Stocks suffer as chances of a summer Fed rate cut decrease

Extra focus on today’s US data releases and Fed speakers

Euro shows resilience while gold defies gravity

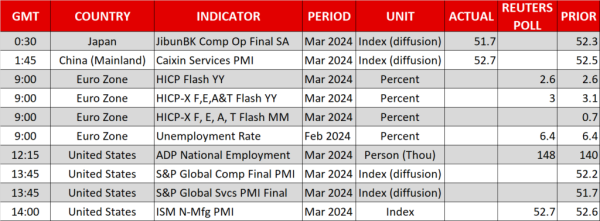

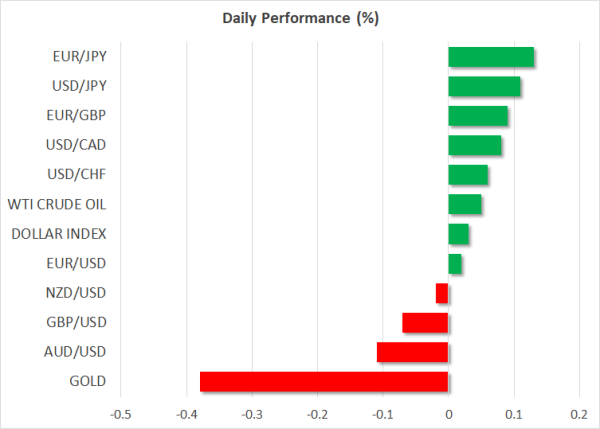

Stocks suffer as the US economic outlook remains brightRecent US data releases, and in particular Monday's ISM Manufacturing survey, appear to have caused quite a market stir. Equities fell during Tuesday’s session with the S&P500 index enjoying its weakest day since early March on the back of growing expectations that the few Fed rate cuts priced in might be even more delayed.While the diminishing Fed expectations are driven by a stronger US economy, which on face value means a brighter outlook for most firms in terms of stronger earnings, the market’s current mindset is that stocks need lower interest rates. This is not entirely odd as the technology firms driving the AI frenzy need significant funding.In the meantime, yields are rising and essentially increasing the borrowing costs faced by most firms. This means even tighter financial conditions, potentially causing discomfort in the Fed corridors. Yesterday, the mostly hawkish-leaning Fed members, Mester and Daly, stated that three rate cuts this year are reasonable. These comments were a touch more dovish than previously, which could be an early indication of a change in the Fed council's tune.Later today we will get a plethora of Fed speakers as no fewer than six members will be on the wires, including Chairman Powell at 16.10 GMT time, potentially offering early commentary on the ADP employment report and the ISM Services survey figures published today.Extra focus on today’s US data releasesAt 12.15 GMT the ADP employment report is expected to show a 148k increase, a tad higher than February’s figure of 140k. More importantly, the ISM Services survey is seen edging to 52.7 with the market focusing on the prices paid subindex. Should this indicator jump higher, confirming the presence of decent inflationary pressures, the equity markets could remain in the red again today.Euro shows resilienceThe euro managed to climb higher against the dollar despite the evident divergence in economic growth indicators and yesterday’s preliminary German inflation report for March printing a bit lower than the forecast. Today, the crucial euro area aggregate CPI will be released. Confirmation of current market expectations is unlikely to upset the market but, following the German figures, there is a sizeable risk for downside surprises in both the headline and core indicators.Gold defies gravityGold continues to defy gravity as it recorded a new all-time earlier today. It is showing unprecedented strength and manages to rally under every market scenario. The lower dollar could have been a factor in yesterday's move, but gold has rallied even in dollar-positive days. This is another indication that other forces are in play such as strong buying appetite from certain sovereigns trying to diversify their dollar holdings.Bitcoin mimics stocks; Oil hits new 5-month highBitcoin’s volatility remains high as the king of crypto enjoyed another strong red session, essentially following equities lower. Notwithstanding the wider economic developments, this year’s big event, the bitcoin halving, is getting more attention, potentially impacting bitcoin’s performance until April 20.Finally, there is an OPEC-JMMC online meeting taking place today. While this usually serves as a monitoring meeting, we could get comments regarding the current rally in oil prices. WTI reached a new 5-month yesterday, adding another headache to the various central banks looking for their first rate cut.

