The Fed rate cut cycle starts with a bang

Key points

- Fast now, but slowing ahead: The Fed cut rates by 50 bps, balancing the labour market and inflation, with a focus on full employment. Fed Chair Powell indicated future cuts would occur at a slower pace, with a projection of 50 more bps cuts by year-end and a gradual decline to 2.75-3% by 2026.

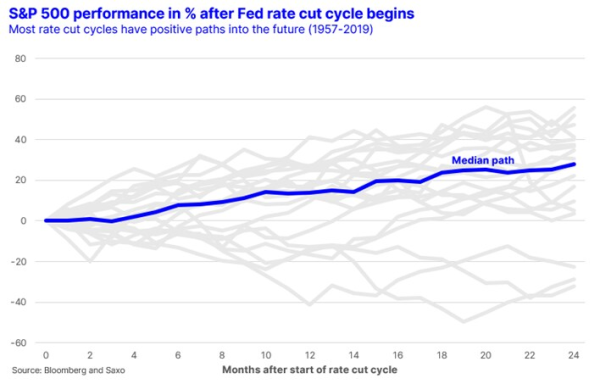

- Rate cut cycles and market history: Despite concerns from past cycles like 2000 and 2007, only 3 out of 20 cycles since 1957 have resulted in negative equity returns. Historically, rate cut cycles have led to strong equity performance, suggesting a need to adjust portfolios toward sectors like consumer discretionary, utilities, and energy.

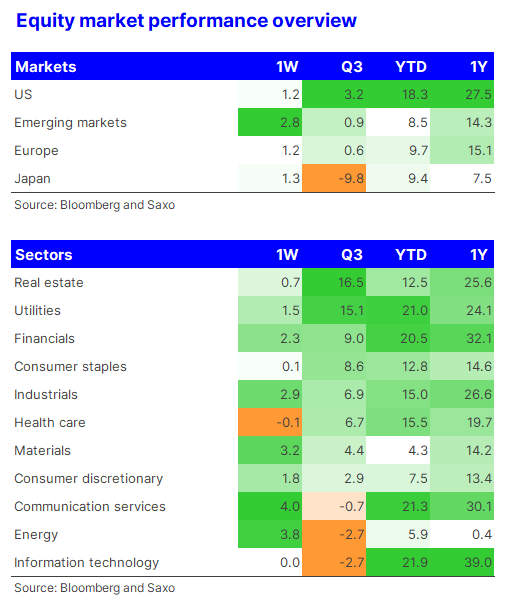

- Equity market reaction: Following the Fed’s rate cut, market reactions were mixed, with confusion evident across sectors. While energy and communication services outperformed, utilities and tech lagged. The next two days will be critical to assess whether there is a sector rotation or a move into small caps and cyclical sectors.

Fast now, but not so fast going forward

I was in the Michelle Bowman’s camp, the only dissenting vote last night in favour of 25 bps rate cut, but Powell managed to convince the rest of the FOMC voting members to cut by 50 bps. As the FOMC statement explains the Fed is not worried about the economy, but sees a balance between the labour market and inflation for the first time in years, and with inflation risks coming down according to the Fed, it went with 50 bps to support the labour market to ensure full employment.

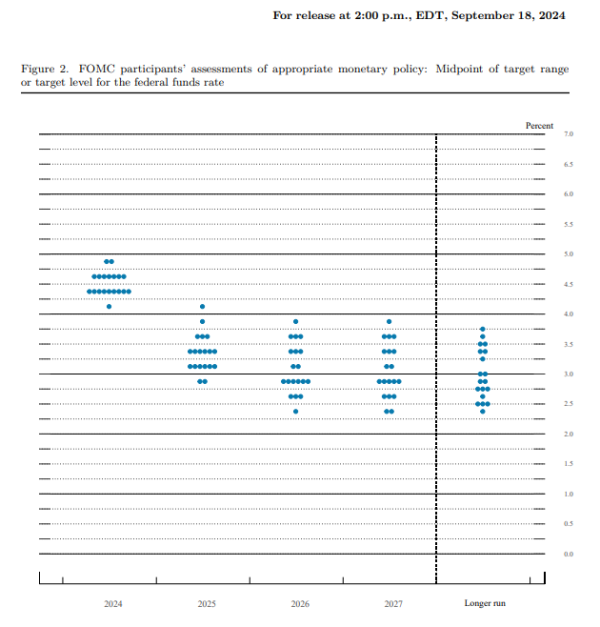

The updated dot plot (see below) indicate that the Fed sees another 50 bps rate cut by year-end delivered over two meetings in November and December. The dot plot also shows that the Fed expects the policy rate to fall to around 2.75-3% by 2026 and then closer to 2.75% in the longer run. The Fed’s projections that the unemployment rate will rise was also a contributing factor to the 50 bps cut.

On the subsequent press conference Fed Chair Jerome Powell made it clear that the Fed does not intend to go this fast on all meetings but instead in a slower tempo. He did everything he could to spin the 50 bps cut as a dovish move and said that he did not think the Fed is behind the curve. He also talked positively about the economy overall. But as everyone knows economic forecasts rot faster than an apple in the sun as incoming data can quickly recent projections look wrong. In any case, the Fed rate cut cycle has begun and evolving US economic data points will dictate the speed of descent for the Fed funds rate.

What does history tell us about Fed rate cut cycles?

Many market commentators are portraying a rate cut cycle as something bad for the economy and markets. It is correct that the rate cut cycles of 2000 and 2007 both led into recession and large selloffs in equities. But is that really the norm?

There has been around 20 complete Fed rate cut cycles since 1957 and of those only three ended up with negative equity returns in the 24 months following the start of the rate cut cycle. Those negative rate cut cycles are 1973, 2000, and 2007. In other words, investors should be careful of putting too high a weight on the 2000 and 2007 rate cut cycles as a guidance for what comes next. The median path shows that the equity market delivers almost 28% return after a rate cut cycle has begun. That return is higher than the average 24-month return in US equities.

Instead of trying to time recessions and figure out whether this rate cut cycle means doom and gloom, it is far more important to look at the portfolio and think about whether it has the right exposures in a falling policy rate environment. Many retail investors are overweight technology, but sectors like consumer discretionary, utilities, communication services, and energy might offer better returns in a falling interest rate environment.

The equity market reaction the next two days is important

The initial reaction to the Fed’s rate cut was positive and then it turned negative with US equities declining yesterday. Futures have since turned around with technology stocks indicated 1.8% higher in the pre-market session.

If we look at the market reaction yesterday across sectors and equity factors then it was an odd reaction. Energy and communication services were the two best performing sectors while utilities and information technology (IT) were the two worst performing sectors. Utilities and IT are two very high duration (meaning they should react the most positively to lower interest rates) pockets of the equity market, but they reacted negatively. Across equity factors (momentum, quality etc.) there was very little dispersion indicating that market participants were confused about the interpretation of the Fed’s decision.

Today and tomorrow are going to be crucial in understanding how the market is positioning itself after the rate decision. Is it a rotation into small caps and cyclical sectors? Will utilities and real estate sectors continue to be winning sectors like we have seen so far in the third quarter? Will emerging markets finally get some love despite China’s structural headwinds? Those questions will soon be answered.

Previous notes on asset allocation and macro

- Will the market get what it wants? (2 September 2024)

- The perfect storm hits market and what comes next (5 August 2024)

- Everyone on Wall Street is talking about these key risks (9 July 2024)

- French election: Is this a new Meloni moment for Europe? (24 June 2024)

- US rate cut seems distant as inflation report looms (10 June 2024)

- Commodities setback, investment drought in mining, and EM elections (3 June 2024)

- The inflation conundrum and private equity party (27 May 2024)