Markets Weekly Outlook – US Elections and Central Banks Lead the Way

- Global markets experienced a mixed week, influenced by geopolitical risks and US jobs data revisions.

- The week ahead focuses on China’s Standing Committee meeting, the US election and Central Bank Meetings.

- Wall Street indexes struggled, potentially due to high valuations and AI capital spend.

Read More: GBP/USD Technical: Trendline Break Sets the Stage for Further Downside

Week in Review: US Jobs Revised Downward After Positive GDP

A mixed week comes to a close as markets deal with renewed geopolitical risks and another downgrade to jobs numbers by the US Bureau Labor of statistics. US Earnings was another area that both surprised and disappointed as Wall Street fret about growing AI capital expenditure.

Six of the ‘Magnificent 7’ companies have already reported with revenue and profit beats but rising capital expenditure around AI continues to weigh on the minds of market participants. Amazon however soared on Friday as it shook off the blues of the Q2 earnings report and on course to post its best day since February, up around 6.5%. This helped Wall Street Indexes rise on Friday after the US open. Apple disappointed markets but the stock price held firm with the technology company down 0.5% on the day.

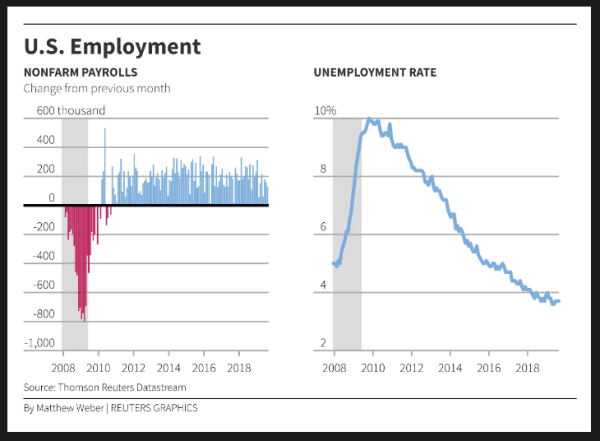

The NFP report did not paint a pretty picture as markets digested another significant downward revision to the previous two months data. The last two job reports were revised lower by a combined 112k jobs with the August report revised down by 81k and the September number by 31000. This has given the Fed more room on the rate cut front just as market participants were eyeing the possibility of less rate cuts moving forward.

Source: LSEG (click to enlarge)

When it comes to performance, the US Dollar Index saw four days of declines this week before a resurgence on Friday. This came as a surprise as market participants were pricing in more aggressive rate cuts which in theory should have led to further USD weakness. Are we seeing the US Dollars safe haven appeal returning?

Commodities saw Oil trickle higher for the majority of the week but finding hurdles consistently. Brent has been unable to close the gap it left over the weekend, but is still up around 2.5% for the week. Gold reached fresh highs before suffering a $60 drop on Thursday before steadying slightly on a Friday. Given the rising risks and geopolitics at play, it would take a brave person to hold onto gold shorts at present.

Wall Street Indexes have all struggled this week and are on course to finish in the red. The sky high company and index valuations may also be off putting to market participants. Will US Indexes be able to stage a recovery in US Election and FOMC week?

The Week Ahead: China’s Standing Committee Meeting, US Election and Central Bank Meetings

Asia Pacific Markets

The week ahead in Asia will see focus pivot back to China, while rising tensions with North Korea need to be monitored as well.

In China, next week will be the meeting of China’s Standing Committee of the National People’s Congress, which will take place between 4-8 November. Markets are paying close attention to see if there will be changes to budget targets or details about new bonds. This would help understand the size of future financial plans. The slow start of this financial boost has lessened some of the initial excitement after monetary policy changes in September, but a big new financial package could bring back that enthusiasm.

Next week is relatively quiet for data releases. Trade data is expected on Thursday, where we anticipate export growth to slightly increase to about 5% year-on-year. However, we expect import growth to drop to -5.0% year-on-year after staying close to zero in the previous months.

