Market Analysis: USD Strengthens Amid Political Developments; GBP Pressured by Softening Inflation

The US Dollar Index (DXY) has extended its gains, decisively breaking above the 100-day Simple Moving Average (SMA) at 103.20—a key technical resistance level. This move signifies strong bullish momentum, with the next targets at 103.50 and 104.00. The key currency pair that makes contribution to the DXY upside trend, EURUSD, broke below 1.09 channel, however market reaction on this event was muted, suggesting further downside is in cards with main selling target at 1.0850 level:

The catalyst behind this surge is multifaceted. Former President Donald Trump's recent appearance on Bloomberg Television has injected a new dynamic into the currency markets. His outlined plans on trade, taxes, and Federal Reserve policies have led traders to price in a higher probability of a Republican victory in the November 5 presidential election. Markets perceive Trump's policies as USD-supportive, particularly his stance on trade and potential fiscal stimulus. With a light US economic calendar and no Federal Reserve officials scheduled to speak, the market's focus shifts to political developments and upcoming central bank meetings. Interest rate futures indicate a 94% probability of a 25 bp rate cut at the November 7 FOMC meeting, with only a 6% chance of rates remaining unchanged. The possibility of a 50 bp cut has been fully discounted.

The high probability of a rate cut suggests the Fed is proactively addressing potential economic headwinds. However, with a rate cut largely priced in, the impact on the USD may be muted unless accompanied by dovish forward guidance.

The US 10-year Treasury yield is trading at 4.00%, slightly below last week's high of 4.11%. The modest softening in yields suggests that bond markets are adjusting to the anticipated rate cut, and the USD strength reflects capital flows seeking higher returns amid global uncertainty.

Suffering substantial losses, European stocks are weighed down by regional economic concerns and caution ahead of the ECB meeting. The lack of significant catalysts has led to profit-taking and repositioning among investors.

Indicating a positive opening, US equity futures are buoyed by the strengthening USD and optimism surrounding potential fiscal policies under a Trump administration. The anticipation of a Fed rate cut also supports equity valuations by lowering the discount rate for future earnings.

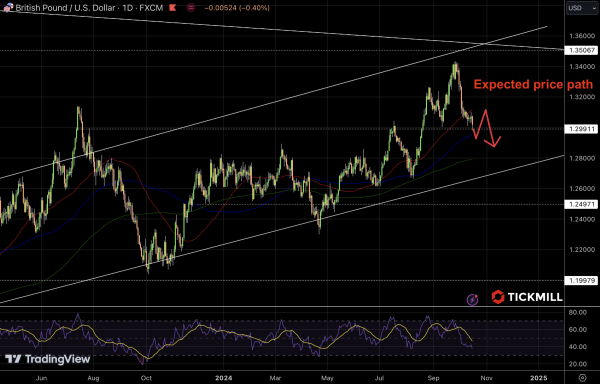

The Pound Sterling faces significant pressure following the release of the UK's Consumer Price Index data for September:

Annual CPI softened to 1.7%, below expectations of 1.9% and down from 2.2% in August. The month-on-month figure remained flat, indicating stagnation in price growth. Excluding volatile items, core CPI decelerated to 3.2% from 3.6%, undershooting forecasts of 3.4%. This suggests that underlying inflationary pressures are easing more rapidly than anticipated.

A key metric for the Bank of England, services inflation slowed to 4.9% from 5.6%. The deceleration aligns with recent data showing a slowdown in wage growth—Average Earnings Excluding Bonuses rose by 4.9%, the slowest in two years.

The soft inflation data increases the likelihood of a 25 basis point rate cut in one of the two remaining policy meetings this year. Market participants are adjusting their positions accordingly, which is reflected in the GBP's depreciation.