September market performance: emerging markets and Asia lead global equity gains

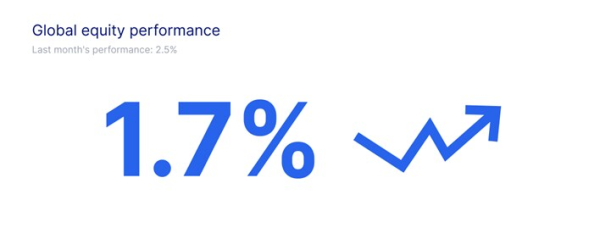

September was another solid month for global equity markets, with the MSCI World Index advancing 1.7%. While not as dramatic as some previous months, this growth shows that investor confidence continues to build, despite the economic uncertainties in various regions. The global rally, driven primarily by Asia and emerging markets, highlights the evolving dynamics in global equity performance.

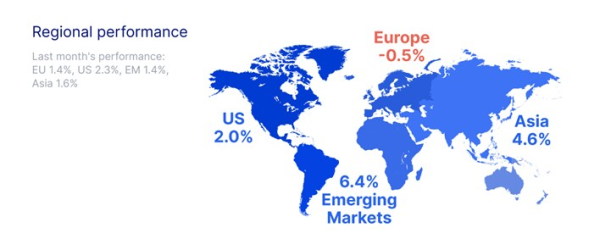

United States (S&P 500): The S&P 500 rose by 2.0% in September, extending its gains from earlier in the year. Investor sentiment remains upbeat, with the market showing resilience as it adapts to the ongoing Federal Reserve rate decisions and macroeconomic factors.

Europe: European equities struggled in September, falling by 0.5%. The energy crisis and inflationary concerns weighed on European markets, with investors growing cautious about the region’s economic outlook.

Asia: Asia emerged as a key driver of global market performance, with a robust 4.6% gain. Strong corporate earnings and favourable government policies, especially in Japan and China’s stimulus, boosted investor confidence across the region.

Emerging markets: Emerging markets were the standout performers in September, surging 6.4%. Chinese stimuli and other regions within the emerging markets space posted strong growth.

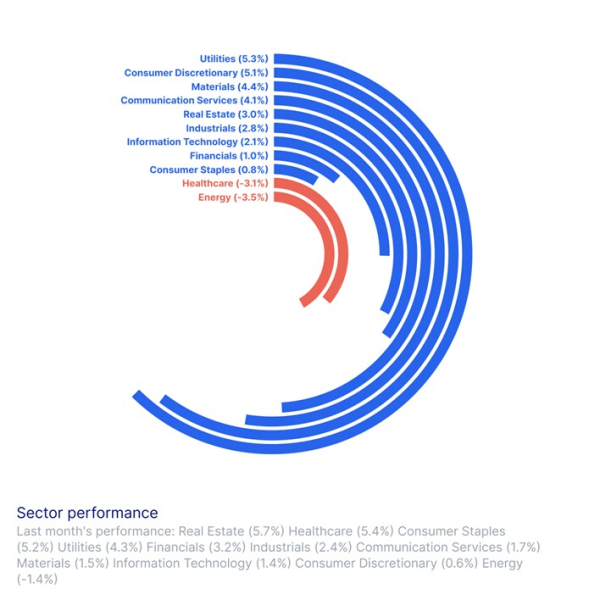

Sector performance in September presented a mixed picture, with several sectors showing notable strength while others struggled:

Utilities: The utilities sector led the way, rising 5.3% as investors flocked to its defensive nature amid broader market volatility.

Consumer discretionary: This sector saw a significant gain of 5.1%, driven by increased consumer spending and optimism about future economic growth.

Materials: The materials sector climbed 4.4%, benefiting from the ongoing demand for commodities and raw materials in manufacturing.

Communication services: Communication services saw a 4.1% gain, reflecting strong performances from companies in media, telecommunications, and entertainment.

Real estate: Real estate posted a 3.0% increase, continuing its solid performance as investors seek stable, tangible assets.

Healthcare and energy: Healthcare experienced a sharp decline of -3.1%, while energy dropped -3.5%. Oil’s sharp decline of -7.3% weighed heavily on the energy sector, as uncertainties around energy demand and price volatility continued to impact investor sentiment.

Sources: Bloomberg and Saxo

Global equities are measured using the MSCI World Index. Equity regions are measured using the S&P 500 (US) and the MSCI indices Europe, AC Asia Pacific, and EM respectively. Equity sectors are measured using the MSCI World/Sector indices, e.g., MSCI World/Energy. Bonds are measured using the USD-hedged Bloomberg Aggregate Total Return indices for total, sovereign, and corporate respectively.