Limited short-selling interest observed during copper’s recent aggressive correction

Key points

- Copper has now slumped 20% from the May records with rising stockpiles disrupting an otherwise positive long-term outlook

- Total stocks at exchange monitored warehouses have risen to levels not seen since the dept of the pandemic crisis

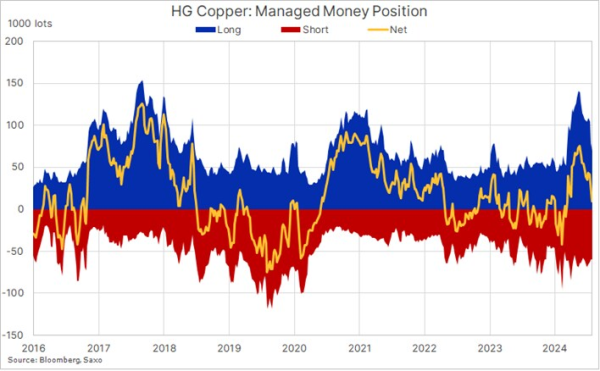

- No naked short selling interest has been observed from hedge funds during a recent 87% reduction in the High Grade net long

- Key support near USD 3.85 with the 200-day moving average potentially offering some resistance

Since reaching a record high at USD 5.2 per pound in late May, the High Grade copper contract has slumped 20%, with the bulk of the decline seen during the past month when the demand outlook in China continued to deteriorate, and US data increasingly began pointing to a slowdown. The premature surge to record highs back in May was driven by momentum-chasing speculators in the London and New York futures markets, as well as investors jumping on the green-transformation and AI-focused themes, only to see the rally run out of steam once the market realised that these potential long-term supporting factors were being overridden by a deterioration in the short-term outlook amid rapidly rising stock levels, first in China and now recently abroad as well, after an arbitrage window opened to make it attractive for Chinese owners of copper to export unwanted stock abroad.

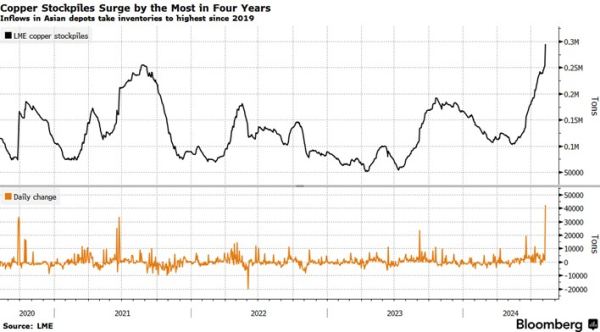

Copper’s current stockpile problem

The second quarter in China tends to represent a period where industrial activity picks up following winter and the Lunar holiday period, but so far this year, this pick-up, which tends to bring down built supplies of key raw materials, has not occurred. Instead, we have seen inventories monitored by the major futures exchanges continuing to rise at a rapid pace, signalling a period of a major supply/demand mismatch, primarily due to weak demand.

Total stocks at warehouses monitored by the exchanges in London and Shanghai have risen to levels not seen since the depth of the pandemic back in early 2020. Following an initial rise in Shanghai, where the overhang was felt the hardest, material has started to flow into LME warehouses in South Korea and Taiwan, culminating this week when the LME reported a 42k ton inflow, the biggest since 2019, bringing total LME monitored stocks near 300k tons, further unnerving the remaining bulls. In addition, Monday’s deleveraging-led mini-crash and volatility spike did nothing to support the current sentiment, which at best points to a period of consolidation while fundamentals eventually improve.

Limited short-selling seen despite prolonged price weakness

Turning to the behaviour among speculators such as hedge funds and CTAs, we discover that since seeing the speculative net long reach a 40-month high on 21 May at 75.3k contracts, the mentioned 20% correction that followed has seen that long collapse by 87% to just 9.4k contracts. However, if we look a bit closer, we find that the reduction has almost exclusively been driven by long liquidation, and not fresh short selling. In other words, despite the deteriorating technical and short-term fundamental outlook, these traders have so far been mostly focusing on bringing down their exposure, and not looking for even lower prices through actively selling themselves short in the market.

With that in mind, we see the prospect for a relatively strong recovery once the technical and fundamental outlook improves. Overall, our long-term belief in higher prices remains, supported by a stabilising China, the US avoiding a recession, an ongoing rise in demand towards electrification, and increasingly tight supply amid lack of new discoveries. In the short-term, the market remains challenged by the risk of further unwinding of yen carry trades, a continued rise in stocks, as well as the (limited) risk of a US recession.

Five consecutive weeks of selling has seen the HG copper contract return to trade around USD 4 per pound, and from a technical perspective, the chart points to support near USD 3.85 per pound, the trendline from the 2020 low, as well as a return to the consolidation area that existed for several months before the eventual move higher earlier this year. The first sign of stabilizing would probably require a move back above the 200-day moving average, currently at USD 4.11 followed by the recent high at USD 4.2235.

Recent commodity articles:

6 Aug 2024: Video: What factors are fueling the current market turmoil and gold's response

5 Aug 2024: COT: Broad commodities sell-off gains momentum; Forex traders seek JPY and CHF

5 Aug 2024: Commodities: Position reduction in focus as volatility spikes

2 Aug 2024: Widespread commodities decline in July, with gold as the notable exception

31 July 2024: Crude's month-long slide halted by fresh Mideast worries

30 July 2024: Record demand explains gold's current resilience

29 July 2024: COT: Energy and metals selling cuts hedge fund long to four-month low

4 July 2024: Sluggish US economic indicators boost demand for gold and silver

4 July 2024: Podcast Special: Quarterly Outlook - Sandcastle Economics

2 July 2024: Quarterly Outlook - Energy and grains in focus as metals pause

1 July 2024: COT: Crude long builds ahead of Q3 while grains selling accelerates

28 June 2024: Metals and natural gas propel commodity sector to quarterly gain

26 June 2024: Crude seeks support from seasonal demand strength

24 June 2024: Copper's resilience despite China weakness

18 June 2024: Precious metals go through prolonger period of consolidation

17 June 2024: COT: Dollar long jumps; Funds start rebuilding crude long

14 June 2024: Commodity weekly: Energy sector gains counterbalance metal consolidation

13 June 2024: Oil prices steady amid divergent OPEC and IEA demand projections

10 June 2024: COT: Brent long cut to ten-year low; metals left exposed to end of week slump

3 June 2024: COT: Crude length added before OPEC+ meeting; gold and copper see profit-taking