👀 Peloton shares are down 2,6% premarket after impressive 35% gain yesterday

Peloton's shares are experiencing a 2,6% decline in premarket trading, following an impressive 35% surge yesterday. This comes after the company reported better-than-expected Q4 results and provided a strong profit outlook for FY2025, showcasing progress in its turnaround efforts.

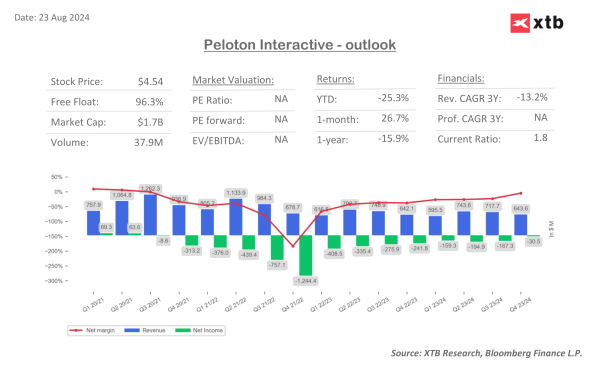

Key financial data:

- Revenue: $643.6 million in Q4, up 0.2% year-over-year (estimate: $630.1 million)

- Adjusted EBITDA: $70.3 million in Q4, compared to a loss of $34.7 million a year ago (estimate: $53.2 million)

- Connected fitness subscribers: 2.98 million, down 0.5% year-over-year (estimate: 3.02 million)

- Paid digital subscribers: 615,000, down 26% year-over-year (estimate: 606,687)

Segment results:

- Connected fitness revenue: $212.1 million, down 3.8% year-over-year (estimate: $197.3 million)

- Subscription revenue: $431.4 million, up 2.3% year-over-year (estimate: $431.2 million)

Key streaming information:

- Connected fitness subscribers: 2.98 million (down 0.5% year-over-year)

- Paid digital subscribers: 615,000 (down 26% year-over-year)

- Secondary market delivered 16% year-over-year growth in paid connected fitness subscriber additions in Q4

The fitness company's Q4 revenue slightly increased by 0.2% year-over-year to $643.6 million, with subscription revenue growing 2.3%. However, connected fitness revenue saw a 3.8% decline, reflecting ongoing challenges in hardware sales.

The fitness company's Q4 revenue slightly increased by 0.2% year-over-year to $643.6 million, with subscription revenue growing 2.3%. However, connected fitness revenue saw a 3.8% decline, reflecting ongoing challenges in hardware sales.

Peloton's focus on profitability is evident in its Q4 adjusted EBITDA of $70.3 million, a significant improvement from the $34.7 million loss in the same period last year. The company expects to achieve $200 million in annualized cost savings in fiscal 2025 through its restructuring program and more efficient media spend.

Despite these positive developments, Peloton faces headwinds in subscriber growth. Connected fitness subscribers decreased by 0.5% year-over-year, while paid digital subscribers saw a sharp 26% decline. However, the company is seeing some success in the secondary market, which delivered a 16% year-over-year increase in paid connected fitness subscriber additions in Q4.

Looking ahead, Peloton's FY2025 revenue forecast of $2.4 billion to $2.5 billion is softer than expected, factoring in year-over-year declines in hardware sales, macro headwinds, and reduced marketing spend. However, the company's adjusted EBITDA guidance of $200 million to $250 million for FY2025 significantly exceeds analyst estimates, highlighting its commitment to improving profitability.

The mixed outlook has led to divergent analyst opinions. JPMorgan downgraded Peloton to Neutral from Overweight, citing limited visibility and challenges in returning to growth in Connected Fitness subscribers and revenue. The downgrade also follows the stock's significant rally, with JPMorgan setting a new price target of $5, down from $7. However, other analysts have revised their price targets upwards: Morgan Stanley raised their target to $3.50 from $2.50, Canaccord increased theirs to $5 from $4, and Citi lifted their target to $4.75 from $4. These revisions reflect the varying interpretations of Peloton's recent performance and future prospects among Wall Street analysts.

In conclusion, while Peloton's profitability improvements are encouraging, the company still faces significant challenges in reigniting subscriber and revenue growth. The market's reaction suggests a cautious outlook as investors weigh the company's progress against ongoing industry headwinds and macroeconomic pressures.

Recommendations: Peloton has 23 recommendations, of which 2 are "buy" with the highest target price at $20, 18 are "hold", and 3 are "sell" around $2. The 12-month average stock price forecast is $4.52, implying almost no upside potential compared to the current price.

Technical analysis: The stock price broke through two resistance levels during yesterday's session and is currently at the beginning of a channel that was a significant resistance at the start of the year. During this session, support will be provided by the previous day's resistance levels, with the first remaining at the 38.2% Fibonacci retracement at $4.43 and then the 200 SMA at $4.35. Breaking through these could result in a return to the 23.6% Fibonacci retracement or even touching the 100 and 50-day SMAs. Resistance remains at the consolidation level between $4.7 and $4.94, with stronger resistance at the 50% Fibonacci retracement at $4.96 per share. Breaking through these levels opens the way to this year's highs. RSI remains temporarily overbought, which may signal a slight price correction. However, it's important to observe the MACD, which at the moment is not sending overbought signals and is still below this year's maximum.