Hang Seng Index and ASX 200: Real Estate Woes and Mining Losses Drag Markets Down

US Equity Markets Gain as Inflation Remains in Focus

On Friday, August 30, the US equity markets had a positive end to the week, as investors monitored inflation data.

The Nasdaq Composite Index and the S&P 500 saw gains of 1.13% and 1.01%, respectively, while the Dow rose by 0.55%.

US Economic Indicators Raise Rate Cut Bets

On Friday, August 30, US economic indicators gave investors reason to cheer. Upward trends in personal income and spending indicated a robust US economy. Furthermore, softer-than-expected inflation supported bets on a 25-basis point September Fed rate cut.

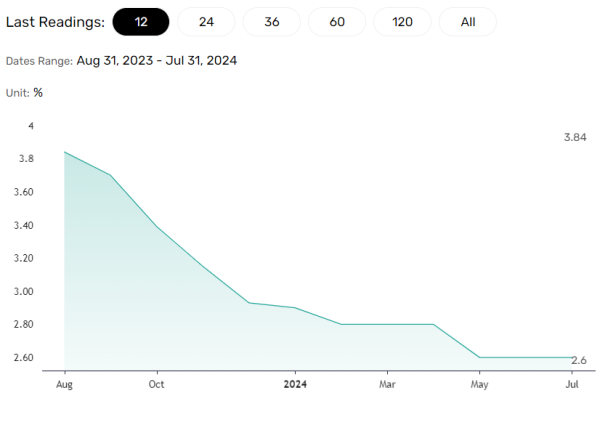

The US Core PCE Price Index increased by 2.6% year-on-year in July, after a 2.6% rise in June.

China Manufacturing PMI Brings Relief

On Monday, September 2, Manufacturing PMIs from Australia, China, and Japan drew investor interest. However, China’s Caixin Manufacturing PMI was a crucial data release amidst ongoing uncertainty about the demand environment.

The Caixin Manufacturing PMI increased from 49.8 in July to 50.4 in August.

Softer Yen Boosts Demand for Nikkei Index-listed Stocks

On Friday, August 30, the USD/JPY gained 0.79%, closing the session at 146.126, and continued to trend higher on Monday, September 2.

The softer Japanese Yen could boost buyer demand for Nikkei-listed export stocks benefitting from overseas earnings.

Early in the Monday morning session, the Jibun Bank Manufacturing PMI increased from 49.1 in July to 49.8 in August, up from a preliminary 49.5. The higher PMI may indicate an improving macroeconomic environment, possibly raising bets on a Q4 2024 Bank of Japan rate hike.

However, a dovish Fed rate path and expectations of a US soft landing remain tailwinds.

Hang Seng and Mainland China Equities Slide Amid Real Estate Concerns

The Hang Seng Index was down 1.75% on Monday morning. Real estate and tech stocks were leading the decline.

The Hang Seng Mainland Properties Index tumbled by 4.65% after New World Development Co. Ltd.’s (0017) forecast a $2.6 billion loss for the 2024 financial year. New World Development shares were down 13.25%.

The Hang Seng Tech (HSTECH) was down 1.92%, with Tencent (0700) and Alibaba (9988) losing 1.44% and 1.96%, respectively. Baidu (9888) fell by 1.33%.

The Mainland equity markets were also under pressure, with the CSI 300 and the Shanghai Composite Index falling by 1.15% and 0.56%, respectively.

Nikkei Index Bucks the Market Trend

The Nikkei Index gained 0.16% on Monday morning. Further signals of a US soft landing drove demand for the USD/JPY pair, supporting Nikkei Index-listed stocks.

Tokyo Electron Ltd. (8035) and Softbank Group Corp. (9984) were up by 0.45% and 0.55%, respectively, while Nissan Corp. (7201) advanced by 0.85%.

ASX 200 Falls as Gold and Iron Ore Prices Slide

The ASX 200 Index was down 0.20% on Monday morning, with gold and mining stocks leading the decline.

Northern Star Resources Ltd. (NST) fell by 1.64% after gold prices declined by 0.71% on Friday. Mining giants BHP Group Ltd. (BHP) and Rio Tinto Ltd. (RIO) were down 1.15% and 1.69%, respectively. Iron ore spot extended its losses from Friday, tumbling 3% on Monday, impacting demand for mining stocks.

Investors should remain alert, with central bank commentary pivotal as the US Personal Income and Outlays Report looms. Closely monitor the news wires, real-time data, and expert commentary to manage trading strategies accordingly. Stay informed with our latest news and analysis to manage positions across the Asian equity markets.