Global Market Quick Take: Asia – September 11, 2024

Key points:

- Equities: Oracle rallied 11.5% after beating earnings estimates

- FX: Canadian dollar hurt by steep falls in crude

- Commodities: WTI and Brent crude hit lowest levels since 2021

- Fixed income: Yield curve bull steepens

- Economic data: US CPI, UK July GDP

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

In the news:

- US stock futures inch lower with CPI data, Harris-Trump debate on tap (Investing)

- Fed's upcoming projections to signal deeper cuts than previously expected: Citi (Investing)

- JPMorgan stock slumps as interest income warning rattles market (Investing)

- GameStop reports fall in revenue, files for 20 million share offering (Investing)

- Oil prices tumble on growth worries, stocks diverge (Yahoo)

- Oracle shares jump as AI push perks up cloud demand (Reuters)

Macro:

- UK labor data came in mixed with average weekly wages cooling to 4.0% YoY for the 3 months to July, softer than 4.1% expected and 4.6% prior (revised higher from 4.5%). However, the unemployment rate dipped to 4.1% in July from 4.2% prior as expected while the job growth at 265k was stronger than 97k prior and 123k expected. The data is not weak enough to prompt a cut from Bank of England next week and hasten the pace of rate cuts.

- US CPI preview: As the Federal Reserve shifts focus from inflation to the labour market and prepares for an interest rate cut next week, US inflation remains above the Fed’s target, with headline inflation at 2.9% YoY and core inflation at 3.2%YoY as of July. While headline inflation is expected to drop to 2.5% in August, core inflation is expected to stay steady, suggesting persistent inflationary pressures. To read a full preview of US inflation due today, go to this article.

Macro events: UK GDP Estimate (Jul), US CPI (Aug)

Earnings: Manchester United, Tsakos Energy, Oxford, Lesaka

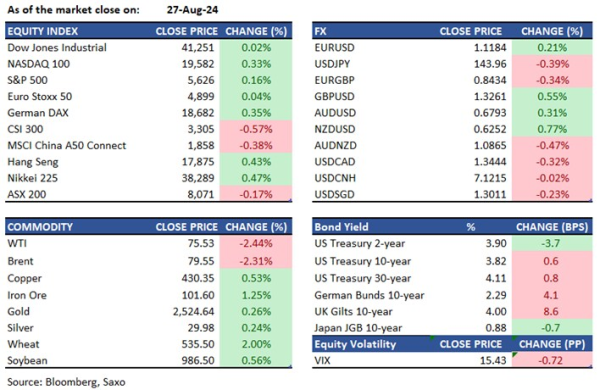

Equities: US stocks ended mixed on Tuesday as investors geared up for a key inflation report tonight that could shape the Federal Reserve's next interest rate moves. The S&P 500 rose by 0.4%, logging its second consecutive day of gains, while the Dow Jones slipped by 92 points due to significant declines in banking stocks. JPMorgan dropped 5.2% after lowering its 2025 net interest income forecast, and Goldman Sachs fell 4.4% following weak trading revenue projections. Tech stocks offered some support, with Nvidia (+1.5%), Microsoft (+2.1%), and Amazon (+2.4%) driving a 0.9% increase in the Nasdaq 100. Oracle shares jumped 11.5% after beating earnings estimates and securing a deal with Amazon Web Services. However, Apple dipped 0.3% after losing a court case over its $14 billion tax dispute in Ireland. Political events also added to market uncertainty, with Kamala Harris and Donald Trump set to participate in their first televised debate at 9pm ET.

Fixed income: Treasury futures held steady as investors awaited US inflation data and the Trump-Harris debate. The yield curve bull-steepened as WTI crude futures fell by up to 5%. The 10-year yield dropped 6bps, while the German 10-year yield declined 4bps. A three-year note sale had a high yield 1.7bps below the when-issued yield, indicating strong demand. Treasuries rose sharply as oil prices declined and regulators proposed less-onerous capital requirements. The three-year note auction drew strong demand despite its low yield, boosting sentiment for upcoming 10- and 30-year offerings. Yields were richer by 4bps-6bps led by front-end and intermediate tenors. The 10-year yield ended around 3.645%, near the day's lows, outperforming the German 10-year by 1.5bps. The $58 billion three-year note auction at 1pm was awarded at 3.440%, the lowest since August 2022 and about 1.7bps below expectations.

Commodities: Gold rose by 0.41% to $2,516, driven by a risk-off sentiment in equities and oil, and declining yields ahead of the CPI release and the Fed meeting. WTI crude futures dropped by 4.31% to $65.75, the lowest since December 2021, due to investor concerns despite Tropical Storm Francine's impact. Brent crude also fell by 3.69% to $69.49, marking its lowest close since December 2021. OPEC has slightly reduced its oil-demand growth forecast, now expecting demand to grow by 2.03 million barrels per day this year and 1.74 million barrels per day in 2025, down from previous estimates of 2.11 million and 1.78 million barrels per day, respectively. Total demand is projected to reach 104.2 million barrels per day in 2024 and 106 million barrels per day in 2025.

FX: The US dollar remained in a tight range in Tuesday’s session as focus turns to US presidential debate and the inflation print due later today. Low yielding currencies such as Japanese yen and Swiss franc outperformed the major currencies once again, given a sharp fall in Treasury yields helped to close the rate differentials with the US, making these currencies more attractive. Meanwhile, the Canadian dollar was the underperformer, weighed by steep selling in the crude complex. Bank of Canada governor Macklem’s dovish comments further added to the pressure on CAD, especially as markets are questioning the odds of a 50bps cut from the Fed next week. Other activity currencies were more mixed, with Kiwi dollar and British pound closing higher but Australian dollar weighed down by China deflation concerns and the fallout in commodity prices.