Global Market Quick Take: Asia – September 6, 2024

Key points:

- Equities: Nio saw its stock surge by 14.3% after strong Q2 deliveries

- FX: USD is back under pressure ahead of NFP

- Commodities: WTI crude trades near $69 amid demand concerns and supply issues

- Fixed income: Money-market fund assets hit record $6.3 trillion

- Economic data: US non-farm payrolls

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

Disclaimer: Past performance does not indicate future performance.

In the news:

- Stock market today: S&P 500 slides on fresh economic worries ahead of jobs report (Investing)

- Broadcom forecasts lukewarm quarterly revenue despite AI chip surge, shares fall (Yahoo)

- NIO Q2 Earnings: EPS Beat, Deliveries Growth, Strong Q3 Outlook And More (Yahoo)

- UiPath sees 10% revenue jump on ‘increasing need’ for AI; stock rallies (MarketWatch)

- Fresh jobs data tests how deeply Fed will cut rates ahead of government payroll report (Yahoo)

- DocuSign stock falls despite better-than-expected earnings, guidance (Yahoo)

- Japan July household spending rises, weaker than expected (Investing)

Macro:

- US ISM services slightly rose to 51.5 from prior and expected 51.4. Looking at the sub-components, employment fell to 50.2 from 51.1 but remained in expansion, with prices paid and new orders lifting to 57.3 (prev. 57.0) and 53.0 (prev. 52.4), while business activity fell to 53.3 from 54.5. Inventories lifted back above 50 to 52.9 (prev. 49.8), while backlog of orders, new exports orders, imports, and inventory sentiment all tumbled. The report continued to highlight that some sections of the US economy continue to be resilient.

- ADP survey labor data sent a dovish signal as national employment fell to 99k in August from the prior (revised lower) 111k, beneath the expected 145k. All attention now turns to payrolls data due today which is likely to be the key determinant of whether the Fed cuts by 50bps or 25bps this month. Saxo’s preview of the payrolls data can be found here.

- US jobless claims (w/e 31st Aug) remained within recent ranges, but slightly dipped to 227k (prev. 232k, exp. 230k), leaving the 4wk average at 230k (prev. 231.75k). Continued claims (w/e 24th Aug) also fell to 1.838mln from 1.860mln, shy of the expected 1.865mln and outside the bottom end of the guidance range.

Macro events: Japan Household Spending (Jul), German Industrial Output (Jul), EZ Revised GDP (Q2), US NFP (Aug) – preview here, Canadian Unemployment/Wages (Aug)

Earnings: BigLots, ABM, Brady, Genesco, BRP

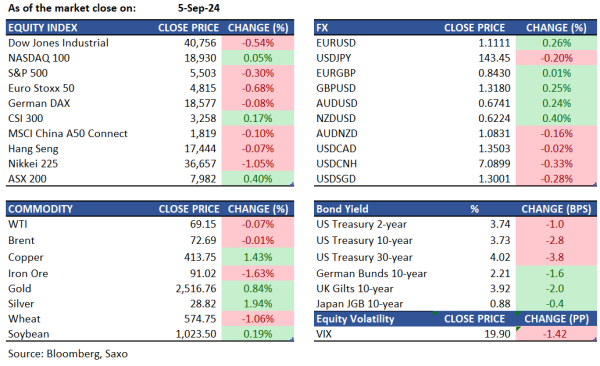

Equities: US stocks ended a volatile session mixed on Thursday as investors repositioned ahead of Friday’s crucial labor report. The S&P 500 and the Dow Jones fell by 0.3% and 0.5%, respectively, while the Nasdaq 100 managed gains after initially rising over 1%. New labor market data offered mixed signals about the U.S. economy's health with ADP private payroll growth for August coming in at 99,000 jobs, the weakest since January 2021 and significantly below expectations. However, weekly unemployment claims declined, providing some relief. The conflicting data, including a drop in job openings on Wednesday, fueled concerns about a potential recession and the pace of the Federal Reserve's rate-cuts. Health sector stocks led the declines, with Eli Lilly down 3.5% and UnitedHealth falling 1.5%. In contrast, the consumer discretionary sector performed best, bolstered by Amazon's 2.6% rise and Tesla's 4.9% increase. Following a 99% increase in revenue and impressive Q2 deliveries, Nio saw its stock surge by 14.3% in today’s session. Conversely, Broadcom, which reported earnings after the market closed and exceeded expectations on both revenue and earnings, saw its shares decline by 6.7%.

Fixed income: Treasuries peaked after ADP data missed expectations. However, gains were trimmed at the front end of the curve due to an unexpected rise in the prices paid component of the August ISM services report. This led to a flattening of the curve, partially reversing Wednesday’s steepening trend, with long-end yields ending the day richer by about 4 basis points compared to the previous day's close. Yields were richer by 1 to 4 basis points across the curve, with the 2s10s and 5s30s spreads flattening by 2 and 2.5 basis points, respectively. The 10-year yields ended around 3.725%, down approximately 3 basis points on the day, outperforming both bunds and gilts. Investors continued to pour money into US money-market funds for the fifth consecutive week, indicating strong demand despite anticipated Federal Reserve interest-rate cuts. About $37 billion was added to these funds in the week ending September 4, bringing total inflows over this period to approximately $165 billion. Buyers eagerly participated in Treasury’s four- and eight-week auctions to lock in yields above 5%, anticipating that the Federal Reserve will cut interest rates later this month. The Treasury sold $80 billion of four-week bills at 5.08% and $80 billion of eight-week bills at 5.04%.

Commodities: WTI crude futures settled at $69.1, close to a 14-month low, due to concerns over slowing demand in the U.S. and China, and potential increased supply from Libya, despite a larger-than-expected 6.9 million barrel drop in U.S. crude inventories reported by the U.S. Energy Information Administration for the week ending August 30. OPEC+ postponed planned production hikes for October and November. In Libya, tankers resumed loading crude despite political tensions. U.S. gasoline futures fell toward $1.9 per gallon in September, the lowest since February 2021, amid a broader slump in the oil market driven by reduced fuel demand. Gold prices increased by 0.65% to $2,516.

FX: The US dollar slipped further lower on Thursday amid mixed economic data continuing to put the focus on Fed’s rate cuts. However, markets still remain divided between whether the US economy will achieve a soft landing or a hard landing, the two scenarios we discussed in this article. Earlier this week, it seemed that a hard landing scenario was being priced in, but yesterday’s price action of Kiwi dollar outperforming among major currencies is reflective of soft landing expectations. Gains in other activity currencies like British pound and Australian dollar also outpaced gains in the Japanese yen, a safe-haven. The Norwegian krone, however, closed in the red as oil prices failed to sustain a bid despite OPEC+ pushing back its supply hike timeline.

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.