Home Depot reported results above consensus, stock falls due to lower annual forecasts

Home Depot (HD.US) lower after downgrading forecasts for 2024

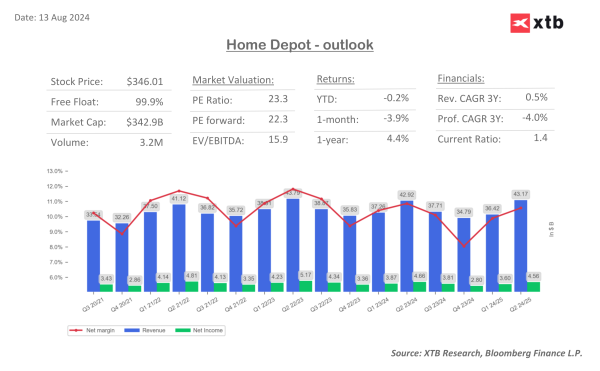

Home Depot is down 4% in pre-market trading following the release of fiscal year 2024 second-quarter results, which exceeded analyst expectations in terms of revenue and earnings. However, the company lowered its forecasts for the full fiscal year. The world's largest home improvement retailer reported a decline in comparable sales but increased revenue thanks to the acquisition of SRS Distribution.

Key financial data:

- Revenue: $43.18 billion

- Up 0.6% year-over-year from $42.92 billion in Q2 2023

- Above analyst expectations of $42.71 billion

- Adjusted earnings per share (EPS): $4.67

- Down 0.2% year-over-year from $4.68 in Q2 2023

- Above analyst expectations of $4.55

- Comparable sales: 3.3% decline

- Below analyst expectations of a 2.2% decline

Forecasts for fiscal year 2024:

- Adjusted earnings per share: 1-3% decline (previously about 1% growth)

- Revenue: 2.5-3.5% growth (previously about 1% growth)

- Comparable sales: 3-4% decline (previously 1% decline)

Key information:

- The 3.3% decline in comparable sales marks the seventh consecutive quarter of declines

- The $18 billion acquisition of SRS Distribution aims to strengthen the company's position in the professional contractor segment

- Customers are postponing larger renovation projects due to high interest rates and economic uncertainty

- The professional customer segment is performing better than the DIY (do-it-yourself) segment

Home Depot reported a decline in comparable sales, reflecting challenging market conditions. In an interview with CNBC, CFO Richard McPhail explained that since mid-2023, the company has been dealing with consumers with a "deferral mindset." High interest rates have led them to postpone buying and selling homes and taking out loans for larger projects, such as kitchen renovations.

Moreover, in the last quarter, surveys of customers and building professionals revealed a new challenge: a more cautious consumer. "Professionals tell us that for the first time, their customers aren't just deferring projects because of higher financing costs," McPhail said. "They're deferring because of a sense of greater uncertainty in the economy."

Despite these challenges, the company increased revenue thanks to the acquisition of SRS Distribution, which is set to strengthen its position in the lucrative professional contractor segment. Home Depot continues to invest in areas that can help increase long-term market share: the professional segment, supply chain, and digitalization.

Home Depot's CEO emphasized that the business fundamentals remain strong, and the company will continue to invest regardless of the outcome of the upcoming U.S. elections. The company expects that homeowners will not change their approach to home renovation and maintenance.

Recommendations: Home Depot has 43 recommendations, of which 26 are "buy" with the highest target price at $426, 13 are "hold," and 4 are "sell" with the lowest price at $270. The 12-month average stock price forecast is $376.81, implying an 8.9% upside potential compared to the current price.

Technical analysis: The stock price in pre-market trading is $337.4 and is approaching the 50% Fibonacci retracement level. Breaking through this support opens the way to retest the year's lows at $324. These will be strong resistance due to the proximity of the 61.8% Fibonacci retracement. The price is also below the 50 and 100 SMAs, and in pre-market trading, it passed through the 200 SMA. In case of a direction change, the SMAs and 38.2% Fibonacci retracement will remain as resistance. Breaking through these could open the way to test the 23.6% Fibonacci retracement. RSI is currently in a monthly downtrend, with a slight rebound to 45. MACD also indicates a more bearish approach from investors towards the company. Look for RSI to break out of the downward channel and a change in MACD to determine a clear upward direction. Otherwise, the price may continue to fall.