Global Market Quick Take: Asia – May 7, 2024

Key points:

- Equities: US stocks end higher, Japan and China markets in focus

- FX: Yen weakness returns, AUD needs more than just a hawkish RBA to extend gains

- Commodities: Wheat and silver led gains

- Fixed income: Refunding auctions in focus this week.

- Economic data: RBA decision, Fed’s Kashkari

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

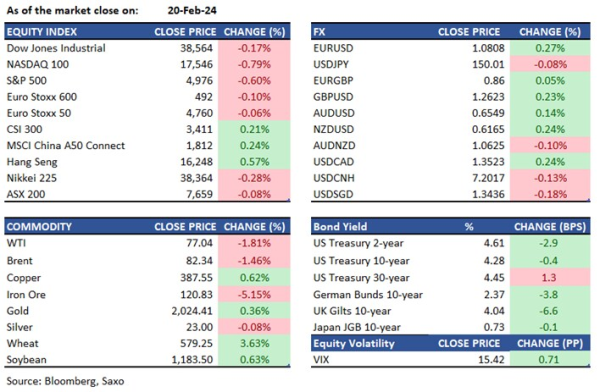

Equities: US stocks extended gains for the third consecutive day, as sentiment remains buoyed by expectations of Fed rate cuts post-NFP miss, as well as on the back of a strong earnings season and increasing shareholder returns. Russell 2000 and NASDAQ 100 led the gains, up 1.2% and 1.1% respectively. Tech and chip sentiment remained upbeat, with Super Micro Computer, Micron and Nvidia up 6%, 4.7% and 3.8% respectively. Warren Buffett’s Berkshire Hathaway was up 1% after reporting a quarterly results over the weekend that included a 40% jump in Q1 operating earnings from a year earlier. Apple fell close to 1% as Buffett cut his stake, despite remaining optimistic about the iPhone-maker’s business. Focus could turn to Wall Street report that Apple is developing AI chips for data centers. Earnings focus today on Walt Disney, and energy major such as Duke Energy and Occidental Petroleum.

Over in Asia, Japan markets returned from holiday opening 1.5% higher on Fed rate optimism and yen back on weakening trend after intervention-driven gains. China markets also closed higher on Monday, with CSI 300 up 1.5% after Golden Week holiday and Hong Kong’s HSI clocking in another 0.6% gains to rise to 8-month highs above 18,500.

FX: The US dollar traded sideways on Monday after ending lower for a second consecutive week. This week is light on macro data and focus will likely remain on earnings and geopolitics. JPY was back in focus with intervention seemingly out of the way, and USDJPY traded back above 154 as FX Chief Kanda saying that intervention may not be necessary if markets are orderly. This came after some remarks from Janet Yellen over the weekend saying that they would expect interventions to be rare and consultation to take place. USDJPY faces a test of the 21DMA at 154.60. AUDUSD has remained steady above 0.66 after the post-NFP surge on Friday, and RBA posturing will be key today, but markets are already priced in aggressively. USDCNH traded back above 7.20, as onshore China markets reopened, and CNY midpoint fixing was back below 7.10 but yen weakness will be key for Chinese authorities once again.

Commodities: Geopolitics was back in the driving seat for crude oil traders after last week’s drop, with prices rising as Israel rejected a ceasefire proposal for Gaza strip that was accepted by Hamas. Demand outlook remains supported by expectations of Fed’s rate cuts, and focus today will be on the EIA outlook report. Base metals pushed higher amid the better risk-on tone across markets. Copper was back in gains as China markets reopened, and Gold prices also gained as expectations of rate cuts rose. Silver led with over 3% gains, and agri commdoities also extended gains with Wheat up over 4%.

Fixed income: Treasuries were choppy in post-NFP ranges with no major data ahead of refunding auctions. More detail can be found in this article.

Macro:

- Fed speakers were on the wires. NY Fed President Williams said that "eventually" there will be rate cuts, but noted that the economy is still healthy, while it is growing more slowly. Richmond Fed President Thomas Barkin said that inflation data this year is "disappointing...job is not yet done"; he is confident that the current restrictive level of rates can curb demand enough to bring inflation to target, one again reiterating high for longer, not higher for longer.

- RBA preview: The Reserve Bank of Australia is set to announce its rate decision today, and is expected to keep the cash rate unchanged at 4.35%. Inflation has remained hot in Q1, but economy is losing steam, as seen from latest retail sales print. Meanwhile, market expectations for interest rates have also gone up with a rate hike back on the table, and forecasts will be key. As such, RBA is likely to keep a hawkish posturing but question is if that will be enough reason to bid AUD with market pricing still looking aggressive. Markets will likely need a rate hike, or an explicit tightening bias from the RBA, for AUD to extend its upside. The decision is due at 0430 GMT (1230 SGT) with Governor Bullock’s press conference an hour later.

Macro events: RBA Announcement, EIA STEO; Swiss Unemployment (Apr), German Trade Balance (Mar), EZ Construction PMI (Apr), Fed’s Kashkari

Earnings: UBS Group, Siemens Healtineers, Nintendo, BP, Duke Energy, Arista Networks, McKesson, Walt Disney, Ferrari, TransDigm, UniCredit, Suncor Energy, Coloplast, Sampo, Infineon Technologies, Leonardo, Geberit, Datadog, Coupang, Rockwell Automation, Occidental Petroleum

News:

- Apple Is Developing AI Chips for Data Centers, Seeking Edge in Arms Race (WSJ)

- Israel Says a Cease-Fire Plan Backed by Hamas Falls Far Short (Bloomberg)

- VinFast’s EV Ambitions Get a Reality Check as Shares Plunge 65% (Bloomberg)

- US banks report weaker loan demand, Fed survey says (Reuters)

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.