Q3 US Earnings Recap: Profits surprise to the upside, but outlook remains uncertain

US earnings for the third quarter were far better than expected. However, uncertainty about the outlook for company profits continues. We review the quarterly earnings and look ahead to what the markets expect from S&P 500 companies going forward.

By the numbers: S&P 500 companies exceed earnings and revenue expectations

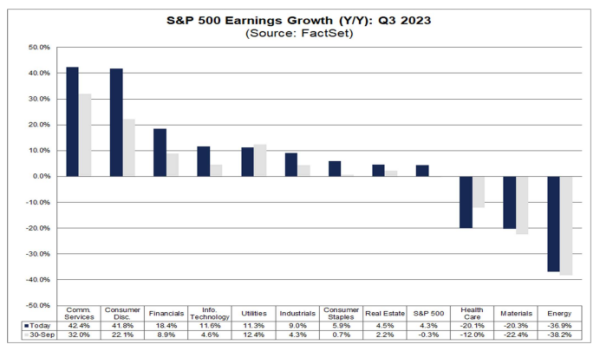

According to FactSet Data, S&P 500 companies far exceeded earnings estimates for the quarter. EPS expanded by 4.3% in Q3, beating the -0.40% consensus forecast heading into the reporting period.

(Source: FactSet)

The better-than-expected result was driven by strong performance amongst communication services and consumer discretionary sectors, with the latter delivering the biggest beat against estimates. The trend was broad-based, however. Based on Bloomberg data, with more than 90% of companies having reported Q3 results, 82% have surprised to the upside, far exceeding the 10-year average of roughly 74%.

(Source: Bloomberg)

Topline growth for S&P 500 companies also beat expectations, albeit by a smaller margin. Revenues rose by 2.4%, bettering the 1.6% growth projected by analysts, with the boost in bottom lines supported by resilient margins as companies manage costs more effectively.

Looking ahead: analysts downgrade earnings outlook

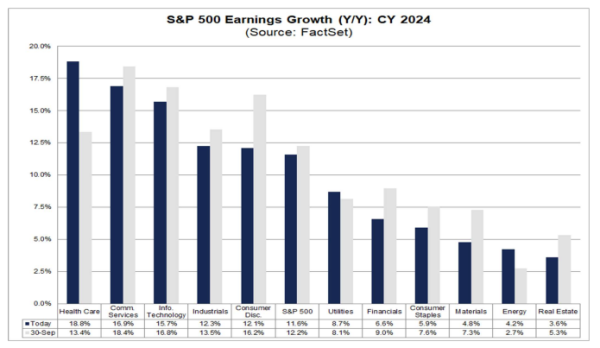

Despite the stronger-than-expected result for the third quarter, analysts remain pessimistic about future earnings. Based on FactSet data, a large part of the earnings growth seen in Q3 was brought forward from Q4, with EPS growth estimates for that quarter downgraded from 8% to 2.9%. Meanwhile, EPS growth for 2024 was revised lower to (albeit still historically high) 11.6%.

(Source: FactSet)

From a qualitative perspective, companies were more optimistic about the macroeconomic backdrop. FactSet analysis identified a continued downtrend in the number of companies citing inflation and recession on their earnings calls, even despite the cautious profit guidance provided.

Technical analysis: S&P 500 charges higher as rate risks fade

The S&P 500 rallied throughout the earnings period, supported by softer US data and expectations that US interest rates have peaked. The index broke downward sloping trendline resistance at a confluence of critical levels at 4400, with momentum surging to the upside. The daily RSI has pushed into overbought territory, with the market looking to consolidate above resistance at approximately 4425. Major resistance could be at the S&P500’s year-to-date higher at 4600.

(Past performance is not a reliable indicator of future results)