PepsiCo with profitability decline in 3Q24 📊

PepsiCo (PEP.US) is slightly gaining today following the release of its 3Q24 results. The company's results were mostly in line with expectations, but it slightly lowered its revenue guidance due to the recall of some products in its Quaker Food segment and boycotts of the company's products in the Middle East.

Today's reaction to the results remains moderate, particularly when compared to the last release of financial results, when the stock fell more than 2% at the opening to finish on a positive note. Source: xStation

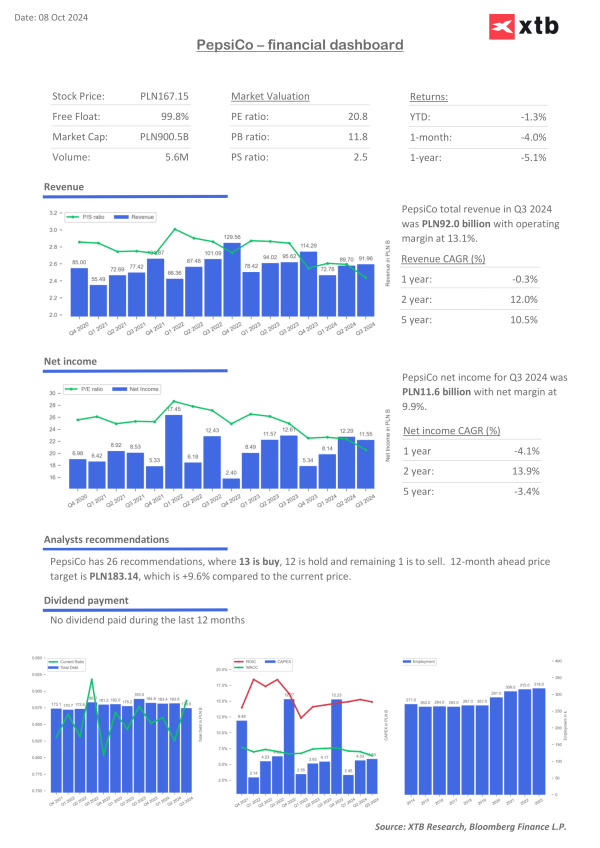

The company's net revenue in 3Q24 remain at a similar level to the previous year (-0.6% year-on-year), due to an environment of higher interest rates still limiting consumers' purchasing power, as well as consumers operating for a long time in an inflationary environment. This macroeconomic situation is taking its toll on consumer habits in connection with non-core purchases, which include the company's snacks and beverages.

More strongly than in the revenue dynamics, this situation is reflected in declining sales volumes, which affected virtually every segment (with the exception of sales in Europe and Asia-Pacific, where sales volumes increased by 1% y/y in both cases). Hardest hit by the decline was the Quaker Foods segment in North America, where volumes (as well as revenues) fell by -13% y/y. Such a strong decline is the effect of the recall of certain products, which the company had already announced.

The company also faces a deepening increase in costs, which caused operating profit to fall to $3.87 billion ( -4% y/y). This, coupled with an increase in financial expenses, caused diluted earnings per share to fall to $2.13 (vs. $2.24 a year earlier). At the profitability level, the company disappointed relative to consensus forecasts for diluted earnings per share of $2.28.

Financial results for 3Q24:

- Core EPS $2.31 vs. $2.25 y/y, estimate $2.30 ( Bloomberg Consensus)

- Net revenue $23.32 billion, -0.6% y/y, estimate $23.8 billion

- Frito-Lay North America revenue $5.89 billion, -1.1% y/y, estimate $5.95 billion

- Quaker Foods North America revenue $648 million, -13% y/y, estimate $672 million

- PepsiCo Beverages North America revenue $7.18 billion vs. $7.16 billion y/y, estimate $7.28 billion

- Europe revenue $3.95 billion, +6.5% y/y, estimate $3.93 billion

- Latin America revenue $2.92 billion, -4.6% y/y, estimate $3.11 billion

- Africa, Middle East & South Asia revenue $1.55 billion, -3.9% y/y, estimate $1.68 billion

- Asia Pacific, Australia, New Zealand & China revenue $1.20 billion, -1.8% y/y, estimate $1.23 billion

- Organic revenue +1.3% vs. +8.8% y/y, estimate +3%

- Frito-Lay North America organic revenue change: -1%, estimate 0%

- Quaker Foods North America organic revenue change: -13%, estimate -10.4%

- PepsiCo Beverages North America organic revenue change: +1%, estimate +1.86%

- Latin America organic revenue change: +3%, estimate +4.49%

- Europe organic revenue +6%, estimate +7.45%

- Asia Pacific, Australia and New Zealand and China Region organic revenue change: -1% (vs. previously: +9%), estimate +2.92%

- Africa, Middle East and South Asia organic revenue +6%, estimate +11.4%

- EPS $2.13 vs. $2.24 y/y, estimate $2.28

2024 Year forcasts:

- Core EPS: $8.15 (maintained forecast), estimates: 8,14 $

- Low single-digit organic revenue growth (previously: 4% growth)

- 8% EPS growth in constant currency (maintained forecast)