Sentiment-driven crude sell-off eases, allowing traders to focus on supply risks

Key points

Crude oil has started August on the defensive amid growth concerns and deleveraging focus

Brent show signs of bottoming out around USD 75 but wider market developments remain a short-term driver

Potential supply risks in focus, as well as OPEC+ and hurricane season

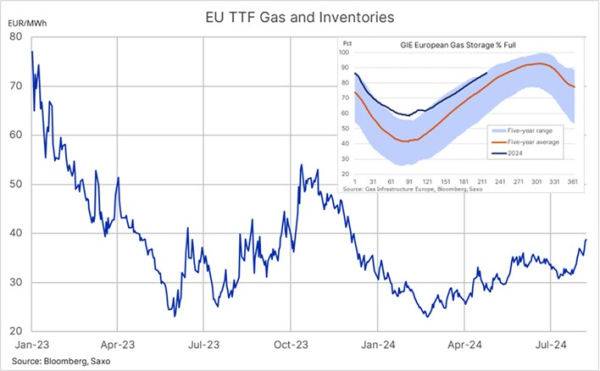

European natural gas jumps to December high amid fears Russia may cut supplies through Ukraine

Crude oil has started August on the defensive, with prices suffering additional losses on top of those seen last month, amid headlines being dominated by the poor outlook for Chinese demand and now also increased focus on whether the US economy can avoid a recession. In addition, the recent loss of risk appetite across key stock market sectors culminated on Monday as a major deleveraging move out of short yen positions sent shockwaves across global markets, including commodities where recent popular investments in crude, copper, and even gold all suffered setbacks amid the need from funds to reduce their overall level of risk as volatility surged higher.

Brent, in the process, reached the bottom of a long-held range between USD 75 and USD 90 per barrel before stabilising markets, geopolitical tensions, a continued drop in US crude stocks, and a technically oversold market condition all helped support a small and ongoing recovery. For now, developments across wider markets will continue to hold major sway over the energy sector, with crude oil prices probably receiving more directional guidance from equity markets than energy-related fundamentals.

Supply risks remain a concern following a halt to production from Libya’s biggest field, while geopolitical tensions focus on Ukraine’s cross-border attack on Russia, and not least Iran’s promise to punish Israel for last week’s assassination of a leading Hamas figure in Tehran. A threat that has so far caused a limited reaction in the market amid reports Iran wants to avoid a region-wide war, which ultimately could lead to the disruption of flows of oil and gas from the Middle East.

In addition, it is increasingly likely that OPEC+ decides to defer the planned October production increase given the current fragility and negative sentiment from outside developments. Also, having entered the North Atlantic hurricane season, the risk of related disruptions, either to the production of crude or the refining of products, will present an underlying source of support.

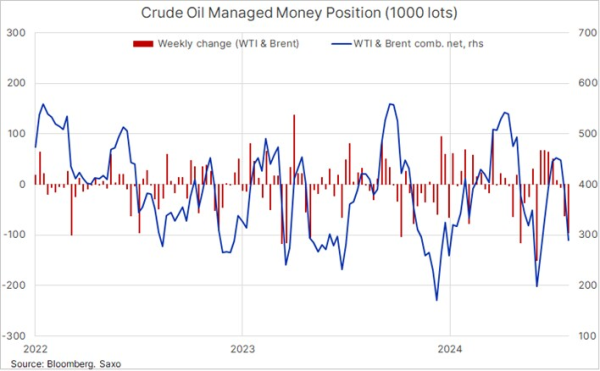

Adding up these current and potential future developments, we see the market hold current support levels; however, with the upside potential for now being limited to the mid-80s. During a two-week period to July 30, hedge funds and other large speculators cut their WTI and Brent crude net long by 35% with the 158 million barrels being the most aggressive in 14 months. If we add the additional weakness since the latest reporting period, we can assume that this length has been reduced further, thereby sowing the seeds for an eventual price recovery from fresh demand once the technical or fundamental outlook improves.

European natural gas jumps to December high

Dutch TTF gas, the European benchmark, trades at the highest level this year on renewed fears of a possible disruption on the remaining pipeline supplying Russian gas to Europe via Ukraine. Since hitting EUR 30.32/MWh low last month, the price has steadily been rising amid temporary disruptions to flows from Norway due to maintenance and unplanned works, and increased competition for LNG cargoes from Asia, where sweltering heat has increased demand for gas from power generators towards cooling. Developments that have seen the seasonal stock building ahead of winter slow, but at 86.5% full, there is limited risk of inventories not reaching desired levels before demand in a few months’ time eventually exceeds supply.

As Russia fights its largest incursion by Ukrainian troops since Putin started his unprovoked attack on the sovereign nation back in 2022, the counterattack has occurred in Russia’s Kursk region, which hosts a key gas transmission point, the Sudzha station near the border, which in recent months has seen daily flows of around 42 million cubic metres. This flow is already expected to grind to a halt by yearend when a transit agreement between Russia and Ukraine expires, thereby disrupting flows to Slovakia and Austria, who currently depend on that supply. Any major disruption before then would increase the need to seek alternative supplies, mostly via LNG; hence the higher price as Europe will have to compete with buyers in Asia and South America.

Recent commodity articles:

7 Aug 2024: Limited short-selling interest observed during copper's recent aggressive correction

6 Aug 2024: Video: What factors are fueling the current market turmoil and gold's response

5 Aug 2024: COT: Broad commodities sell-off gains momentum; Forex traders seek JPY and CHF

5 Aug 2024: Commodities: Position reduction in focus as volatility spikes

2 Aug 2024: Widespread commodities decline in July, with gold as the notable exception

31 July 2024: Crude's month-long slide halted by fresh Mideast worries

30 July 2024: Record demand explains gold's current resilience

29 July 2024: COT: Energy and metals selling cuts hedge fund long to four-month low

4 July 2024: Sluggish US economic indicators boost demand for gold and silver

4 July 2024: Podcast Special: Quarterly Outlook - Sandcastle Economics

2 July 2024: Quarterly Outlook - Energy and grains in focus as metals pause

1 July 2024: COT: Crude long builds ahead of Q3 while grains selling accelerates

28 June 2024: Metals and natural gas propel commodity sector to quarterly gain

26 June 2024: Crude seeks support from seasonal demand strength

24 June 2024: Copper's resilience despite China weakness

18 June 2024: Precious metals go through prolonger period of consolidation

17 June 2024: COT: Dollar long jumps; Funds start rebuilding crude long

14 June 2024: Commodity weekly: Energy sector gains counterbalance metal consolidation

13 June 2024: Oil prices steady amid divergent OPEC and IEA demand projections

10 June 2024: COT: Brent long cut to ten-year low; metals left exposed to end of week slump

3 June 2024: COT: Crude length added before OPEC+ meeting; gold and copper see profit-taking