+ Holds the Line on Cuts (Bloomberg)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration