S&P 500 weekly report: What to expect for US retail sales ahead

What to expect for US September retail sales data this week?

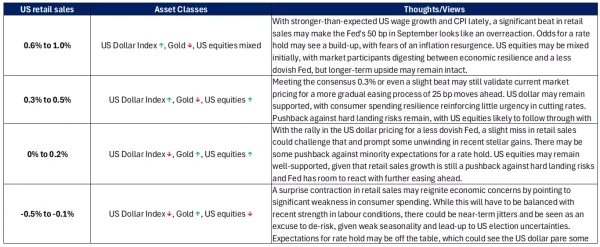

This week, the US September retail sales data will be closely watched as a barometer for the US economy, given that consumer spending accounts for about 65 - 70% of the US gross domestic product (GDP). Expectations are for headline retail sales to grow 0.3% month-on-month, up from the 0.1% prior, while core retail sales are expected to stay unchanged at 0.1%. Other same-day data releases include US weekly unemployment claims, which is expected to tick lower to 241,000 last week versus the 258,000 prior.

Thus far, US consumers have been resilient, having beaten expectations for three straight months. With the US economic surprise index back in positive territory for the first time since April this year, another beat in retail sales will add to the current trend of upside economic surprises.

The key risk could be any significant deviation in the retail sales number from consensus. With stronger-than-expected wage growth and consumer price index (CPI) inflation lately, an overwhelming beat in retail sales could question the Federal Reserve (Fed)’s previous rate decision and spur some inflation resurgence concerns. On the other hand, a significant miss could highlight greater economic risks and question if another 50 basis point (bp) move will be needed in November.

Here may be a few potential scenarios to consider:

Nasdaq 100: Eyeing to retest previous record high

Traction in growth sectors has been robust lately, despite Treasury yields surging to its highest level in two months, as renewed hype around artificial intelligence (AI) demand has overridden expectations for a less-dovish Fed. With the S&P 500 and Dow Jones Industrial Average (DJIA) posting yet another record highs this week, eyes will be on whether the Nasdaq will follow suit, being less than 2% away. Previous retracement has offered a more neutral positioning for market breadth, along with a technical reset in terms of near-term conditions, offering room for the rally to continue.

Focus will be on upcoming corporate earnings to justify the relatively high valuation in tech stocks. A move in the index above its July 2024 high at the 20,700 level could pave the way towards the 22,000 level next. On the downside, a retracement will still leave buying-on-dips as the preferred approach, given the broader upward trend in place. Near-term support to watch may be at the 19,670 level, followed by the 18,920 level.

Levels:

R2: 22,000

R1: 20,700

S1: 19,670

S2: 18,920

Source: IG charts

Sector performance

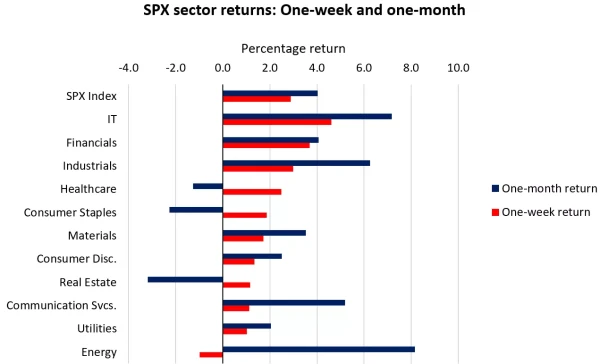

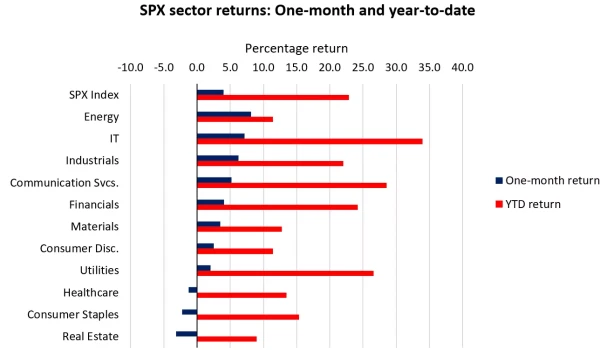

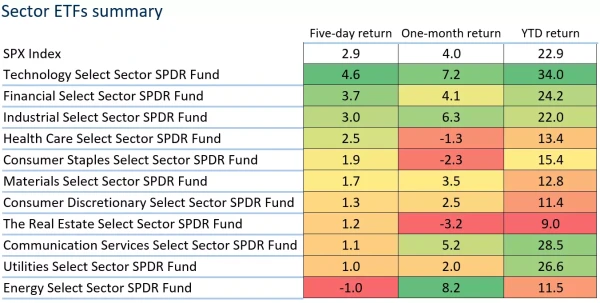

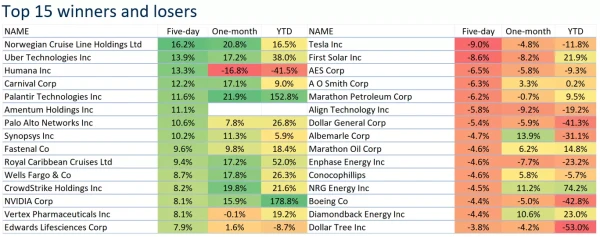

Sector performance over the past week revealed a broad risk-on rally, with ten out of the 11 S&P 500 sectors in the green, as positive economic surprises out of the US overrides weak seasonality. The exception was the energy sector (-1.0%), which was weighed by a 7% retracement in crude oil prices as market participants fade geopolitical risks in the Middle East. Technology was the outperformer (+4.6%), as renewed confidence over a soft landing brings fresh momentum to megacap stocks. Nvidia was up 8.1% over the past week, Apple was up 4.3% while Amazon was up 3.7%. The sole dampener was Tesla, which lost 9.0%, following some ‘sell the news’ with its Robotaxi event.

Source: Refinitiv

Source: Refinitiv

Source: Refinitiv

*Note: The data is from 8th – 14th October 2024.

Source: Refinitiv

*Note: The data is from 8th – 14th October 2024.

Source: Refinitiv

*Note: The data is from 8th – 14th October 2024.