Nikkei 225 Climbs on Yen Movements as ASX 200 Eases from New Intraday High

US Equity Markets End Relatively Flat

On Tuesday, September 17, the US equity markets had another mixed session as the Fed interest rate decision loomed. The Dow dipped by 0.04%, while the Nasdaq Composite Index and the S&P 500 saw gains of 0.20% and 0.03%, respectively.

The US indices retreated from session highs as investors took profits ahead of the FOMC interest rate decision.

US Retail Sales Unexpectedly Rise

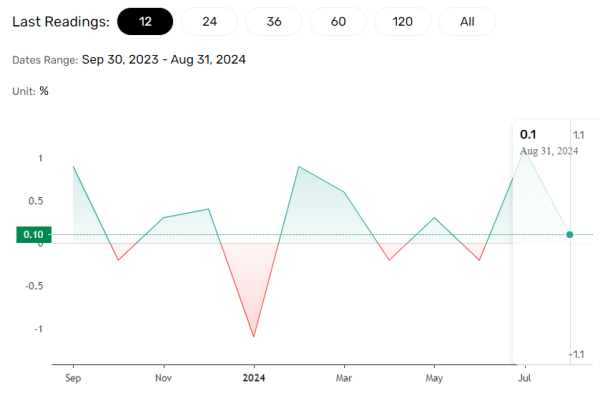

US retail sales increased by 0.1% in August after surging by 1.1% in July. The uptrend in retail sales signaled a resilient US economy as it accounts for over 60% of the US GDP. Economists had expected retail sales to drop by 0.2% in August.

Other stats included US industrial production and housing market data, all exceeding expectations.

Despite upbeat economic indicators, the CME FedWatch Tool continued to signal a 50-basis point Fed cut. On Tuesday, September 17, the chances of a 50-basis point Fed rate cut increased to 65.0%, up from 62.0% the previous day.

Signs of a resilient US economy and bets on a 50-basis point September Fed rate cut set the stage for a positive Wednesday Asian session.

Japan’s Economy in Focus as the BoJ Decision Looms

On Wednesday, economic data from Japan drew investor interest. Year-on-year, exports increased 5.6% in August, down from 10.2% in July. Imports saw a similar trend, rising 2.3% in August compared with 16.6% in July.

The import and export numbers signaled weakening demand but failed to dampen Yen demand. On Wednesday morning, the USD/JPY was down 0.68% to 141.428 as investors looked ahead to the Fed interest rate decision.

Mainland China Markets Have a Mixed Open

The mainland China markets reopened on Wednesday, with investor caution evident ahead of the Fed decision. The CSI 300 advanced by 0.07%, while the Shanghai Composite was down 0.07%.

The Hong Kong markets were closed for the post-Autumn Festival holiday.

Nikkei Index Advances on USD/JPY Trends

On Wednesday, the Nikkei Index was 0.71%. The USD/JPY rallied 1.27% on Tuesday before Wednesday’s pullback. Nevertheless, the USD/JPY enjoyed net gains, driving buyer demand for Nikkei-listed export stocks.

Fast Retailing Co. Ltd. (9983) rallied 2.43%, while Nissan Motor Corp. (7201) advanced by 1.57%. Tokyo Electron (8035) and Softbank Group Corp. (9984) saw gains of 0.18% and 0.91%, respectively.

ASX 200 Climbs a New High

The ASX 200 Index was up 0.01% on Wednesday morning, easing back from a new intraday high of 8,154. Oil and banking stocks offset declines in gold and tech stocks.

Woodside Energy Group Ltd. advanced by 0.33% following overnight oil price gains. National Australia Bank (NAB) and Westpac Banking Corp. (WBC) saw gains of 0.91% and 0.32%, respectively. Australian banks are known for high dividend yields, drawing interest from yield-seeking investors as the Fed interest rate decision loomed.

With the focus on the Fed, investors should remain alert and closely monitor news wires, real-time data, and expert commentary to adjust trading strategies accordingly. Stay informed with our latest news and analysis to manage positions across the Asian equity markets.