The Week Ahead in FX

Hello, everyone – I’m back covering FX, hopefully on a weekly basis at minimum. For this week, I am doing a week ahead piece, as you can see below that we have one heck of an action-packed week before the following week’s event risk of the year, the US election.

By the way, you can sign up for the webinar Trading the US Election I will be hosting together with colleagues Charu and Koen next Tuesday.

Chart: USDJPY

USDJPY leaped above the 200-day moving average Wednesday and has almost tested the 61.8% Fibo retracement of the massive downdraft that was accelerated by the one-two of the July 31 BoJ large hike surprise and the dovish Fed surprise later the same day. Interesting to note that current levels represent a full retracement back to the price action on that day. The US dollar has been lifted by the market pricing in either a very soft landing or no landing at all as well as the rising perceived probability of a Trump 2.0 regime helping send US treasury yields higher. The USDJPY pair will likely move the most on the US election event risk – but let’s not forget a very important Bank of Japan next Thursday. We are likely very close to territory where Japan may step in to intervene. Optionality is very expensive for good reason, as one can imagine 145 or 155 or both trading within the next two weeks under possibly scenarios.

FX calendar next week and what’s at stake (times are GMT where shown):

Note for Europeans! Next week is the odd week for Europe and possibly elsewhere in which local clocks have been set back an hour while the US doesn’t set its clocks back until next weekend on November 3 - so US data an hour early next week.

Trump on Joe Rogan podcast (late today) – impossible to quantify this as an event risk, but this is likely the most high-profile appearance former president Trump could possibly do between now and election day. Rogan has millions of followers and listeners who are used to tuning in for hours-long discussions. So millions of possible voters will be listening and it might change some few thousands or tens of thousands of minds if – enough to determine the election outcome if things are very close, which they very much appear to be. Watch for any consensus takeaway, though it seems Trump can get away with saying just about anything and even reveling in that fact.

Japan election (this weekend) The LDP may struggle to get its usual outright one-party majority in the key lower house (233 seats needed for that) due to a recent scandal in the LDP ranks, which saw new Prime Minister Ishiba booting some 12 LDP members from the party, although 10 of these are running as independents. This would require relying on the Komeito party for a coalition if Ishiba rules out rapprochement with the shunned former LDP members. The less power for the LDP, perhaps the more the inflationary risk for Japan as other parties call for more spending.

France budget (starting Monday night and lasting through Friday). The debate on the new budget will start with taxing plans and moves on later with the spending plans. In general, the impression is that PM Barnier wants to deliver years of growth killing austerity and tax rises – bad for the euro at the margin, but only becoming alarming if French sovereign debt misbehaves. This is not necessarily an event risk that will see immediate impact, but France’s ability to get its fiscal house in order and is critical for the longer haul as it is violating EU budget deficit rules (forecast at 6% for this year versus 3% max under EU rules). The hung parliament will make the going very tough for PM Barnier and President Macron. Worth keeping an eye on the France-Germany 10-year yield spread, which peaked on three occasions at around 80 basis points, the first time just ahead of the legislative elections in June. That spread is at 72 basis points going into this budget announcement.

Australia Q3 CPI (0030 Wednesday) The RBA has been quite firm that they are going to take it easy on the rate cuts – only a big acceleration lower in the core CPI (the “trimmed mean” usually the focus with these quarterly numbers) might change the narrative, with more than 50/50 odds of a rate reductio not priced at the moment until the February RBA meeting. Otherwise, AUD also held up at margin by hopes for more Chinese stimulus – any news there probably more impactful than potential for rate outlook shifts.

US Oct. ADP Payrolls (1215 Wednesday) – The market and USD will be very twitchy on all US labor market data – this data series ticked higher to 143k in September after two rather weak numbers the prior two months. October’s number expected at +99k.

UK autumn budget statement (1230 Wednesday). This is potentially pivotal for sterling. The degree to which Chancellor Rachel Reeves can deliver expanded spending priorities and new taxes without triggering either Gilt vigilantes on the one hand, or a more pessimistic outlook for growth on the other is the two-sided risk here. She has sent many of the right messages: wanting to avoid austerity and ruling out income tax hikes, while encouraging much-needed investment. If the market greets the effort with higher Gilt yields on the anticipation of stronger UK growth (as opposed to an ugly spike of yields a la the Truss/Kwarteng mini-budget of September 2022), it could keep the path of Bank of England cuts at a modest pace and boost sterling, especially versus the Euro as the contrast with the growth-killing approach in France and the woeful outlook for Germany is stark.