Japan has just come off a busy week with next week expected to be much more subdued. Labor cash earnings will be a key release to watch as wage growth has been a key for the BoJ in its policy normalization efforts. Therefore a significant uptick here could add some strength to the struggling JPY.

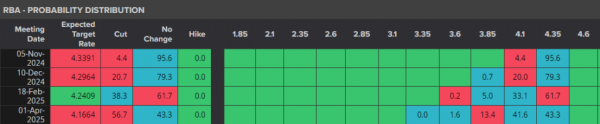

The RBA are holding their interest rate meeting next week and this follows on from the inflation data this week. Inflation came in much better than expected, now at its lowest level since Q1 2021 with a print of 2.8%.

Markets appear convinced that despite the drop in inflation the RBA will keep rates on hold. Markets are pricing in around a 95.6% chance that the RBA keep rate on hold. Will we get a surprise?

Source: LSEG (click to enlarge)

Europe + UK + US

In developed markets, the European Union is enjoying a slight respite with the major data release being retail sales. There are also two speeches from ECB President Christine Lagarde, which after the recent bout of data may provide some insight into ECB policy moving forward.

The UK is set for another busy week after the Autumn Budget was released this week. A mixed bag and reaction to the budget heading into the BoE meeting leaves the British Pound in an intriguing position against many of its counterparts.

According to LSEG data, markets are pricing in around an 84% probability of a 25 bps cut next week which could send the British Pound lower.

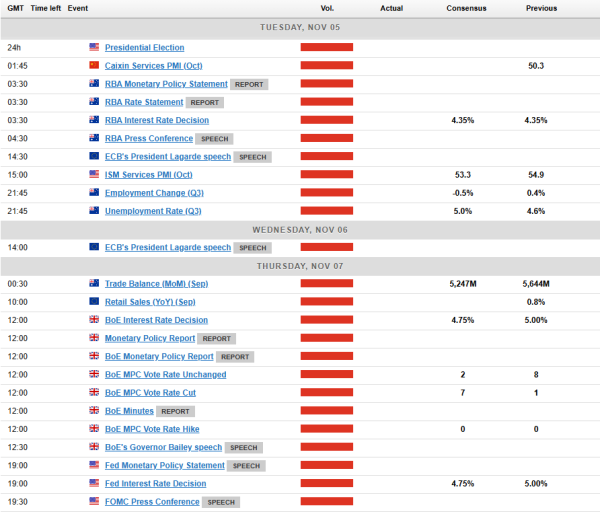

The biggest events next week however are from the United States. The US Election is on Tuesday with the FOMC meeting following the very next day. The jobs data downgrades on Friday have really cemented rate cuts from the Fed at both the November and most likely December meetings.

The US Election is the one with the most uncertainty as polling has thrown up extremely mixed numbers. Betting websites have Donald Trump as the front runner, while a Reuters/Ipsos poll and a few others have Kamala Harris in the lead. The question is who prevails and what will the impact be? A trump win could help benefit Gold prices as market participants may use it as a hedge against the pending uncertainties.

Besides Gold we could see some wild swing in US Dollar pairs, Wall Street Indexes and potentially a knock on effect for markets as a whole as risk sentiment sways back and forth.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar.

Chart of the Week

This week’s focus is back to Gold, following fresh highs and a significant pullback in what was a very choppy week.

There are of course factors supporting further increases in the Gold prices as global uncertainties continue to rack up.

Having made its run toward $2800 an ounce and falling short, this may see gold bulls make one final attempt at a test or breach of the $2800 handle.

A move higher from here will bring 2750 back on the table for the 2775 price level becomes an area of focus.

Conversely a move lower from here needs to break the 2724 handle before the 2714 and 2700 come into focus.

The RSI on the daily has finally left overbought territory which could be a sign of a shift in momentum. However, at present i would say, keep a close eye on geopolitical developments as this could have a major impact on markets over the weekend.

Gold (XAU/USD) Daily Chart – November 1, 2024

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 2724

- 2714

- 2700

Resistance

- 2775

- 2790

- 2800

Follow Zain on Twitter/X for Additional Market News and Insights @zvawda

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at [email protected]. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.