RBI rate cut prospects for October dim on rising Middle East tension

The escalating tension in the Middle East, following Iran’s missile attack on Israel, can disrupt oil supply. No wonder, oil prices spiked after the news of Iran’s military operation broke out. There is fear that the regional conflict may snowball into a wider war which can alter the trajectory of interest rates globally.

The major central banks in several major advanced economies, except Japan, and emerging markets have moved towards easing their monetary policies. However, the Middle East crisis is set to pose a new challenge for central banks.

The US Federal Reserve (Fed) began its long-awaited easing cycle at the September 18 meeting with a super-sized interest rate cut of 50 basis points, bringing the federal funds rate down to a range of 4.75-5 percent. The “dot plot” indicated that the Fed would cut 50 basis points (bps) more in CY2024 and a further 100 bps in CY2025.

Back home, all eyes are now on the Reserve Bank of India (RBI) after the US Fed kickstarted the much-awaited rate-cut cycle.

In its last bi-monthly MPC (Monetary Policy Committee) meeting on August 6-8, 2024, the RBI kept the policy repo rate unchanged at 6.5 percent as expected, a decision that was primarily driven by risks to the inflationary outlook.

Goldilocks period for India but geopolitical headwinds ahead

The Indian economy has recovered strongly from the pandemic and is contributing more than 18 percent to global growth. Inflation is on a declining trajectory. The external sector remains resilient with strong buffers. The performance of the banking and corporate sector is healthy. Moreover, fiscal consolidation is underway.

All these favourable macroeconomic factors point to the possible start of a rate-easing cycle by the RBI in the near term as it has always followed a data-dependent approach. However, geopolitical shocks are often not well captured in existing macroeconomic models. The Middle East tension is a new source of shock. Hence, with the focus shifting to external risks, the RBI is likely to turn cautious and respond in a calibrated manner to global turbulences.

Given the evolving geopolitical tension, an October cut is not likely even as the likelihood of a rate cut by the RBI in H2FY25 stays put.

GDP growth resilient, but external risks need to be monitored

India’s economic growth outlook, while positive, faces headwinds from global uncertainties, including a slowdown in key export markets and the rising tension in the Middle East.

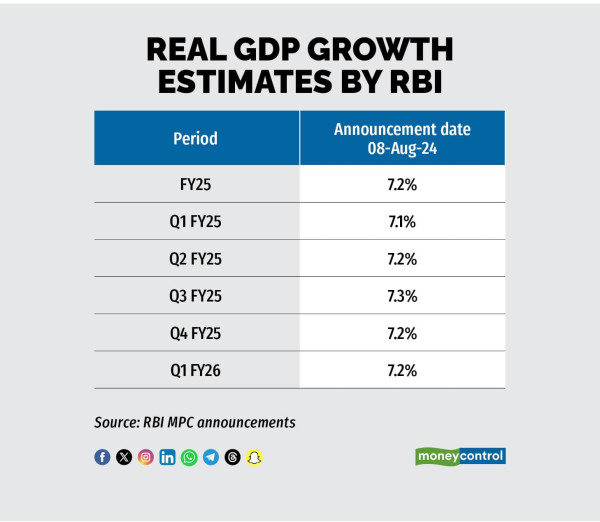

growth estimates by RBI

In Q1FY25, the GDP growth decelerated to a five-quarter low of 6.7 percent year on year (YoY) from 7.8 percent in Q4FY24, albeit on a high base of 8.2 percent in Q1FY24. More important from the perspective of monetary policy, Q1FY25 GDP growth was 40 bps lower than the RBI’s estimate of 7.1 percent YoY.

Benign inflation, but fuel and food prices do pose risk

The RBI wants to wait until inflation stays around the 4 percent (2-6 percent range) target on a durable basis before decisively changing the monetary stance.

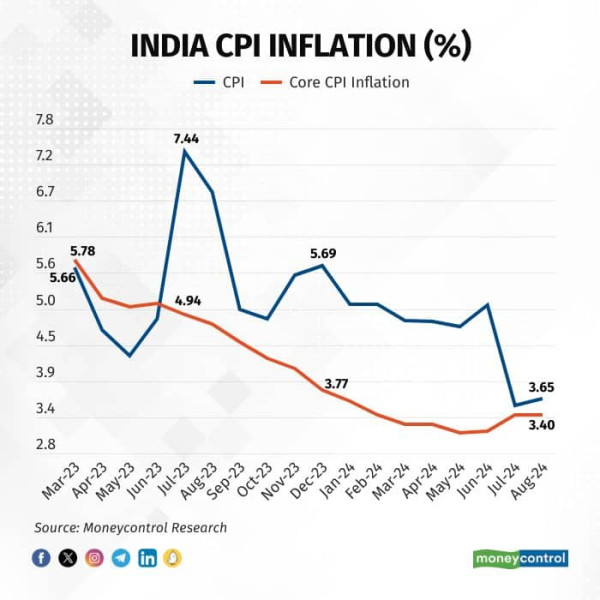

The core CPI inflation that excludes food and fuel prices has consistently stayed below the 4 percent threshold for eight consecutive months. However, the RBI is cautious about food inflation, which accounts for nearly 46 percent of the overall consumer price basket.

