How high can gold and silver rally?

Key points

- Gold's rally continues, and following another brief correction it is close to reaching a sixth record this year

- As the opportunity cost of holding gold decreases, we may see increased demand for gold-backed ETFs

- A poll among LBMA delegates sees gold add 10% and silver 40% in the next year

Gold’s record-breaking rally continues, and following another shallow mid-month correction that saw buyers return ahead of USD 2,600, spot bullion has returned to trade just below the USD 2,685 record reached last month. The precious metal market has witnessed an unprecedented strong uptrend this past year, with gold and silver both trading up close to 40%, with only minor corrections seen during this extended rally—a sign of strong underlying momentum and FOMO (fear of missing out) of a rally that, at this point, shows little signs of ending.

Since hitting a cycle low last October, the gold rally, has as per the three attempted trendlines, continued to accelerate, highlighting the level of FOMO and fundamental support the metal has and continues to enjoy. In the short term, traders will be watching incoming US data to see whether support remains strong enough for the metal to reach another fresh record, the sixth this year.

The bullish drivers throughout this period are numerous, with the most important being the risk of fiscal instability, safe-haven appeal, geopolitical tensions, de-dollarization, uncertainties surrounding the US presidential election, and now also rate cuts—not just by the Fed, but by other central banks as well—reducing the cost of holding non-interest-paying investments in gold and silver. The latter potentially supports increased demand for gold-backed ETFs from underinvested asset managers, especially in the West, who, up until May, had been net sellers since the FOMC began its aggressive rate hikes in 2022.

The sustained demand for investment metals during this time has, for now, triggered a breakdown in the normal inverse correlation between gold and the dollar. The latest example is the lack of a negative reaction in gold to the 2.5% gain in the Bloomberg Dollar index since the beginning of September—a period that has seen the timing, speed, and depth of future US rate cuts pared back amid continued strength in US economic data. However, with inflation increasingly getting under control, and in some countries and regions falling back below 2%, the prospect of further rate cuts remains.LBMA delegates predict 40% upside for silver

Having already jumped by almost 40% in the past year, there is little doubt that many would-be investors balk at the prospect of paying record prices. But with the fear of missing out on the continued rally ultimately forcing many to get involved, having reached record prices, the ability to forecast the next level is increasingly down to guesswork and the round numbers game. The next major target for gold points to USD 3,000 and silver to USD 35.This week, a poll among delegates from around the world attending the London Bullion Market Association’s annual gathering predicted higher prices in a year’s time for gold, silver, platinum, and palladium. While gold is expected to climb around 10% to USD 2,917.40 an ounce by late October next year, delegates held a very strong view on silver, seeing it gain more than 40% to reach USD 45 an ounce, with experts noting that industrial demand continues to drive market deficits as mine supply struggles to keep pace.

Delegates also saw a strong 12 months ahead for platinum, predicting the price could reach USD 1,147.90 an ounce, a level not seen since the first half of 2023. The white metal trades historically cheap to gold, with the current ratio of 2.7 only expected to decline to 2.61 based on the above price assumptions. Like silver, analysts expect platinum prices will benefit from growing industrial demand, primarily from the renewable energy industry, and a deepening supply deficit next year.

Investor flows in ETFs and futures

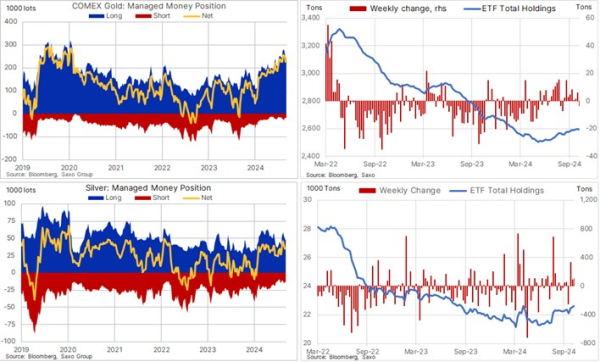

Bullion-backed holdings in exchange-traded funds peaked at a record 3,453 tons in October 2020 after governments and central banks fought the global pandemic with stimulus and rate cuts, thereby raising the risk of inflation. However, while the global economy recovered, the inflation threat only picked up pace the following year. Following a brief spike in gold demand after the Russian invasion of Ukraine in 2022, the beginning of an aggressive US rate hike cycle saw investors flee ETFs as funding costs rose. By May this year, total holdings had slumped to 2,500 tons before the prospect of rate cuts and a continued rally helped stabilise demand.Around the time of last year’s October low, momentum-chasing hedge funds held a small net short position in COMEX gold futures, and the subsequent rally helped trigger a strong buying response, culminating last month when the net long reached a 4.5-year high at 255,000 contracts, or 25.5 million ounces. The recent correction attempt to near USD 2,600 drove a two-week period of net selling to 226,000 contracts. But with the bulk of the current net long having been established back in February/March at much lower prices, selling pressure from speculators remains relatively weak.

Silver, which depends on industrial and investment demand, has seen similar trends, with ETF holdings bottoming out during the first quarter before staging a relatively muted recovery as prices struggled to reach fresh cycle highs. Hedge fund activity, meanwhile, remains much more volatile compared with the flows seen in gold, with the net long recently seeing a two-week reduction of 25%, leaving the net long at 35,000 contracts—not far above the 26,000 average seen so far this year, highlighting a market that needs a technical signal to attract fresh demand from momentum-focused funds.

Recent commodity articles:

8 Oct 2024: Podcast: Navigating market shifts: Fed rate cuts, commodities and rising food prices

8 Oct 2024: Video: These commodities might be impacted by the US election

7 Oct 2024: Crude oil surge caps strong four-week rally for commodities

7 Oct 2024: COT: Broad buying momentum persists, led by Brent, copper and grains

2 Oct 2024: Q3 2024 Commodity Outlook: Gold and silver continue to shine bright

30 Sept 2024: COT: Fed and PBOC trigger largest weeklyl surge in commodities demand in a decade

27 Sept 2024: Commodity weekly: Industrial metals gain strength during a week of crude weakness

26 Sept 2024: Crude prices drop again as Saudi and Libya supply concerns grow

24 Sept 2024: Fed and PBOC add momentum to commodities market rebound

23 Sept 2024: COT: Dollar short reduced; Investment metals see strong demand ahead of FOMC

20 Sept 2024: Commodity weekly: Commodities boosted by bumper rate cut

20 Sept 2024 Video: Gold or silver, which metal will perform the best

17 Sept 2024: With gold reaching new heights, silver shows potential

16 Sept 2024: COT: Record short Brent and gas oil positions add upside risks to energy

11 Sept 2024: Crude slumps amid technical selling and recession fears

10 Sept 2024: US Election: will gold win in all scenarios

9 Sept 2024: COT: Crude long cut to 12-year low; Dollar short more than doubling

5 Sept 2024: Can gold overcome the 'September curse'?

4 Sept 2024: Wheat rises on European crop worries

3 Sept 2024: Chinese economic woes drag down crude oil and copper

2 Sept 2024: COT: Commodities see broad demand as the USD slumps to a net short