US GDP first estimate (1230 Wednesday) - a lot of discussion that public sector is driving the US GDP outperformance, for what it’s worth (not much yet).

Germany Flash Oct. CPI (1300 Wednesday) – delivered the same day as Q3 GDP, which is scraping along near 0% or worse. Tactically important as market struggles with mixed message from ECB – currently about 35% in favour of a larger 50 bps cut at December ECB meet.

Bank of Japan (Thursday – released during the night (most likely 0230-0330) – The Bank of Japan is seen not likely to move at this Thursday’s meeting, but the guidance will prove critical. The recent sharp rally in JPY crosses has been driven by the strong back-up in US yields at the long end of the yield curve, in part on the anticipation of Trump 2.0, or Republican sweep of the White House and both houses of Congress.

Eurozone October CPI – (1000 Thursday) Important as input for as ECB is supposedly still a single-mandate central bank focused on inflation.

US Oct. Nonfarm Payrolls Change and Unemployment Rate (1230 Friday) – This is the most important data release ahead of the election on November 5. Many have rightly bemoaned the quality of the Nonfarm payrolls data series, which has been plagued by massive revisions that should make us all wonder why we bother reacting to each new monthly data point. As well, the BLS has noted a huge drop in participation of the survey. Alas, I suppose we react because we have no other choice. Expectations for the October payrolls growth running at +120k and an unchanged 4.1% figure is expected for the Unemployment Rate.

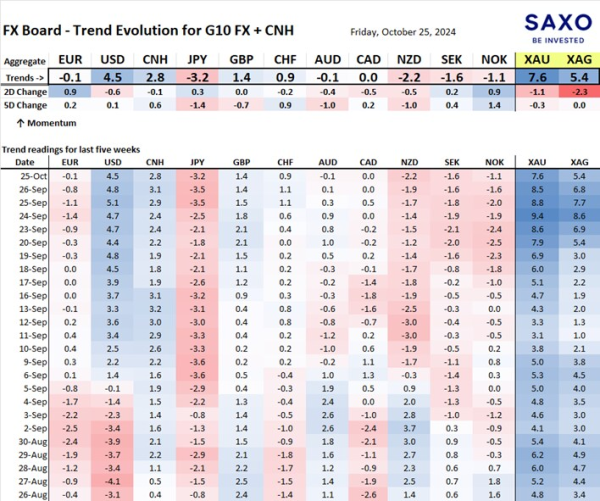

Table: FX Board of Trends in G10 FX + CNH & precious metals.

Note: the FX Board trend indicators are only on a relative scale and are volatility adjusted. Readings below an absolute value of 2 are fairly weak, while a reading above 4 is quite strong and above 6 very strong.

The US dollar the strongest trending currency and the JPY the weakest – no surprise there. Note that the gold trend hit a massive 9.4 at the start of this week – a very rare reading for any of the FX board currencies/metals.

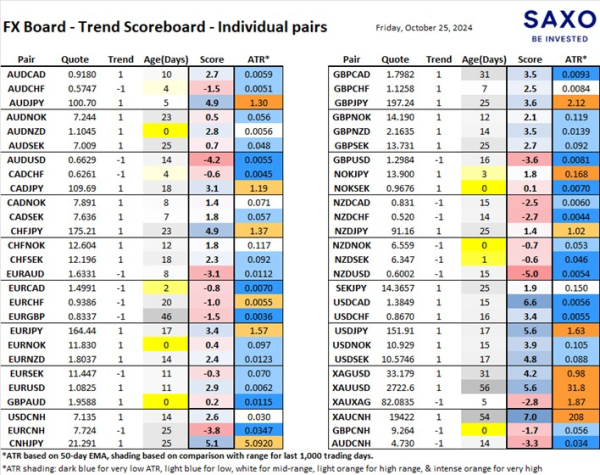

Table: FX Board Trend Scoreboard for individual pairs.

What sticks out like a sore thumb here is the hot volatility levels in JPY pairs and precious metals (The ATR shading indicates from blue (suppressed trading ranges) to bright orange (large trading ranges). Elsewhere, most of the rest of FX is mired in low volatility ranges, even with some of the fairly persistent trending moves we have seen over the last couple of weeks in USD pairs.