Stocks suffer as the US economic outlook remains brightRecent US data releases, and in particular Monday's ISM Manufacturing survey, appear to have caused quite a market stir. Equities fell during Tuesday’s session with the S&P500 index enjoying its weakest day since early March on the back of growing expectations that the few Fed rate cuts priced in might be even more delayed.While the diminishing Fed expectations are driven by a stronger US economy, which on face value means a brighter outlook for most firms in terms of stronger earnings, the market’s current mindset is that stocks need lower interest rates. This is not entirely odd as the technology firms driving the AI frenzy need significant funding.In the meantime, yields are rising and essentially increasing the borrowing costs faced by most firms. This means even tighter financial conditions, potentially causing discomfort in the Fed corridors. Yesterday, the mostly hawkish-leaning Fed members, Mester and Daly, stated that three rate cuts this year are reasonable. These comments were a touch more dovish than previously, which could be an early indication of a change in the Fed council's tune.Later today we will get a plethora of Fed speakers as no fewer than six members will be on the wires, including Chairman Powell at 16.10 GMT time, potentially offering early commentary on the ADP employment report and the ISM Services survey figures published today.Extra focus on today’s US data releasesAt 12.15 GMT the ADP employment report is expected to show a 148k increase, a tad higher than February’s figure of 140k. More importantly, the ISM Services survey is seen edging to 52.7 with the market focusing on the prices paid subindex. Should this indicator jump higher, confirming the presence of decent inflationary pressures, the equity markets could remain in the red again today.Euro shows resilienceThe euro managed to climb higher against the dollar despite the evident divergence in economic growth indicators and yesterday’s preliminary German inflation report for March printing a bit lower than the forecast. Today, the crucial euro area aggregate CPI will be released. Confirmation of current market expectations is unlikely to upset the market but, following the German figures, there is a sizeable risk for downside surprises in both the headline and core indicators.Gold defies gravityGold continues to defy gravity as it recorded a new all-time earlier today. It is showing unprecedented strength and manages to rally under every market scenario. The lower dollar could have been a factor in yesterday's move, but gold has rallied even in dollar-positive days. This is another indication that other forces are in play such as strong buying appetite from certain sovereigns trying to diversify their dollar holdings.Bitcoin mimics stocks; Oil hits new 5-month highBitcoin’s volatility remains high as the king of crypto enjoyed another strong red session, essentially following equities lower. Notwithstanding the wider economic developments, this year’s big event, the bitcoin halving, is getting more attention, potentially impacting bitcoin’s performance until April 20.Finally, there is an OPEC-JMMC online meeting taking place today. While this usually serves as a monitoring meeting, we could get comments regarding the current rally in oil prices. WTI reached a new 5-month yesterday, adding another headache to the various central banks looking for their first rate cut.

Stocks suffer as the US economic outlook remains brightRecent US data releases, and in particular Monday's ISM Manufacturing survey, appear to have caused quite a market stir. Equities fell during Tuesday’s session with the S&P500 index enjoying its weakest day since early March on the back of growing expectations that the few Fed rate cuts priced in might be even more delayed.While the diminishing Fed expectations are driven by a stronger US economy, which on face value means a brighter outlook for most firms in terms of stronger earnings, the market’s current mindset is that stocks need lower interest rates. This is not entirely odd as the technology firms driving the AI frenzy need significant funding.In the meantime, yields are rising and essentially increasing the borrowing costs faced by most firms. This means even tighter financial conditions, potentially causing discomfort in the Fed corridors. Yesterday, the mostly hawkish-leaning Fed members, Mester and Daly, stated that three rate cuts this year are reasonable. These comments were a touch more dovish than previously, which could be an early indication of a change in the Fed council's tune.Later today we will get a plethora of Fed speakers as no fewer than six members will be on the wires, including Chairman Powell at 16.10 GMT time, potentially offering early commentary on the ADP employment report and the ISM Services survey figures published today.Extra focus on today’s US data releasesAt 12.15 GMT the ADP employment report is expected to show a 148k increase, a tad higher than February’s figure of 140k. More importantly, the ISM Services survey is seen edging to 52.7 with the market focusing on the prices paid subindex. Should this indicator jump higher, confirming the presence of decent inflationary pressures, the equity markets could remain in the red again today.Euro shows resilienceThe euro managed to climb higher against the dollar despite the evident divergence in economic growth indicators and yesterday’s preliminary German inflation report for March printing a bit lower than the forecast. Today, the crucial euro area aggregate CPI will be released. Confirmation of current market expectations is unlikely to upset the market but, following the German figures, there is a sizeable risk for downside surprises in both the headline and core indicators.Gold defies gravityGold continues to defy gravity as it recorded a new all-time earlier today. It is showing unprecedented strength and manages to rally under every market scenario. The lower dollar could have been a factor in yesterday's move, but gold has rallied even in dollar-positive days. This is another indication that other forces are in play such as strong buying appetite from certain sovereigns trying to diversify their dollar holdings.Bitcoin mimics stocks; Oil hits new 5-month highBitcoin’s volatility remains high as the king of crypto enjoyed another strong red session, essentially following equities lower. Notwithstanding the wider economic developments, this year’s big event, the bitcoin halving, is getting more attention, potentially impacting bitcoin’s performance until April 20.Finally, there is an OPEC-JMMC online meeting taking place today. While this usually serves as a monitoring meeting, we could get comments regarding the current rally in oil prices. WTI reached a new 5-month yesterday, adding another headache to the various central banks looking for their first rate cut.