Core CPI Inflation is trending downwards

Core CPI Inflation is trending downwards

The overall CPI inflation inched up marginally to 3.7 percent in August, up from 3.5 percent in July, largely on account of an uptick in food inflation. Although the monsoon was erratic, late-season rains have eased concerns over food inflation, one of the primary factors that drove up prices earlier.

But the new risk from fuel prices has emerged amid the ongoing Iran-Israel tension.

Brent crude prices had fallen to about $70-71 per barrel last week, down from $80 per barrel in the last week of August. However, following the news flow from Middle East, it touched almost $75 per barrel on Wednesday with an increased upside risk.

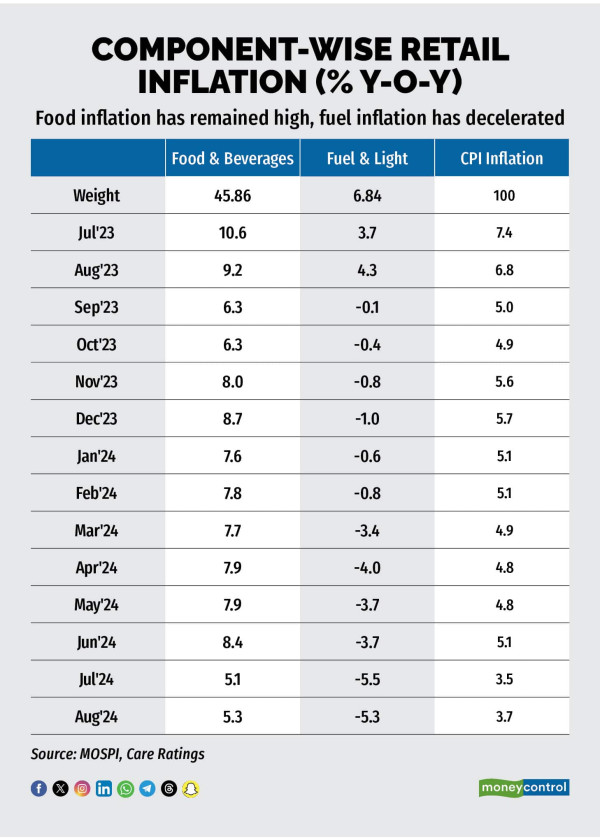

While fuel has weight of only 7 percent in the CPI (consumer price index) basket, the risk of fuel prices passing through to the domestic consumption basket remains a key concern. Hence, monitoring the Brent crude prices going ahead is crucial from the inflation perspective.

inflation has remained high, fuel inflation has decelerated

Expect RBI to initiate rate cut in H2 FY25, but October turns tricky

While it is difficult to predict the exact month of RBI’s action, the rate cut is likely to be shallow, consisting of 50 bps in two tranches. According to the latest estimate by RBI, the natural (neutral) rate of interest is between 1.4 and 1.9 percent.

With the RBI projecting FY25 average inflation at 4.5 percent, the real interest rate stands close to 2 percent (as Repo is at 6.5 percent), providing some opportunity for a shallow rate cut of only 50 bps.

-

-

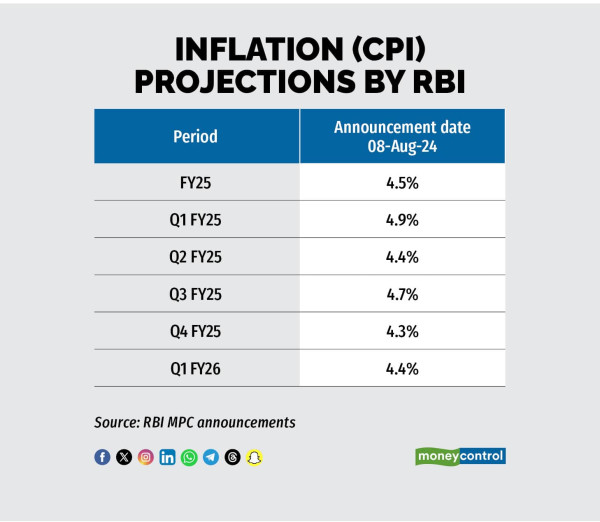

inflation estimates by RBI

The CPI inflation in the second quarter (Q2FY25) is likely to substantially undershoot the RBI’s projections of 4.4 percent. While this can support rate cut, the RBI will take into consideration the fact that the base effect for the CPI will turn unfavourable in September, ahead of an early festive season this year. More importantly, it will be mindful of external risks to the inflationary outlook, stemming from geopolitical uncertainties. In addition to the turmoil in Middle East, a Trump win in the upcoming US elections could be inflationary, because of his protectionist stance.

Overall, while the RBI is likely to initiate a rate-cut cycle in the second half of the fiscal year (H2FY25), the October rate cut is not given amid the rising tensions in Middle East.

Follow @nehadave01

For more research articles, visit our Moneycontrol Research page